Can Hastings hold on to top spot? Insurance Times analysis of annual underwriting results reveals which insurers took the gold, silver and bronze across several league tables, and which was judged overall as the top performing firm

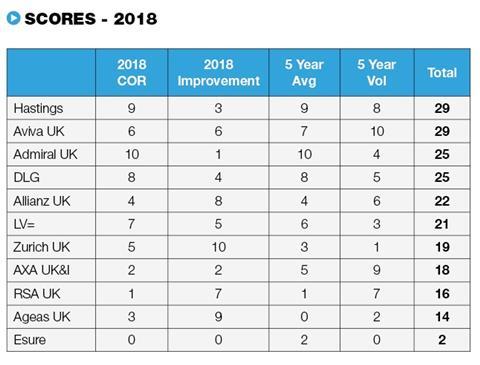

Hastings has once again retained its place at the top of the Insurance Times underwriting league table, but needed a tie-breaker to separate it from Aviva after the two insurers tied on 29 points.

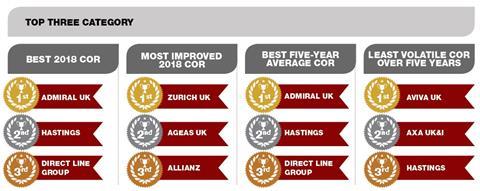

Hastings clinched the top spot courtesy of its three podium finishes across the four ranking criteria, compared with Aviva’s solitary top three finish, meaning that the insurer has now won the gold medal every year since its debut 2016 results.

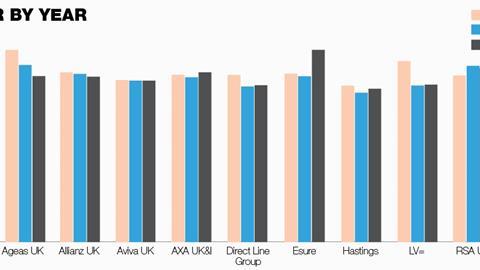

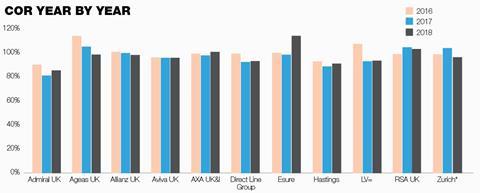

Hastings reported a profitable combined operating ratio (COR) of 89.4%, the second-best in this year’s analysis behind Admiral, as it reported record profits across the group and strong growth. Previous table-topper Admiral, the last insurer other than Hastings to take gold back in 2016, dropped to third place despite reporting the best COR for 2018 at 83.6%.

Admiral’s overall ranking was hit hard by a 3.9 percentage point worsening of its COR compared with 2017’s market-leading 79.7%, with only esure, whose COR rose by a whopping 15.1%, seeing a larger increase over the last 12 months.

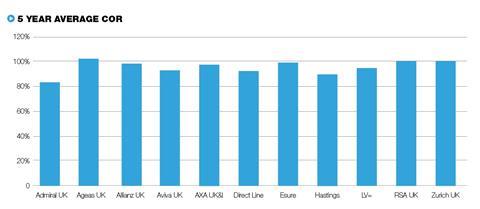

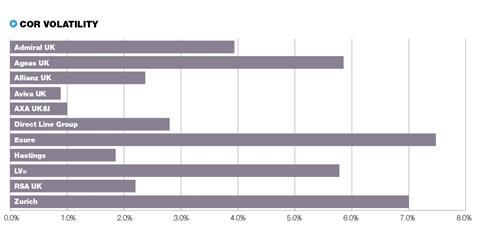

Shareholders like stability and consistency when it comes to analysing investments and, despite Admiral reporting the best average COR over the last five years, the high levels of variability in its underwriting performance meant that it was only able to secure seventh place in our five-year COR volatility analysis.

The situation looks worse for Admiral once the impacts of the Ogden discount rate are taken into account, with the insurer releasing £140m from reserves as a result of this one-off change in assumptions. Shareholders were spooked, with Admiral’s share price dropping 4% on the back of these results. Announcing Admiral’s results for 2018, chief executive David Stevens admitted it had been a mixed year for the insurer, with challenging times ahead.

“Yes, we delivered record profits and dividends, but we were helped by the UK government’s decision to unwind partially the change in the Ogden discount rate from a couple of years ago,” he said.

“Yes, we grew rapidly pretty much across the board, but growth in the core UK motor business slowed in the second half as we reduced our competitiveness in the face of rising claims costs.”

The former table-topper has fallen four points behind Hastings and Aviva at the top of the overall rankings, level on points with Direct Line Group (DLG) on 25 out of a possible 40.

Biggest climber

Aviva, meanwhile, has had the biggest rise up the table, as it climbed from fifth to second-place, and level on points with Hastings, on top. The driving force behind the insurer’s climb up the rankings was the clinching of top marks for its five-year COR volatility, with its COR changing by no more than 0.8 percentage points over the five-year period, a sign of consistent and accurate underwriting.

Aviva is the only insurer in this analysis that has improved its COR every year for the last five years, something Aviva managing director of intermediaries Phil Bayles hailed as a stand-out achievement.

“Often people see a trade off between growth and profitability, but we have broken that trade-off, are growing at a decent rate and improving our profitability at the same time,” he said.

“One of the nice things about running a successful business is people want you to do more of it and they’ll carry on investing in it. The message that we’re getting from the business is keep doing what you’re doing, keep growing, and you’re on the right track.”

Poor performance

At the other end of the scale, esure has suffered the most in the rankings as it fell from sixth to last thanks to a loss-making COR of 111.8% for 2018, compared with 96.7% for 2017.

While 2018 was the only year in the last five for which esure reported a loss-making underwriting performance, the scale of the increase, driven largely by claims inflation across its motor and home books, means the insurer failed to pick up any points in three of the four categories. It slumped to last position in all but the five-year average COR analysis, picking up just two points for its ninth place finish under this measure.

This poor underwriting performance means the insurer turned 2017’s £98.6m profit into a £15.6m loss for 2018, with that loss meaning that esure was only just above its solvency capital requirement with own funds of £356.7m (2017: £330.3m) and a solvency coverage of 108% (2017: 156%).

Analysts had been concerned about esure’s aggressive growth targets for a while. Berenberg’s response to esure revealing its solvency issues pointed out it had previously said it “believed esure’s growth and footprint expansion was fraught with risk, especially given its minimal reserving buffers”.

Difficult year

Esure founder and chairman Sir Peter Wood said it had been a difficult year for the insurer, but that the backing from Bain Capital, which acquired the business for £1.2bn in August 2018, would help secure the investment needed to drive the business forward and put it back on a solid solvency base.

“The team is focused on evolving the group’s long-term strategy in response to a world which is changing at an increasing pace, with advances in digital and data analytics shaping customer expectations of all businesses,” he said.

“However, 2018 was not without challenge. Firstly, competitive market dynamics (lower premiums and elevated claims inflation in motor) combined with the group’s own claims experience impacted upon its underwriting performance.

“Secondly, the exceptional weather events seen across the UK, particularly in the first half of the year, increased claims costs.”

In May 2019, esure revealed it had restored its solvency ratio to a more healthy 149% by implementing a reinsurance arrangement that includes adverse development cover, preventing net claims liabilities deteriorating beyond a pre-agreed point.

But with claims inflation in the motor market set to ruffle the feathers of insurers across UK general insurance even more as they report their results for 2019, we could see a further shake-up in the rankings as we move into next year and beyond.

Methodology

Insurers were ranked on four aspects of their combined operating ratio (COR) performance: full-year 2018 COR; how much the COR had improved over 2017; the average five-year COR; and COR volatility over five years.

For each of the four criteria, insurers were assigned a score of zero to 10 depending on their position in the ranking for that category, with 10 points for the company at the top of the table and no points for the company at the bottom.

The scores for the four criteria were combined to give the final ranking and all were given equal weighting.

No comments yet