Industry voices believe a boom in employment liability claims is on the horizon. Insurance Times explores the Covid-19-related drivers behind the trend as well as what insurers and employers need to consider to mitigate claims

Employment liability is predicted to form the “next wave of claims” arising from the Covid-19 pandemic, as industry commentators note “a spike” in claims activity.

Outlining this trend, Gallagher Bassett’s chief client officer for the UK Peter Diskin explained: “We’re just starting to see a spike in employment liability claims and they are coming as a direct result of – allegedly - Covid, where frontline workers are indicating that they contracted Covid as a result of not being supplied with the right [personal protective equipment] quickly enough, or put in positions where there wasn’t social distancing, continuing to serve people in restaurants and so forth without the right equipment or the right space.

“It’s going to be some testing times in the employment liability world around how those claims are going to be dealt with, how are they going to be defended, how are they going to be paid and if they’re paid, what precedence does that set?”

Aaron le Marquer, a partner at Fenchurch Law, agreed with Diskin’s analysis.

“Of course, we’ve got a very infectious disease here, which is causing very widespread illness and sickness and deaths, so the question is bound to arise: are employers liable?” he said. “There could be and there certainly will be claims.”

Although healthcare settings – such as care homes - and hospitality are likely to be the main sectors hit with these types of employment liability claims, Hayley Kiely, legal assistant at law firm Weightmans, anticipates that the aviation industry may also face claims.

In particular, she noted there could be issues around how crew are rested on long-haul flights moving forward – typically “crew would be staying in overseas destinations for X period of time” between journeys, but airlines will now need to consider “how are we protecting them against the risk of Covid”?

Furthermore, Kiely believes there could be “a surge in this type of claim” because of “airlines failing to ensure passengers are wearing masks”, which could have a knock-on effect for cabin crew safety.

Remote risks

Alongside the employment liability risks of attending work physically, there are also claim risks and considerations associated with home working, said Joe McManus, partner at Kennedys.

This could include claims around employees’ mental health, which may be suffering as a result of social isolation in lockdown, or health concerns arising from home-based workstation setups, including around display screen equipment (DSE). Furloughed staff may also make mental anxiety or anguish claims.

An updated, recorded risk assessment is a good tool to combat potential claims here, added McManus, as is following Health and Safety Executive (HSE) guidance.

Meanwhile, James Whitaker, partner at international law firm Mayer Brown, added: “One of the central – and probably long-lasting – impacts of the pandemic has been the large scale and remarkably quick, transition to remote working.

“Whilst the precise scope of an employer’s obligations in the world of remote working will need to be clarified, by way of official guidance, or if and when these issues become the subject of dispute and litigation (as they are likely to), it is clearly incumbent upon employers to consider, and discharge, their duty of care to remote employees carefully and, of course, to protect themselves – via appropriate protocols, liability insurance and other measures – against exposures in this regard.”

Clarifying claims potential

To establish liability for these types of claims, “there are generally three steps that have to be completed”, Le Marquer said.

“A claimant is going to have to establish that there is a duty of care, that that duty of care has been breached and that the breach of the duty has caused the loss – caused the sickness, the infection or the death,” he explained.

“In this case, establishing a duty of care is well established. Employers have a statutory and common law duty of care to their employees.

“Establishing a breach of that duty might be possible in certain circumstances [too]. Certainly, if an employer can be demonstrated not to have followed HSE guidelines or other government advice, not to have provided a Covid safe environment to work in, not to have allowed its employees to work from home when they could have done.

“There are quite clear steps which should be followed and if they’re not, then it’s probably not going to be difficult to establish a breach of duty there.”

But “causation is going to be the element where many claimants will fall down”, Le Marquer added.

“The prevalence of Covid-19 is so widespread now that it’s going to be extremely difficult for most claimants to establish that the breach of duty – the employer’s failure to provide a Covid safe environment – actually caused their infection because they will have been visiting other areas.

“Presumably, they may have been on public transport, they may have been in shops, they may have been seeing other people. It’s very difficult to prove where that infection came from.”

Future forecasting

Diskin noted that forecasting future claims trends, such as an uptick in employment liability claims, is vital amid this uncertain pandemic landscape.

One way to do this is to increase two-way conversations with commercial clients to “every week rather than once a month on pertinent issues – we’re fact finding as to what’s actually happening inside their risk profile”.

“We’re picking up all those granular issues and that will really help,” he added.

Furthermore, the sector needs to be “constantly aware of a changing landscape”, for example the extension of the government’s furlough scheme.

Diskin said: “Just constantly being aware of your surrounds and communicating that north, south, east and west in your business.

“Sometimes, the people that take that first notification of loss call in our business are the very best people to get that information from because they’re actually at the heartbeat of where the customer is in a period of distress. As well as looking at the top end as to whether financial modelling and forecasting is coming out.”

EMPLOYMENT LIABILITY CUTS

Reducing insurance spend

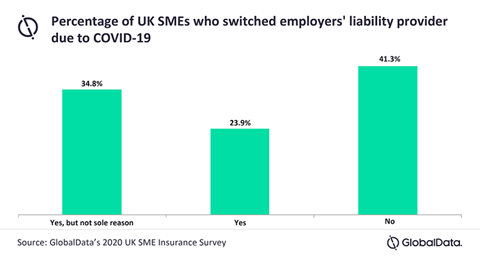

According to data and analytics organisation GlobalData, the Covid-19 pandemic is causing an increase in SME businesses cancelling or switching their employers’ liability insurance in light of the pandemic-induced economic downturn.

Its 2020 UK SME Insurance Survey found that 15% of respondents cited Covid-19 as the reason why they cancelled their employers’ liability policies in 2020; 59% switched provider last year for the same reason.

Of those who switched employers’ liability provider in 2020, 24% did so purely because of the effects of the pandemic.

Ben Carey-Evans, insurance analyst at GlobalData, said: “Employers’ liability insurance is a legal requirement for businesses in the UK, so SMEs cannot cancel it as a cost-cutting measure just because budgets are squeezed.

“However, other factors arising from the pandemic – such as rising unemployment and increasing company liquidations – mean the size of the market for employers’ liability insurers will shrink.”

No comments yet