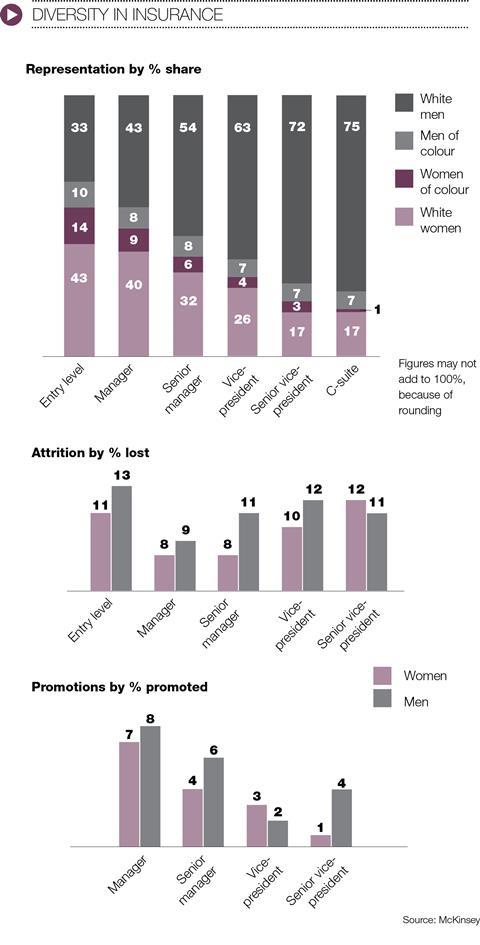

It is essential that insurance improves representation for both race and gender at all levels, to better reflect its customer base

During an increasingly bitter court battle between rivals Gallagher and Ardonagh over the alleged poaching of staff, Gallagher UK boss Simon Matson admitted using offensive racist language when describing departing energy broker Nawaf Hasan.

Liberal Democrat leader Vince Cable responded with a letter urging Premiership Rugby to drop Gallagher as a sponsor due to Matson’s “awful words”, which he said would undermine the anti-racism efforts of the sport.

The case highlights how much further there is to go to improve levels of professionalism and diversity and inclusion within the UK broking sector, according to Ashwin Mistry, Brokerbility executive chairman.

He thinks the tone should be set at the top. “All organisations should take a photograph of their board of directors and have a discussion about that photograph,” Mistry says. “The board of UK broking firms should, by and large, reflect their customer base. If its board doesn’t reflect the ethnicity and diversity of its customers then they need to ask themselves why.”

Boardrooms that are ‘pale, male and stale’ are no longer fit for purpose in an industry that is actively seeking to engage its customer base.

“If you do not reflect your customer base, you’re going to miss out on the richness of the culture that already exists and therefore you’re not reaching out to the customer base that you could do,” says Mistry. “There’s a direct business benefit of being inclusive in a whole range of ways.”

Diversity and inclusion features heavily in this year’s Biba manifesto as part of its pledge to “promote behaviours that encourage inclusivity and eliminate discrimination”.

Biba has signed up to the Treasury’s Women in Finance Charter, as well as Lloyd’s Diversity and Inclusion Charter and the Inclusive Behaviours in Insurance Pledge, among others.

Diverse organisations are more likely to attract talent and avoid succession planning pitfalls, says Biba executive director Graeme Trudgill.

“You don’t want to have ‘groupthink’ in a company,” he says. “You want to have people from diverse backgrounds and different age groups and then you have a much richer mix of knowledge.”

Women on board?

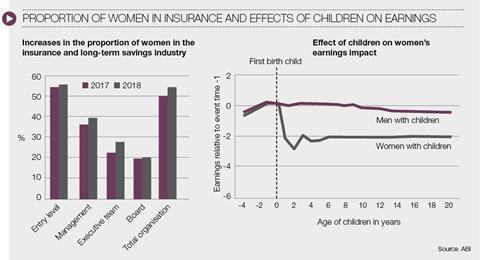

According to ABI figures, gender diversity has improved at nearly all levels of the insurance industry, with the proportion of women on executive teams increasing by 5% year on year. However, women occupy just 20% of board positions (up from 19% year-on-year). The ABI’s annual survey also found that 76% of member firms have a diversity and inclusion strategy and 61% have a mentoring programme targeted at developing underrepresented groups, and it asks: “Is the dial starting to shift?”

Not yet, according to ABI chair Amanda Blanc. Referring to research on the gender seniority gap and the ‘motherhood penalty’ she said: “While I have no doubt that many people at the top of the industry are fully committed to change, it is simply not good enough that in 2018 there are 60% fewer women at board level than entry level.”

In its research with female leadership website LeanIn.org, McKinsey found that while there are more women coming into the industry at entry level than men, this falls as positions become more senior. Among the barriers preventing women from rising to the top is a lack of support from employers in balancing family and work commitments. Entry-level women are also less likely than male counterparts to have managers acting as advocates.

But the business case for diversity is clear, with companies in the top quartile for gender diversity on executive teams outperforming their peers both in terms of profitability and value creation.

“Research shows diversity leads to better performance, more innovation, and stronger economic growth,” said Sheryl Sandberg, chief operating officer of Facebook and founder of LeanIn.org.

No comments yet