Reducing claims, reducing price, reducing the overall premium pie: is the Internet of Things an opportunity or threat?

In some personal lines business, Big Data and the Internet of Things (IoT) already help insurers and brokers reduce claims frequency and severity.

Telematics, for example, provides important information about how you drive: when you drive, how quickly you take corners, how rapidly you brake, how fast you drive on the motorway, and so on.

By extrapolating this information, telematics providers can tell you how to be a safer driver. Likewise, the use of wearable health monitoring devices offers health insurers the opportunity to feed back information to consumers, such as how to tackle high blood pressure or a sedentary lifestyle.

The connected home can alert homeowners and insurers about hazards ranging from burst pipes to intruders. Flood preparedness is another area where insurers can cut claims.

In its paper How data makes insurance work better for you, the ABI says: “Insurers have always had an interest in customers taking action to reduce their risk.

“These actions benefit both parties – fewer claims for insurers on the one hand, and happier, safer and more secure customers on the other.

“But in practice it has not always been easy for insurers to help customers this way.

“The digital revolution has the potential to completely transform this relationship, and reframe insurance as a service that helps you manage your risk, as well as paying out when things do go wrong.

“Companies that collect your data might analyse it in order to spot patterns and trends that you were not even aware of.”

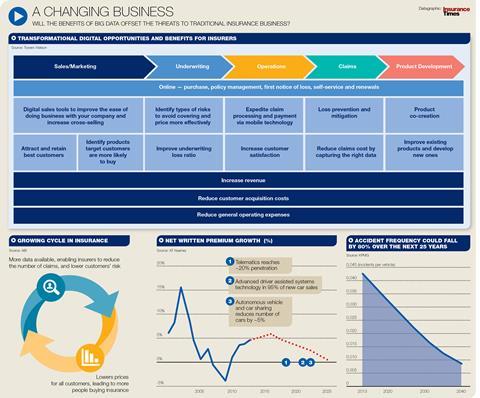

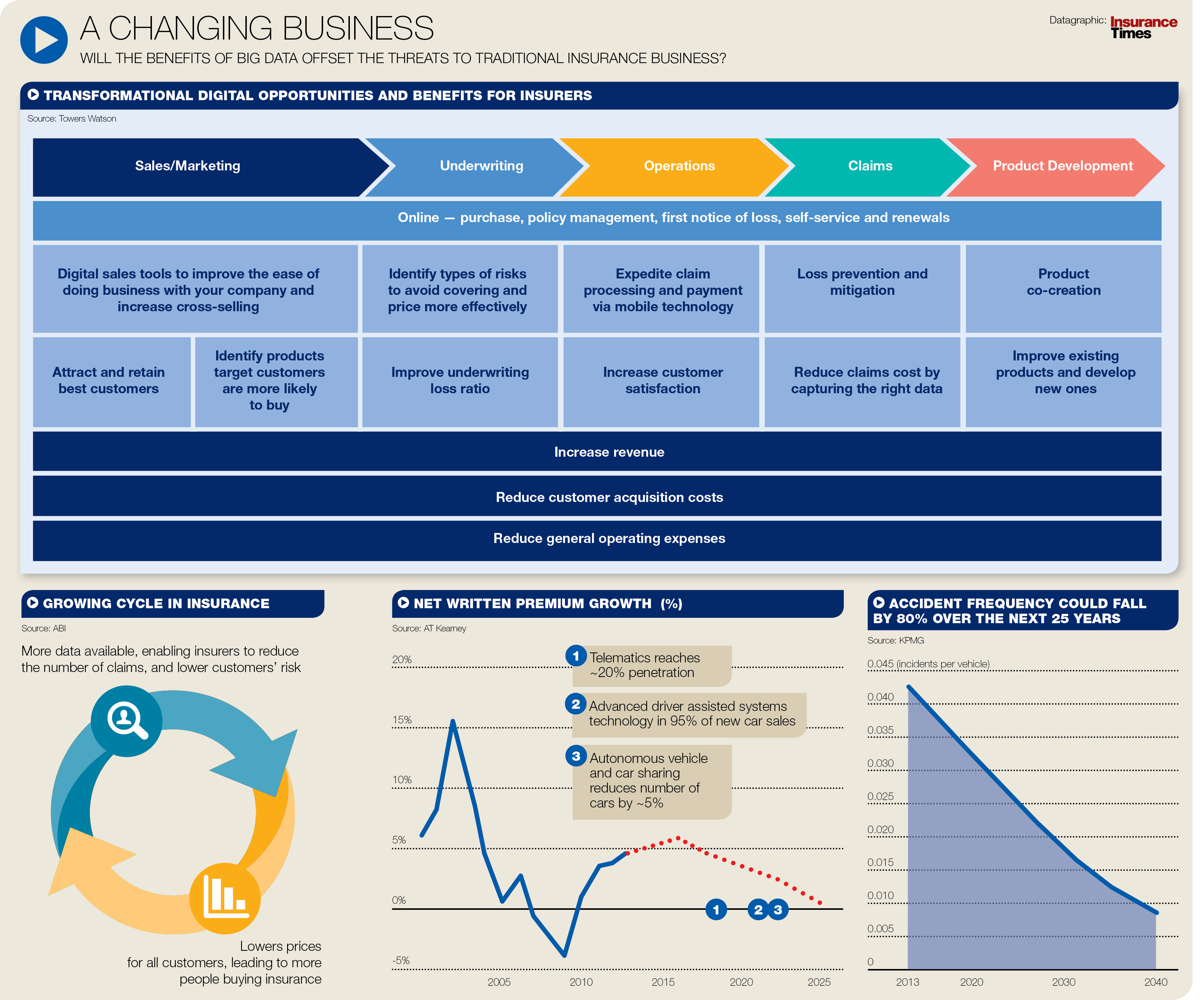

Click here for a larger version

The logical conclusion is that by improving the risk, the IoT and Big Data will cut the cost of claims and ultimately reduce premium income.

“What happens when there are (almost) no accidents?”, asked Celent director Donald Light in 2012. He predicted that autonomous cars would reduce the US auto liability sector’s share of total industry premium from 25% to 10%.

But others argue the IoT, in tandem with the digital revolution, offers more opportunities and benefits for insurers and brokers than threats. These transformational opportunities include new products (cyber, for example), services, distribution channels and loss control, increased customer engagement and improved business intelligence for better underwriting.

{kind=link}

No comments yet