Capacity slowly improves for the beleaguered waste and recycling sector as brokers and adjusters seek to provide bespoke policies

The boom in waste and recycling has been driven in recent years by government determination to make the UK a “zero waste” economy.

But the industry’s rapid growth has not been without its problems, including price volatility of commodities, and fire risk, given the susceptibility of waste material to spontaneous combustion.

As a result of the high frequency of claims, premiums shot up and some insurers – including Catlin in April 2014 – reduced capacity.

For SMEs in the sector the cost and lack of availability of insurance became a burden, with risk management requirements, such as sprinkler systems, adding costs.

Another significant issue discovered by loss adjusters was the underinsured nature of a high number of claims.

“The biggest bane of this industry, whether you’re a one-man band or global plc, is stock debris removal,” Cunningham Lindsey corporate development director Paul McLarnon says.

Many policies do not recognise waste in its raw or converted state as ‘stock’ in the traditional sense, and so waste debris removal is often uninsured. The situation is exacerbated by the additional weight of water.

“If you have a fire, the fire service comes along and douses the burning waste,” he says. “Saturation can double or treble the weight of stock that needs removing, and this isn’t insured.”

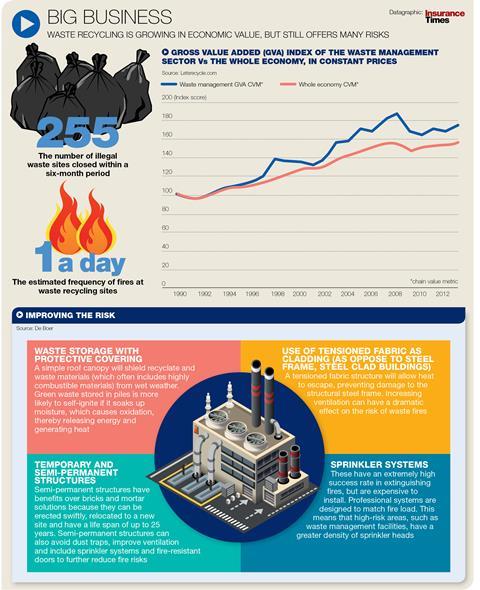

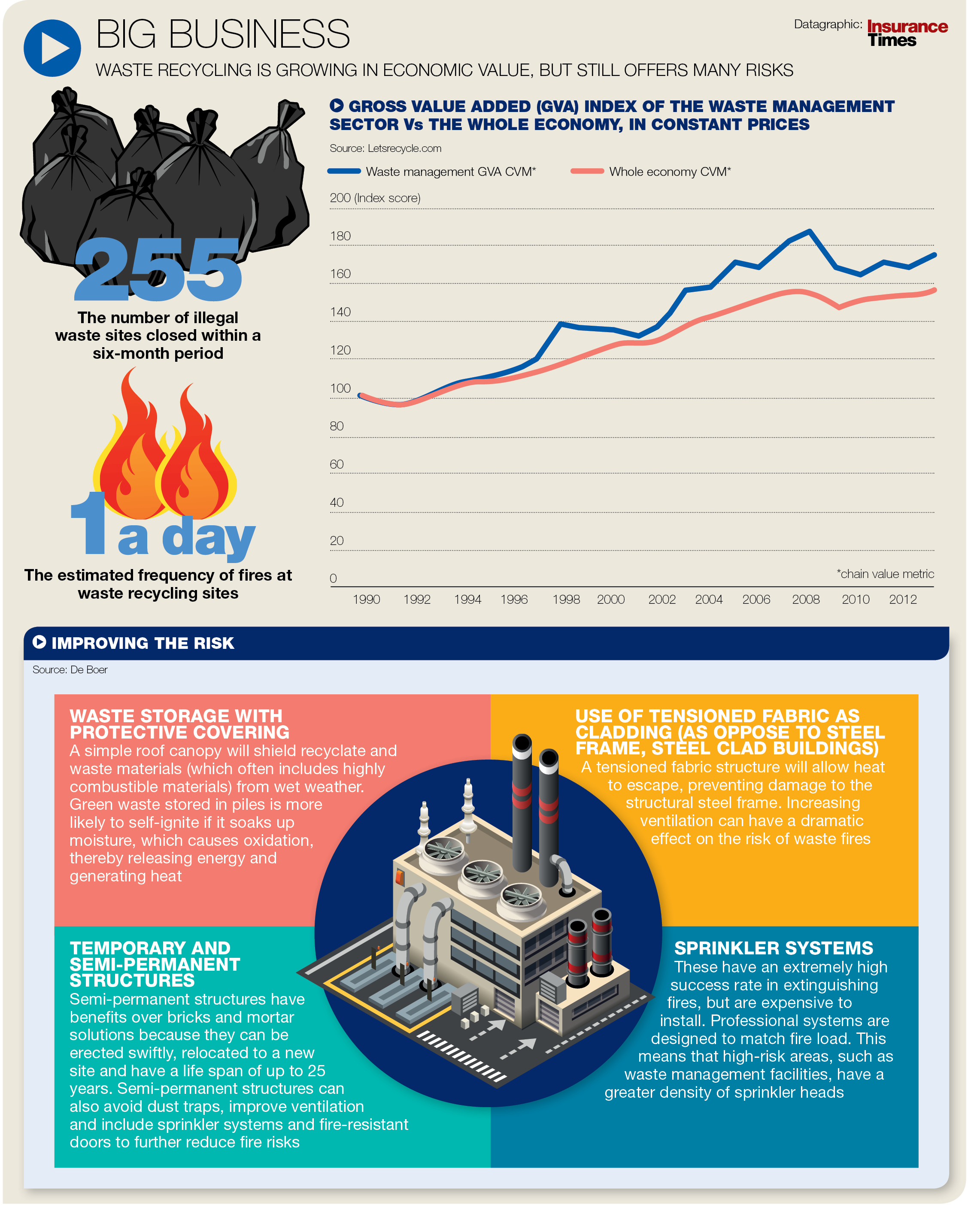

Click here for a larger version

Turning a corner

The sector seems to have turned a corner, however. Initiatives to improve risk and crack down on illegal sites are bearing fruit, with the Department for Environment, Food and Rural Affairs noting a fall in the risks posed by waste fires.

Some new specialist markets have also entered the sector, including the launch of a new scheme for recycling and waste management businesses in the UK and Ireland, backed by Hiscox, and a facility – Solon Underwriting – backed by Lloyd’s capacity for the UK, Ireland and Germany.

“It seems to have been easing, particularly for businesses with a desire and willingness to adopt further risk management, or those that have a high level of culture in this regard,” Folkestone-based Independent Insurance Services proprietor Ray Johnson says.

“Markets seem to be developing; it is common when some areas have been hit hard for others to enter.

“Waste by way of, say, paper is a difficult risk to place, but other waste processing entities can be a more attractive risk to underwriters,” he says.

“It helps that the Environment Agency and other authorities are cracking down in relation to theft/fire. Good risk attitudes prevail as companies that demonstrate best practice do not want to be in breach with these authorities either.”

Johnson estimates that around 50% of his waste sector clients are SMEs. “They can range from recyclers of scrap to vehicle components, dismantlers of electrical goods to recyclers of vegetation.”

Policies are also becoming more bespoke. Noting gaps in cover when claims arose, loss adjusters are working with brokers to ensure wording is better suited to the waste sector.

McLarnon says: “We are often the ones who deliver the bad news that a claim is not covered. So we’re highly motivated to work with brokers to find wording that works and that people can clearly understand.”

Downloads

Recycling graphic

Image, Size 2.43 mb

Hosted by comedian and actor Tom Allen, 34 Gold, 23 Silver and 22 Bronze awards were handed out across an amazing 34 categories recognising brilliance and innovation right across the breadth of UK general insurance.

{kind=link}

No comments yet