The London market could be on the brink of a fallout from the US opioid crisis as legal activity ramps up, those responsible could be slapped with up to £38bn ($50bn) to pay after the rising death toll of 134 people per day taking prescribed doses

It was the thing that killed Prince in April 2016. An accidental overdose of the synthetic opioid fentanyl left the American pop star dead at 57.

But fentanyl is just one type of opioid, it is 50 times stronger than heroin and 100 times stronger than morphine.

Now London insurers who provide cover for pharmaceutical firms accused of fuelling the US opioid crisis could end up forking out £38bn ($50) in compensation over the soaring number of deaths connected to the deadly painkillers that are addictive. But the addiction issue was downplayed and that is the basis of some legal action.

Swiss Re is now warning underwriters to be more vigilant in properly assessing, underwriting and mitigating potential exposures to their portfolios, in everything from providing cover for life sciences to product liability, directors’ and officers’, medical malpractice and health insurance.

Last year Aspen Re reported that there were more than 700 pending lawsuits in US federal and state courts nationwide, brought by government agencies and local authorities.

For insurance, the opioids epidemic has been likened to the 1990s asbestos crisis which saw Lloyd’s of London pushed to the brink of collapse.

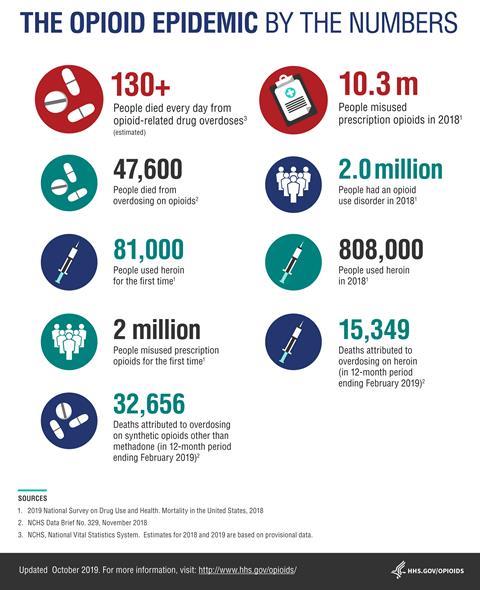

Over the past two decades there have been reportedly 400,000 opioid-related deaths in America.

However, manufacturers are still producing these drugs with significantly high potencies, leading to addiction, abuse, and deaths, as well as putting pressure on public bodies dealing with the fallout.

It is also a problem that could spread here.

Dr Teresa Bartlett, senior medical officer at Sedgwick, told Insurance Times the number of prescriptions for opioids has increased drastically in the UK over the 10 years to 2018. In 2008 there were 14 million prescriptions compared with 23 million in 2018.

Currently in the US there are 134 deaths every day from prescription opioids; this rises to 200 daily deaths for all opioids.

Bartlett also warned that claims costs could double due to the longer duration and medical expenses involved.

The concern for big pharmaceuticals, she said, is that they are facing lawsuits for allegedly misleading physicians by saying that these drugs were not addictive.

Both state governments and victims’ families are suing as they have had to pay for programmes to rectify it.

Bartlett believes some big pharmaceutical companies could face bankruptcy and that the cost of policy premiums could increase but it is unlikely that it will be an exclusion.

“From the broker perspective it will be very difficult for them to have programmes in place to manage the prescription environment,” she added.

Developing problem

In its 2018 report The US Opioid Epidemic: An Evolving Challenge for Insurers, Swiss Re stated that there are number of open questions around policy triggers.

For example, what exactly constitutes an occurrence in the context of a policy? Does each individual dose, each prescription or each person receiving a prescription constitute an occurrence?

The reinsurer said that both manufacturers and distributors have been named in litigation as a result of allegedly deceptive advertising or marketing. Some pharmacies have also faced litigation for failing to detect misuses with other medication and not warning patients sufficiently.

Chris Gamber, focus group leader – healthcare (international) at Beazley, told Insurance Times that the opioid crisis is not a single country issue, nor a single product issue. He said Beazley saw the US opioid issue beginning to develop a few years ago.

“As underwriters, our role is to ask questions about how prescriptions are issued and how the prescribing community, doctors and pharmacists, identify potential issues. We have an international book, and these issues arise across many countries,” he said.

“The precedents being set in the US in terms of the rising volume and severity of claims means we are vigilant about the risks that we underwrite in this market and careful to make decisions based on the data presented.”

Coverage disputes

Clive O’Connell, partner at law firm McCarthy Dennings, believes it will affect insurers the most as they will shoulder the cost. He said that this would be a significant hit to the London market.

“The local authorities and other government bodies in America are looking for recompense for the massive amount of money they have paid out. They are going through the court where they are seeking compensation from drug companies and they are starting to be successful,” McConnell told Insurance Times.

Pharmaceutical firms will then turn to insurers and commercial general liability (CGL) policies, and because the numbers are so big, insurers will question whether coverage was properly given leading to coverage disputes, he said.

“The terms of reinsurance contracts will be looked at very carefully indeed to see to what extent those losses can be aggregated under one event and that could impact very significantly on the way in which those claims hit London,” O’Connell added.

He said that there could be a rise in claims due to more awareness and social media. O’Connell also suspects that the London market will consult with lawyers to defend CGL claims, review reinsurance wording and work with brokers to calculate claims.

No comments yet