Aggregate revenue across the top 10 brokers for 2025 was just over £13bn – an amount that summed up brokerage across the whole top 50 brokers list in 2023 – as leaders of the broker pack double down on M&A investments to solidify earnings

The Top 50 Brokers report compiled by Insurance Times and MarshBerry is an annual project, with subsequent analysis and commentary usually centred around the shuffling and swapping that has occurred between the big names at the top of the ranking table.

Well, not this year.

For the first time ever – since Insurance Times and MarshBerry first collaborated on the Top 50 Brokers report back in 2002 – the top 10 constituents of the ranking are exactly the same as they were last year.

Positions one to 10 in 2025’s list are identical to 2024, with Howden Group well ahead in the top spot – followed by Marsh, Arthur J Gallagher, The Ardonagh Group and WTW.

This should perhaps not come as a huge surprise. As the big brokers get even bigger, so too do some of the gaps between them.

For example, six firms posted income of more than £1bn in 2025, as they did in 2024. This year, however, the gap between numbers one and two in the ranking is over £1bn. Even the two firms closest to each other in terms of figures within the top 10 are still around £50m apart – an amount that could itself amount to a Top 50 Brokers level firm.

These are big numbers to close, either organically or via M&A.

Continued growth

The big have continued to get bigger in 2025.

Aggregate brokerage across the top 10 featured brokers this year was just over £13bn. For context, the entire Top 50 Brokers list posted a similar total brokerage as recently as 2023.

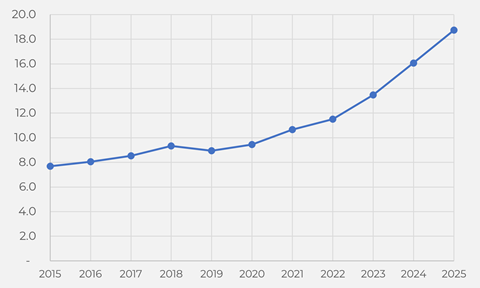

Aggregate brokerage across the top 50 firms for 2025 was £18.7bn, an increase of 16.5% over 2024. In percentage terms, this is actually the lowest level of brokerage growth recorded in the Top 50 Brokers report since 2022 – when Covid-19 impacted figures were being reported.

Has broker growth this year been affected by the soft market then? Well, no because the Top 50 Brokers report uses figures from constituents’ latest filed accounts – which in most cases is for the year to December 2024.

There is a lag effect and reported numbers within 2025’s Top 50 Brokers instalment will not yet fully reflect the softer pricing conditions the UK general insurance (UKGI) market has seen across most classes of business in 2025. This will be more fully felt in next year’s list.

Apples and oranges

The Top 50 Brokers has historically been a relatively pure domestic listing that uses UK filed accounts. As such, the figures captured for most overseas owned businesses – such as Aon and Marsh, for example – are their UK numbers.

More recently, however, a distorting effect has hit the underlying Top 50 Brokers data due to the material level of overseas acquisitions being made by UK-headquartered firms – most notably Howden Group and The Ardonagh Group. The combined income of these two businesses amounts to 23.5% of the entire recorded income across all 50 featured firms this year. PIB Group and BMS Group have also undertaken extensive overseas M&A.

These UK firms report their overseas earnings in their group numbers and have thereby introduced an increasing component of non-UK income into this annual list.

This factor – alongside the impact of domestic consolidation, exposure base growth and rate driven increases – is contributing to the double digit year-on-year growth in brokerage noted in this year’s report, running ahead of the real level of UK growth in the sector.

Consolidating consolidators and new entrants

Among the biggest broking groups featured in the Top 50 Brokers, where underlying growth is not radically different, it is M&A that really drives changes in the annual ranking.

Five names from last year’s Top 50 Brokers publication are not included this year, with four of these firms having been recently acquired by top 15 constituents.

This includes AssuredPartners UK being bought by Gallagher in August 2025, BMS Group buying David Roberts and Partners (DR&P) in December 2024, Brown and Brown snapping up Kentro Capital in October 2023 and PSC Insurance joining The Ardonagh Group fold in October 2024.

Collectively, these four firms contributed more than £250m of income to last year’s Top 50 Brokers ranking. That income – plus the firms’ growth over the past 12 months – is still included within 2025’s list, but instead resides under their buyers’ numbers.

All four firms had themselves been acquisitive and, as such, this represents a further step towards the ongoing ‘consolidation of consolidators’ trend that has been widely expected.

The fifth firm to leave the Top 50 Brokers list for 2025 is AutoProtect. Ranked as number 46 in 2024, the broker has fallen out of the ranking organically – but it may well be back as constituents at the lower end of the listing often reappear.

For example, this year’s list has seen two firms re-enter the annual ranking – Complete Cover and Alan Blunden and Co.

There have also been three completely new entries for 2025, reaching the hallowed pages of the Top 50 Brokers report for the first time. This includes ManyGroup, Marshmallow and Pine Walk.

The first two firms are both widely referred to as insurtechs – perhaps unusually, they are also both profitable. As more of the tech driven firms that have been set up in recent years come of age, similar new entrants will certainly begin to appear in this ranking.

This year’s highest new entry, Pine Walk, has made it onto 2025’s list largely through a technicality – while also growing spectacularly in recent years. It was spun out of the Fidelis Insurance Group and now – as a standalone managing general underwriting platform rather than part of an insurer – it qualifies for this list.

In the US, insurer AmTrust is currently undergoing a similar spin-out. If this trend catches on, it could potentially see a number of new entrants making their way into future Top 50 Brokers rankings.

Now and then – a decade of change

Despite the stalemate in this year’s top 10, the Top 50 Brokers is a constantly evolving list.

This year, MarshBerry turned back time to review 2015’s Top 50 Brokers edition, to see what has changed over the last decade.

Perhaps remarkably, only 20 of the 50 names on 2015’s ranking are still there in 2025. Meanwhile, 30 of the class of 2015 have left the list – but, of course, they have not departed really. For the most part, they have just been taken over by others on the list. Bluefin, A-Plan, Jelf, Swinton, Lark, Stackhouse Poland – all familiar names in 2015 and now residing in some of the largest groups featured in 2025’s Top 50 Brokers.

In 2015, only eight of the top 50 brokers were US-owned. In 2025, this number is 11. In terms of the share of overall income that is backed by US ownership, this amounts to 40% in 2015 and 46% in 2025.

This may not look like a huge change, but that can be attributed to Howden Group and The Ardonagh Group – the two aforementioned UK behemoths where overseas income is included in 2025’s Top 50 Brokers figures, partially obfuscating the real increase in US controlled brokerage over the past 10 years.

US ownership of UK brokers is likely to continue as a key market trend – several large US firms are evaluating UK acquisition opportunities and are expected to arrive in Blighty for business over the medium term.

In 2015’s Top 50 Brokers list, there were also a handful of listed and insurer-owned firms, as well as French, Belgian, Swiss and South African-owned businesses. This is no longer the case in 2025, where US and private equity (PE) ownership are almost entirely dominant, accounting for 15 firms and 43% of the ranking’s income.

However, there is an honourable cohort of UK privately held businesses on this year’s list, including stalwart constituents like Alan Boswell Group, Aventum Group, United Insurance Brokers (UIB) and Adrian Flux.

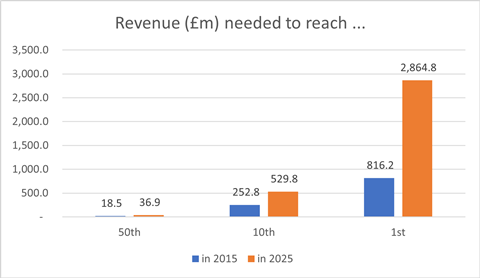

In terms of table stakes, the level of income required to actually feature in the Top 50 Brokers report has more than doubled over the past decade – to around £40m.

In terms of the number one spot, there has been a 3.5 times increase in income between Jardine Lloyd Thompson’s (JLT) victory in 2015 with £816m compared to Howden Group’s market-leading income of £2.9bn this year.

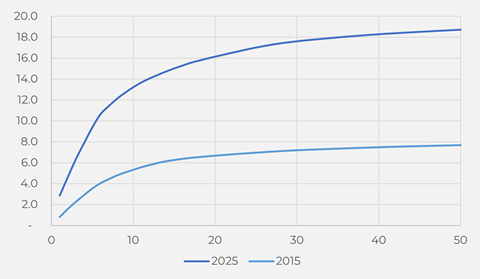

The top six firms in 2025 are all more than 50% larger than JLT was in 2015 in terms of income. Howden Group, meanwhile, is 78 times the size of number 50 on this year’s list – HW Kaufman Group. In comparison, JLT was only 44 times the size of 2015’s 50th place Cobra.

This demonstrates the widening gap at the top of this list.

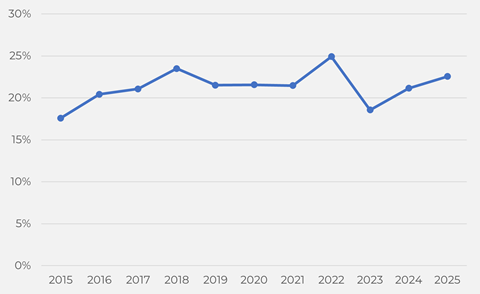

No real change in margins

In terms of average margins for earnings before interest, taxes, depreciation and amortisation (ebitda), little has changed across the Top 50 Brokers cohort for 2025 – the average continues to hover at just over 20%.

However, in truth, MarshBerry’s analysis – as well as other key performance indicators and measures of productivity – is not as revealing as one might expect.

The Top 50 Brokers is a very broad list, containing a mix of extremely different businesses and business models.

Comparing a digital motor insurance business to an MGA focused on warranty and indemnity cover, or a big London market broker, or a group like The Ardonagh Group that is engaged in almost every sort of broking business and across multiple geographies, has too many limitations to mention.

Equally, ebitda figures can be temporarily inflated or depressed for all manner of reasons in a given year.

So, although it is important to take some trends and themes with a pinch of salt, whether consolidators double down further to really entrench their Top 50 Brokers positions in 2026 will be one story to watch, among many others that help keep UKGI operating as a vibrant, profitable and interconnected marketplace.

No comments yet