Data from Insurance DataLab suggests that the FCA’s landmark regulation has not led to a measurable reduction in escalated disputes

When the Consumer Duty came into force in July 2023, it was positioned as the most significant shift in conduct regulation in a generation.

The FCA’s expectation was not that firms would simply comply with a new set of rules, but that they would rethink how products are designed, sold and serviced – with a particular focus on outcomes at moments that matter most to customers.

Since then, the industry has seen a number of regulatory reviews of the home and motor insurance markets particularly, as well as a super complaint from Which? alleging that home and travel insurance markets are delivering “systemically poor outcomes”, especially at claims stage.

It is therefore telling that despite these pressures – and nearly three years on from the implementation of Consumer Duty – there has been little evidence of a positive shift in customer outcomes.

Indeed, analysis by market intelligence firm Insurance DataLab, published exclusively by Insurance Times, has found that in some of the most scrutinised markets, progress has been hard to come by.

Using market-aggregate data from the Financial Ombudsman Service (FOS), Insurance DataLab has compared complaints volumes and upheld rates before and after the introduction of Consumer Duty on 31 July 2023.

The results suggest that, at least so far, Consumer Duty has not translated into a measurable reduction in escalated disputes.

And in some cases, the opposite appears to be true.

Home focus

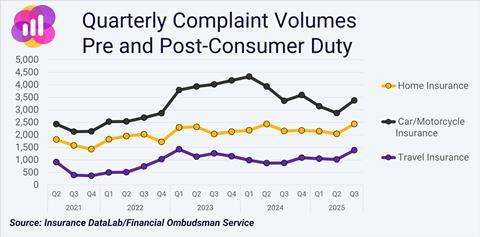

For home insurance, which incorporates both contents and buildings insurance, the volume of complaints reaching the ombudsman has increased materially since Consumer Duty came into force.

Read: FOS complaint levels climbing despite Consumer Duty reforms

Read: UKGI market returns to underwriting profit as expense management pays dividends

Explore more Data Matters content here, or discover other news analysis stories here

In the nine quarters before July 2023, the market saw an average of around 1,884 new home insurance complaints per quarter. In the post-duty period, that figure has risen to 2,193 cases per quarter.

More striking, however, is what has happened to upheld rates.

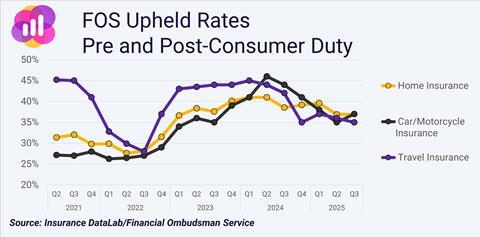

Prior to Consumer Duty, around 32% of home insurance complaints were upheld by the FOS. Since July 2023, the average uphold rate has climbed to 39%.

Insurance DataLab co-founder Dan King said that this shift matters enormously, particularly when it comes to the upheld rate.

“Upheld rates are not simply a measure of dissatisfaction – they are an external assessment of whether firms’ decisions and processes align with expectations of fairness and reasonableness,” he said.

“Our analysis clearly shows that a growing proportion of disputes escalated to the ombudsman are being resolved in favour of consumers, despite heightened regulatory focus on outcomes.

“And with the overwhelming majority of complaints relating to the claims process, this suggests the changes envisaged by Consumer Duty have not yet translated into better customer outcomes.”

A similar pattern can be seen in motor insurance, which has seen upheld rates surge by more than 10 percentage points to 40%. Meanwhile, average motor complaints per quarter have risen by more than 31% to 3,646.

Travelling in the wrong direction

The story is less marked in travel insurance, where insurers faced an average of just under 779 new complaints per quarter prior to the implementation of Consumer Duty, with uphold rates of around 39%.

Since July 2023, average quarterly complaints have increased to 871, while uphold rates have risen to just over 40%.

King added that while this analysis across three major business lines points to a deterioration in escalated customer outcomes, it would be wrong to conclude from this data that Consumer Duty has failed.

“Complaints data inevitably lags behavioural change, and many of these cases will relate to policies sold before the duty came into force,” he said.

“Nonetheless, the absence of an early inflection point does raise legitimate questions about how insurers have responded to Consumer Duty and whether enough has been done to improve processes and policies.”

Indeed, the 2025 Which? super complaint is further evidence that the industry still has some way to go.

This is especially true in the eyes of the industry’s customers, with almost 190,000 having signed a Which? petition as part of its ’End the Insurance Rip-off campaign’.

Which? has been clear that its concern is not a lack of regulation, but a failure to meet existing obligations, citing “systemic problems with how policies are sold and explained and also with how claims are then handled”.

Reputational risk

For insurers, the challenge posed by Which? is as much reputational as it is regulatory.

Claims handling is where the value of insurance is ultimately tested and persistent disputes risk reinforcing a public narrative that insurers are difficult to deal with when customers need them most. That narrative has proved resilient and complaints data continues to provide an empirical lens through which it is assessed.

In its formal response to the super complaint, the FCA accepted that there are serious issues to address, accepting that “firms must do more to meet the standards we set in our Consumer Duty”.

However, the FCA stopped short of launching a full market study or committing to broad, sector-wide intervention. Instead, it pointed to existing and planned work under Consumer Duty, alongside targeted supervisory action and enforcement where necessary.

The implicit message is that Consumer Duty, if properly embedded, should be capable of addressing the problems identified. But that change will take time.

The FCA has already taken action against some providers. This includes two enforcement investigations and independent reviews of three firms’ claims handling systems and controls through s166 reports.

The regulator has also asked senior managers at three firms to strengthen their systems and controls, and 13 out of 15 insurers they sampled to review how they handled storm claims and cash settlements. Yet reputational pressure does not operate on regulatory timetables and sustained evidence of friction risks narrowing the FCA’s room for manoeuvre.

Insurance DataLab has also analysed the latest complaints data with the FCA, finding that response times have slowed across the board since the introduction of Consumer Duty.

Across all lines of business – excluding PPI – the proportion of internal complaints being closed within three days has fallen from an average of 49% for the two years before Consumer Duty came into force to 45% for the two years after implementation. Meanwhile, the proportion closed within eight weeks has risen to more than 49% from 45% prior to implementation.

But complaints data occupies an awkward space in this debate. Claims acceptance rates can look healthy and firms may point – with justification in some instances – to the majority of claims being paid.

After all, more than 80% of travel insurance claims were accepted according to the most recent FCA Value Measures data for 2024. But in buildings and contents insurance these figures stood at just 63% and 74% respectively.

It is also worth noting that these still sit well-below the figures for other major markets such as motor (99%) and pet (88%-95% depending on type of cover).

King noted that all of this goes directly to the outcomes Consumer Duty was designed to improve.

“Complaints, particularly those upheld by the Ombudsman, highlight where decisions, explanations or processes fail to meet external expectations,” he said.

“In that sense, the post-Consumer Duty increase in upheld rates across both home and travel insurance is difficult to dismiss as mere noise.

“And when taken alongside these less than stellar claims acceptance rates and slower response times, it is clear that insurers need to be doing more to improve customer outcomes.”

For now, the FCA appears content to allow Consumer Duty and targeted supervision to do the heavy lifting. Whether that patience can be sustained will depend, in part, on whether the data begins to show improvement.

Nearly two years on, the evidence suggests that, at least at the point of escalation, outcomes have not yet shifted in the way many had hoped.

Consumer Duty set out to raise standards across financial services. In home and travel insurance, the complaints data suggests that the journey is still very much in progress – and that the market has yet to demonstrate, at scale, that outcomes have materially improved where it matters most.

No comments yet