Market intelligence firm pinpoints the best performing business lines in UKGI, while warning that the ‘diverging fortunes’ between firms’ expense and loss ratios can make or break sustainable profitability

The UK general insurance (UKGI) market returned to underwriting profitability in 2024 for the first time since 2021, according to the latest research by market intelligence firm Insurance DataLab, published exclusively by Insurance Times.

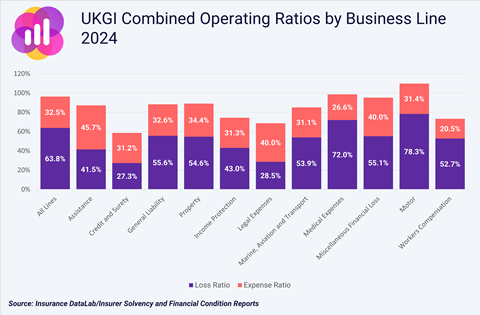

This research, based on an early analysis of insurer Solvency and Financial Condition Reports (SFCRs) ahead of the 2025 edition of Insurance Times’ Top 50 Insurers report being published this October, revealed a market-wide aggregate combined operating ratio (COR) of 96.2% for 2024.

This is the best underwriting result since Insurance DataLab started analysing insurers’ SFCRs in 2017 and is around six percentage points better than the loss-making 102.2% COR reported by the market in 2023.

The decisive factor behind this improvement has been the industry’s success in driving down operating expenses and boosting efficiency savings, with the overall expense ratio improving every year of this annual analysis to reach 32.5% in 2024.

This means that insurers have knocked a combined 7.3 percentage points off their aggregate loss ratio since 2020.

While UKGI’s loss ratio has improved slightly over the past year – the 2024 loss ratio of 63.8% was 1.8 percentage points better than 2023’s 65.6% – this follows two years of rising losses, which means the aggregate loss ratio is now 4.3 percentage points higher than it was in 2020.

The diverging fortunes of these two ratios underpins the importance of managing operating costs in what can be a very volatile market.

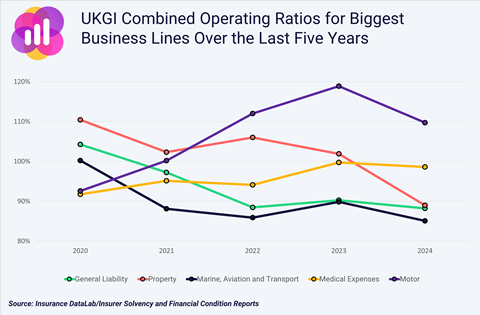

Indeed, the weaker business lines featured in this analysis have been characterised by wide swings in their loss ratios. Motor, for example, has seen its loss ratio fluctuate across a range of almost 20 percentage points over the past five years, while medical expenses’ loss ratio has also risen steadily over the same reporting period, from less than 60% to the low 70% bracket.

By contrast, expense ratios in these poorer performing classes have stayed within a relatively narrow band, with only marginal changes year-on-year.

These figures are starkly different to the best performing UKGI lines, where insurers have managed to reduce expenses by more than 10 percentage points since 2020.

This highlights how sustainable profitability has been built by improving the cost base, while lines that rely solely on favourable claims trends to deliver results remain exposed to shocks from ongoing claims inflation.

Which are the best performing lines in UKGI?

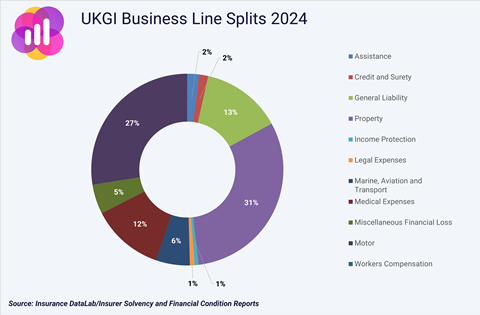

When it comes to individual business lines, property insurance remains the largest, with gross written premium (GWP) of £18.4bn in 2024. This means it now accounts for almost a third of the UKGI market with 31% of total premiums.

This business line also swung massively back into underwriting profitability last year after knocking 12.9 percentage points off its COR to report a ratio of 89%.

This uptick in performance was underpinned by an 8.5 percentage point improvement in the expense ratio to 42.9%, while the loss ratio fell 4.4 percentage points to 54.6%.

This latest result for property insurance follows four consecutive years of underwriting losses and marks the best COR for property insurers since Insurance DataLab began analysing the market in 2017. Indeed, the only other year property insurers reported a sub-100% COR across this reporting period was in 2019, with a ratio of 99%.

This market will also have been buoyed by significant price increases seen in recent months.

For example, Consumer Intelligence’s August 2025 Home insurance price index showed that these premiums rose for 18 consecutive months up until the end of September 2024. These premiums then remained consistently high before beginning to fall at the turn of the year.

Motor fails to turn a profit

The second biggest business line in UKGI is motor insurance, with GWP of £16.3bn – equal to 27% of total market premiums in 2024.

The motor market has endured similarly challenging market conditions to property in recent years – and although the sector reported a 9.2 percentage point improvement in its COR for 2024, motor insurers remain firmly in loss-making territory.

Indeed, the 109.7% motor COR for 2024 is the fourth consecutive year of underwriting losses for motor insurers. These companies have failed to make an underwriting profit in five of the last eight years.

This persistent underperformance reflects the continued pressure of repair cost inflation, supply chain disruptions pushing up the price of parts and availability of labour, as well as ongoing challenges in the bodily injury claims environment.

These structural issues have made it difficult for motor insurers to translate premium growth into underwriting profit.

This means that motor insurance is the only class of business in UKGI to fall to an underwriting loss in 2024, with a COR some 11.1 percentage points higher than the second worst performing business line, medical expenses, which recorded a COR of 98.6% last year.

The motor market can, however, take some comfort from a 9.4 percentage point improvement in its loss ratio to 78.3%, although this does still remain the highest loss ratio across all lines of business. Medical expenses was the only other business line to report a loss ratio north of 70% (72%).

Motor insurers do, however, have one of the best expense ratios in UKGI, aided by the mass market nature of the product line.

It is worth noting though that the motor market’s 0.3 percentage point increase in its expense ratio means motor is one of just three business lines to see expenses increase, alongside legal expenses (1.2 percentage points) and miscellaneous financial loss (4.1 percentage points).

Liability continues profitable run

General liability business also forms a sizeable part of the UKGI marketplace, with £8bn in GWP recorded in 2024, which is equal to 13% of total premiums.

General liability insurers reported a highly profitable COR of 88.2% for 2024, meaning that this class has now reported an underwriting profit in each of the last four years.

This latest result also represents a 2.1 percentage point improvement on the previous year, driven by an 8.6 percentage point improvement in the expense ratio to 32.6%.

Despite these improvements, the aggregate loss ratio for general liability rose by 6.6 percentage points to 55.6% last year – the third highest result across all business lines.

The new format of SFCRs introduced under the Solvency UK rules, effective from December 2024, mean that it is also now possible to explore the individual business lines within general liability in more detail.

This new analysis found that public and product liability leads the way with a COR of 84.6%, followed by professional indemnity insurance (88.2%) and employers’ liability (90.5%). Other classes of business under general liability reported a COR of 91%, meaning that all individual lines reported an underwriting profit.

The only other line to report a double digit share of the UKGI market is medical expenses, with GWP of £7.2bn – this amounts to 12% of total market premiums.

Medical expense insurers continue to record underwriting profits, albeit at a more marginal level in recent years, having reported a sub-100% COR in each year of this analysis.

A COR of 98.6% for 2024 is 1.1 percentage point better than 2023 – although this is still higher than the three preceding years, when COR ranged from 91.7% to 95.1%.

Specialty lines lead the way

The best performing of the major lines in UKGI is marine, aviation and transport. Its GWP of £3.4bn, accounted for 6% of the market in 2024.

Its COR of 85.1% is comfortably the best performing ratio of the five largest business lines and represents a 4.7 percentage point improvement on the 89.8% COR reported for 2023.

This improvement was driven by a 10.6 percentage point improvement in the expense ratio, which more than offset a 5.8 percentage point increase in the loss ratio, driven by net claims incurred rising by more than 10% to top £700m.

Efficiency gains must be matched with claims resilience

Looking ahead, the key challenge for many insurers will be sustaining these hard won efficiency gains in an environment where there is continued pressure on claims costs.

The ability to keep driving down operating expenses while investing in further improvements across the insurance value chain will define whether 2024’s return to profit proves to be a turning point or a short-lived reprieve.

And while tighter expense management has delivered strong benefits in recent years, that does not mean insurers can take their eye off the ball when it comes to claims.

With claims inflation still exerting pressure on loss ratios and pricing dynamics shifting across the market, the sector’s resilience will also hinge on maintaining cost discipline in what remains a fine balancing act between growth and maintaining the bottom line.

And, with the market seemingly more competitive than ever, those that get it wrong could find themselves falling back into loss-making territory very quickly.

No comments yet