Insurance DataLab reveals the preliminary findings of its 2022 MGA performance report exclusively in Insurance Times, rating the performance of MGAs based on their financial performance

We live in increasingly uncertain times. Today, it seems just as hard to predict who the prime minister will be next week as it does to evaluate the future of the insurance market.

For MGAs operating in this uncertainty, there are a number of headwinds to deal with, including changing regulation, rising claims inflation or a tightening capacity crunch.

All of these challenges mean that - for some MGAs - growth has been hard to come by.

Indeed, analysis from Insurance DataLab’s inaugural MGA performance report – published in November 2022 – highlighted that MGA growth has slowed in recent years.

The 52 MGAs rated by the market intelligence firm for the report received an average growth rating of 49.4% for 2022.

This marked a 2.2 percentage point decline on 2021, when the MGA market received an average growth rating of 51.6%, and is also lower than 2020’s average growth score of 53.8%.

This growth slowdown was driven by faltering revenue growth, with the 2022 cohort of MGAs rated by Insurance DataLab reporting aggregate revenue growth of 4.1% over the course of 2020/21, alongside revenues in excess of £660m.

This is down from revenue growth of 14.4% and 23.5% in each of the previous two years.

Despite this revenue result, MGAs’ growth in operating profits has remained relatively healthy.

The aggregate operating profit for the 2022 cohort of MGAs rose by 44.6% to £66.3m for the 2020/21 financial year, after operating costs grew by less than 1% over this period to £593.7m.

This is, however, still slower than the 54.8% growth in aggregate operating profit these companies recorded over the previous 12 months – but 2020/21’s uptick is also much higher than the 5.7% growth in operating profits reported for 2018/19.

Productivity uptick

When it comes to overall profitability, however, the average Insurance DataLab profitability rating – based on each MGA’s three-year aggregate earnings before interest, taxes, depreciation and amortisation (ebitda) margin – has remained relatively steady over the last three years.

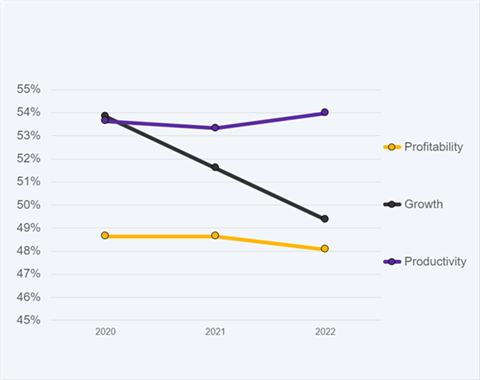

Indeed, the market average for this measure stood at 48.1% for 2022, down marginally from 48.6% in both 2021 and 2020, with lower ebitda margins from 2019 still pulling down the three-year aggregate position, despite improvements in recent years.

The news is better, however, when it comes to the productivity of MGAs, with the average Insurance DataLab rating under this metric climbing to 54% for 2022 - up from 53.3% in 2021 and 53.6% in 2020.

This productivity rating is the central figure of the three pillars used by Insurance DataLab to assess MGA performance in each of the last three years.

The MGA market performed best in terms of staff costs as a percentage of turnover, receiving a standardised score of 64% for 2022. Aggregate staff costs for the 2022 cohort of MGAs accounted for 42% of turnover.

When it comes to turnover per employee, the average standardised score for the MGAs in this research stood at 46% for 2022 – this year’s cohort of MGAs brought in an average of just over £138,000 per employee.

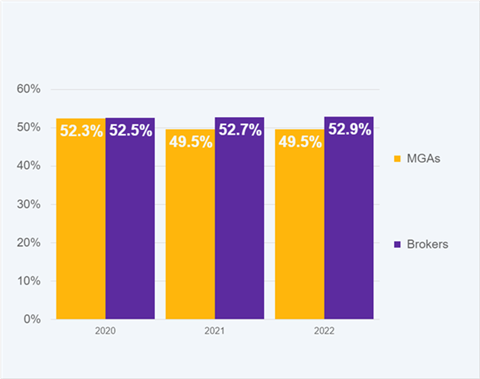

Despite the slight improvements in productivity, this was not enough to boost the MGA market’s overall performance, with the average Insurance DataLab MGA performance rating standing at 49.5% for 2022 – consistent with the rating received for 2021, but some 2.8 percentage points lower than the 52.3% average rating for 2020.

This drop in the average performance rating also means that MGAs have now fallen behind brokers when it comes to financial performance.

Brokers received an average rating of 52.9% for 2022 in Insurance DataLab’s inaugural Broker performance report. Published in May 2022, this report used the same methodology as this analysis, but for rating brokers.

Brokers’ performance rating was 52.7% and 52.5% for 2021 and 2020 respectively.

Read: When it comes to financial performance, does bigger really mean better?

Explore more news analysis here.

Is bigger really better?

But how does financial performance compare when it comes to the size of an MGA?

To help answer this question, Insurance DataLab categorised MGAs into three different size bands according to their revenue for the 2020/21 financial year. These are:

- Small: Revenues of £5m or less.

- Medium: Revenues of between £5m and £15m.

- Large: Revenues in excess of £15m.

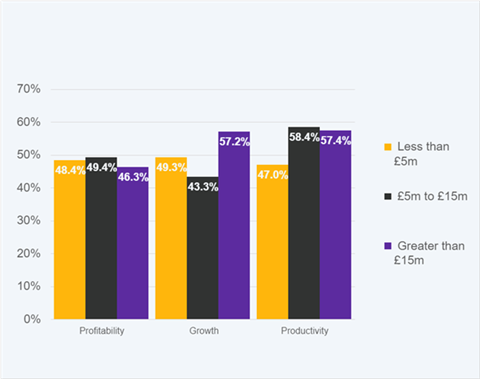

When it comes to overall performance, the larger MGAs performed better, picking up an average Insurance DataLab MGA performance rating of 52.9% for 2022, compared to average scores of 48.8% for medium-sized MGAs and 48.5% for smaller MGAs.

This trend held over the course of this analysis, despite the average score for larger MGAs falling from a high of 56.3% in 2020. MGAs with revenues in excess of £15m outscored their smaller peers across each of the last three years.

Larger MGAs also performed best in terms of growth, picking up an average growth rating of 57.2% for 2022 – around 7.9 percentage points higher than the 49.3% average score received by small MGAs and 13.9 percentage points higher than the 43.3% score for medium-sized MGAs.

Despite this outperformance relative to the rest of the market, the growth of these larger players has slowed over the last couple years – following a similar trend to the market as a whole.

The average growth rating for large MGAs has fallen by 6.2 percentage points since 2020, when it stood at a high of 63.4%.

The growth scores for smaller and medium-sized MGAs have also been on the decline since the start of this analysis - falling 0.7 and 8.3 percentage points respectively since 2020.

When it comes to productivity, however, it is not the larger MGAs that come out on top. Instead, it is the medium-sized MGAs with revenues between £5m and £15m that trump the other size categories.

In 2022, the medium-sized MGAs reviewed by Insurance DataLab received an average productivity rating of 58.4%, one percentage point above the 57.4% rating for large MGAs and 11.4 percentage points ahead of the smallest MGAs.

This marked a change in fortune for medium MGAs compared to 2020, when a productivity rating of 58% saw them fall behind their larger counterparts by three percentage points.

Meanwhile, when it comes to the profitability pillar of Insurance DataLab’s analysis, it is the medium-sized MGAs that once again come out on top with a profitability rating of 49.4% for 2022.

Large MGAs, however, received the lowest rating under this measure, with a score of 46.3% - this is some 2.1 percentage points behind the small MGAs, which received an average profitability rating of 48.4%.

Over each of the last three years, MGAs with revenues in excess of £15m have scored the lowest in terms of profitability, with the smaller MGAs coming out on top in 2020 with a score of 49.2%.

This is 0.2 percentage points higher than 2021, when small and medium-sized MGAs tied for the top spot with an average profitability rating of 49%. This compared to 47.9% for the large MGAs cohort.

This shows that while growth may be easier to come by for larger MGAs, the margins they are able to deliver when it comes to profitability may not be as great as those smaller players at the lower end of the revenue bands.

And for those smaller players looking to make their way up the ladder, it will be interesting to see how they approach the challenge of finding sustainable growth while also maintaining their margins.

Methodology

The performance metrics used for this research have been calculated using Insurance DataLab’s own analysis of MGAs’ company accounts filed at Companies House, which takes into account both short and long-term performance over the last three years of trading.

The three metrics used to calculate the overall Insurance DataLab MGA performance rating are:

- Profitability: Insurance DataLab calculated the three-year aggregate earnings before interest, tax, depreciation and amortisation (ebitda) margin by dividing the aggregate ebitda figure by the aggregate revenue generated over the last three years.

- Growth: Insurance DataLab calculated a growth metric comprised of a weighted average of the growth in revenue over the last 12 months and the growth in operating profit over the same period.

- Productivity: Productivity has been assessed by looking at staff costs as a percentage of turnover over the last 12 months, as well as the turnover generated per employee over the same period.

Each metric has subsequently been standardised to create a percentage score for each MGA, with a weighted average used to create Insurance DataLab’s overall rating.

No comments yet