The hype cycle is masking the true ‘enabling’ potential of insurtech, says Sam Evans, founder of Eos Venture Partners

In the future, Insurance will be bought, sold, underwritten and serviced in a fundamentally different way. That creates opportunities for industry leaders – and problems for industry laggards.

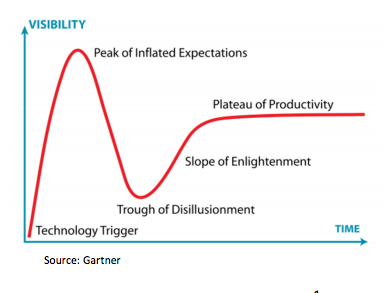

As insurtech continues to impact the insurance sector, it is clear that we are still in the initial stages of what Gartner terms the ‘Hype Cycle’, with an ever increasing amount of noise and expectation without clear impact and results.

Have we reached the peak of inflated expectations? We expect not.

Certainly, valuations continue to rise with relatively new businesses still effectively at pre-revenue stage, commanding valuations in the tens of millions – hard to justify on any fundamental level.

However, at the core of insurtech, we continue to see a huge opportunity to innovate a sector that is ripe for change: lack of customer engagement, lack of customer trust, outdated and legacy infrastructure combined with traditional and unpopular products all highlight the need for change, and the underlying potential.

Ignore insurtech at your own risk

Eos, the UK’s first dedicated insurtech fund, has talked with dozens of insurance companies, and there is a wide range of responses from the insurance community about when, where, if and how to engage with insurtech. The top insurance companies have for the most part, followed a two-phase approach combining an innovation team with a corporate venture initiative.

These carriers see the impending disruption clearly, and want to be able to shape and influence the impact. The results so far have been mixed as some large incumbents have found it difficult to circumvent legacy mind-sets, governance, organisational structures, and technology.

Have we reached the peak of inflated expectations? We expect not.

Other carriers have yet to agree/settle on an approach to deal with these disruptive forces. Eos calculates that the impact of insurtech is at least 40% to the average carrier; we calculate that by looking at a 20% upside, and a 20% downside scenario – on a conservative basis, insurers may risk losing at least that much of their business to disruption.

On the flip side, for those that embrace innovation there is an opportunity to grow their business by 20%. Stated another way, the net present value of insurtech is $100m for every $1bn of premium on the downside and $285m on the upside, assuming a top line and profitability improvement. Timing is also key as the scale of adoption and impact is not linear. The upside opportunity by investing now in the right opportunities is likely to give an insurer a lead that others can’t catch — essentially a “first-mover” advantage.

At the same time, the lost opportunity by delaying is exponential not linear.

There are many ways to create and capture value

The positive momentum is further driven by the growth of insurtech into all areas of the value chain and across multiple product lines.

We see two broad types of innovator: the ‘enabler’ and the ‘disruptor’. The enabler, is a business that significantly improves an existing part of the value chain driving efficiency, improved customer satisfaction and/or better customer outcomes.

A great example is RightIndem that is transforming the claims process by creating an end to end customer managed claims process. The disruptor, is a business that has developed a new approach to fulfilling part, or all, of the value chain. For example, this is illustrated by Insure A Thing, an insurtech startup that has created a new way of providing insurance without the need for an upfront premium (Disclosure: Eos is an investor in both these businesses).

The value of insurtech is $100m for every $1bn of premium on the downside – and $285m on the upside.

At face value the disruptors may appear more exciting, but the enablers perhaps better illustrate the underlying potential of insurtech as there are an abundance of opportunities for most insurance companies to hit ‘the low hanging fruit’ and do things better, more cheaply and more aligned with the customer.

Insurtech is not an overnight revolution and there are many ways to create and capture value that combine different elements of the above, for example:

- Low hanging fruits - these are mostly your enablers

- True differentiators - a combination of enablers and disruptors

- Measured bets for the future - all pure disruptors

What investors are focusing on

At Eos, we continue to adapt and evolve our investment strategy to take advantage of these opportunities, with an initial focus on our three core platforms:

- Digital distribution

- Frictionless Claims

- Artificial intelligence for risk selection, underwriting, pricing & capital optimisation

All of the above underpin our first trend and belief that the future of insurance will look very different to today, with all areas of the value chain from distribution, underwriting, products, claims and customer engagement changing fundamentally:

- Bought differently: As asset ownership (cars, homes) mobility and cross-border employment evolve with the shared economy, insurance covers (at least, personal lines initially) will be bought on a just-in-time, on demand, needs basis. Greater information transparency on the buyer and seller side will enable direct interaction with lower cost of intermediation/brokerage. We see this starting with simpler personal line covers and gradually evolving to more complex risks.

- Sold differently: Insurance will be quoted, bound and issued at points of transaction/ sales/ service enabled by ubiquitous IoT, telematics and external data availability. Selling will become increasingly distributed and linked to companies with strong customer engagement across both B2C and B2B sectors.

- Serviced differently: End consumers will choose how to be serviced and made whole via a channel, time, and a manner of their choice. Servicing, especially claims, will focus on ‘delivering on the customer promise’ as an integral part of the policy.

Sam Evans is founder of Eos Venture Partners, the UK’s first specialist insurtech fund. It has offices in London, Guernsey and Philadelphia, and affiliates in Palo Alto and Hong Kong. Sam will be speaking at Innovation and Disruption 17 next month. To find out more, click here.

No comments yet