Part two of our commentary on post-Covid M&A prospects

Briefing by Saxon East

Last week Saxon East wrote ’The City loves RSA again, a new era or another false dawn?

Here in part two of the RSA Briefings, he examines the prospect of RSA being acquired.

The annus horribilis drags on. Insurers are in the dock for unpaid business interruption claims and their share prices have fallen considerably.

But when this pandemic is finally over, attention will once again focus on insurance M&A.

Enter RSA and Allianz.

Reasons for Allianz & RSA deal

RSA is expected to manage the pandemic claims well and make a strong recovery right through to 2022, according to analysts’ latest view on RSA.

Allianz is also expected to come through these Covid claims relatively unscathed, with large cash reserves - even if there are some London law firms teaming up to get business interruption claims paid.

Allianz has shown its appetite for UK deals, having successfully snapped up the UK general insurance arms of LV= and Legal and General.

A deal for RSA would be a considerable step up, but Europe’s largest insurer easily has the size and firepower to make this deal happen.

The reasons for acquiring RSA are compelling:

- RSA has a strong footprint in Scandinavia, with healthy underwriting profits. Allianz is underweight on this region.

- The RSA Canada business is strong, and would complement Allianz’s footprint in the North America region

- Even though the RSA UK arm has shrunk in recent years, there could still be significant cost savings from a merger with the UK business.

- RSA is now so small compared to Allianz, it would be considered a ‘bolt on’ deal. A medium-sized deal is unlikely to arouse much objection from Allianz’s stakeholders.

- RSA pension liability could be de-risked by transferring it to a specialist, or it could simply be absorbed into the far bigger Allianz business.

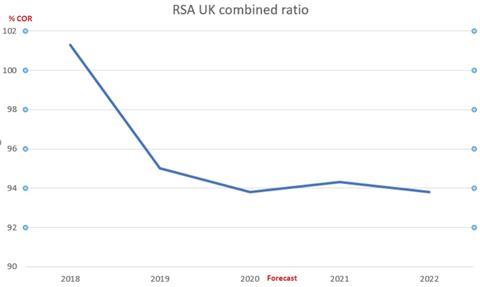

Another major plus is that the once troublesome UK and International arm is returning to strength.

It has been shrunk by chief executive Stephen Hester with the aim of improved underwriting profits, and now managed by Scott Egan, it is expected to undergo significant combined ratio improvement (See graph below).

Allianz realistically remains the only big European insurer with the appetite for a deal.

Zurich is unlikely to go there again having had its fingers burned with a failed bid five years ago, AXA has its hands full with the XL merger.

A merger between Aviva and RSA has been mooted, but this seems unlikely.

It would be a complex merger between two insurers with legacy issues - even if it got past UK competition watchdogs.

Aviva has its own strategic pathway to follow, with some calling for a break up to enhance shareholder value - an idea chief executive Maurice Tulloch has shown no real signs of supporting.

Allianz chief executive Oliver Baete has watched European rival AXA make a major deal with XL Catlin

So Allianz is the front runner.

Clearly price would be a major consideration.

RSA share price is currently at 407p. If it hovers round the 500p mark that might be a good entry point for a deal.

RSA shareholders might accept a premium on this price, while Allianz may feel there is value, especially if the sterling drops post-Brexit against the Euro.

A deal would provide a neat exit for RSA chief executive Stephen Hester after six years at the helm.

For Allianz boss Oliver Baete, this would be a low to medium risk acquisition that sensibly expands its footprint in property and casualty. It also builds on its previous deals in the UK market.

Allianz has the firepower to make it happen. The only question is whether it has the desire.

Not a subscriber? Become a subscriber and access our premium content

The insurance landscape is evolving. Click here to have your say. Brokers how well have your insurance partners supported you over the last 12 months?

No comments yet