As catastrophes wreak havoc across the world, (re)insurers face yet another learning curve

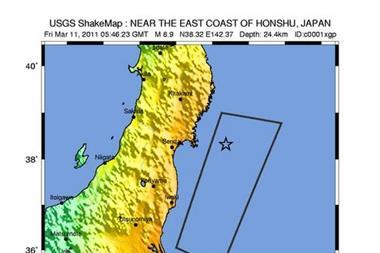

The past 18 months have proved a whirlwind of activity as 2010 claimed high fatalities and huge losses for the industry. And the frenetic pace shows little sign of slowing. The 6.3-magnitude earthquake in Christchurch, New Zealand, in February, followed more recently by the 9.0-magnitude quake and tsunami in Japan, have kick-started another hyperactive year.

A total of 950 natural catastrophes were recorded last year, of which 90% were weather-related. This makes 2010 the year with the second highest number of natural catastrophes since 1980 and exceeds the annual average for the past 10 years (785 events per year). Overall losses amounted to $130bn (£80bn), of which about $37bn was insured.

According to Munich Re, this puts 2010 among the six most loss-intensive years for insurers since 1980. “The year 2010 showed the major risks we have to cope with. There were severe earthquakes. The hurricane season was also eventful – it was just fortunate that the tracks of most of the storms remained over the open sea,” Munich Re reinsurance chief executive Torsten Jeworrek says.

Such activity has posed many challenges to reinsurers handling claims from large catastrophes – issues related to specific events, claims practices, squabbles with cedants over policy wordings, and accessing the correct data to determine overall losses.

Assessment challenge

Access to data and data mining techniques have improved dramatically in the past few years. Satellite technology and aerial mapping, for example, can help reinsurers determine the scale of damage and losses more quickly than ever.

Lloyd’s senior claims manager Phil Godwin says: “Over the past five to 10 years, the sophistication of data capture in the market has accelerated considerably. You now have risks geo-coded, so you know exactly the latitude and longitude of where that risk exists.”

Yet despite such improvements in data collection, some catastrophes prove far more complex than others. Earthquakes in general are much trickier for reinsurers than windstorms, making loss assessments difficult.

“With hurricanes, there is a reasonable expectation that most of the damage will be visible. But with earthquakes, there’s a high probability you are going to have structural damage that is hidden from sight,” says Godwin.

RMS chief research officer Robert Muir-Wood believes the biggest catastrophes are not always the most complex. Chile was last year’s most expensive natural catastrophe and the fifth strongest ever measured, with overall losses of $30bn and insured losses of $8bn. But the potential damage was mitigated by Chile’s strict building codes, which take account of the country’s high earthquake exposure, and the lack of severe secondary effects such as after shocks.

Projected settlements

But even if the event itself is straightforward, the systems within the claims processes can still bring trouble.

Godwin says reinsurers need to be careful of the rules and procedures surrounding projected settlements. Following 9/11 and Hurricane Katrina, projected settlement clauses in contracts have increased to allow reinsurers to advance settlements to the cedant company before the final loss assessments are calculated. The aim is to assist cedant companies that face cashflow problems after a catastrophe.

Godwin says reinsurers should have the processes in place to ensure the correct level of advanced payments have been paid out.

“The industry could enhance the quality of clauses,” he says. “It is in the reinsurer’s interest to speed up the process as the trusted reinsurance partner. But at the same time you have to create the appropriate rules around the way that money is advanced.”

Lloyd's lesson

Willis Re executive director Spencer Pardoe says LIoyd’s was not fully prepared for the Chilean earthquake because the London market did not have enough projected settlement clauses written into contracts.

He points out that a huge lesson was learnt by Lloyd’s when it was put under pressure to agree large sums on behalf of reinsurers.

“But I think the market will be better prepared. In future, there should not be many contracts out there without these clauses built in,” he says.

Lloyd’s is critical of the practice of passing advanced settlements via brokers rather than directly to the cedant company. This, argues Godwin, can create problems with currency fluctuations. “There is a great appetite to send the money direct to mitigate exchange rate issues,” he says.

But Willis Re executive director Gus Newell believes this process enhances the claims process following catastrophe losses. “With money going through the broker, it should avoid time-and resource-consuming reconciliation issues down the line.”

Ground control

Disputes over claims practices aside, reinsurers face ongoing challenges in ensuring they have enough expertise on the ground in the aftermath of a disaster. A dearth of loss adjusters and engineers, especially in developing countries, can delay the claims process and create problems.

The Chilean government’s strict rules over deployment of loss adjusters in the country delayed aspects of the claims process, says Godwin.

According to Muir-Wood, there were also complaints about the lack of a joined-up approach by claims handlers on the ground. “In Chile, the complaint was that every insurer had a different claims form. The industry had not got its act together in terms of a collaborative approach. It can take a large catastrophe to teach people how they can improve things,” he says.

While the logistics of the claims processes surrounding the earthquake in Chile may have presented problems, they were small compared with the complexities generated by the disasters that hit Australia and New Zealand.

This year, natural catastrophes in Australia/Oceania totalled 16% of global losses. Complex environmental factors and policy wording issues have exacerbated the difficulties for reinsurers. New Zealand’s third-largest city, Christchurch, was hit by an earthquake on 4 September 2010, but this was followed by a more deadly one on 22 February. The combined losses are expected to reach NZ$8bn-NZ$10bn (approximately £3.6bn-£4.5bn).

Reinsurers say environmental factors conspired to turn these earthquakes into a much bigger challenge. Liquefaction of the soil in New Zealand, for example, intensified the losses.

“Liquefaction is when the soil is sandy and behaves like a liquid, so there is more potential for shaking and damage,” explains Willis Re catastrophe risk analyst Rashmin Gunasekera.

All in the wording

In addition, says Muir-Wood, the policies of state-backed insurer the New Zealand Earthquake Commission are unusually worded and cover damage to the ground under which a property is built. The organisation also has a limit of NZ$100,000 per dwelling.

He believes this could create problems. “Given the connection between the two earthquakes in September and February, I think the commission will attempt to capture all the damage to an individual property under a single aggregate limit across both earthquakes. Once the damage spills over, that loss is going to be passed on to the underlying insurer of the property and then the reinsurer.”

Most reinsurers, however, will consider the earthquakes as two events. This in turn will conflict with the commission’s definition of a single event, adding complications to further loss calculations.

The saga doesn’t end there. Muir-Wood says the New Zealand government has closed down the central business district in Christchurch, which will ramp up business interruption claims. “A number of complex factors are pushing up the losses in a Katrina-like way,” he says.

How many floods?

The floods in Australia have also created a conundrum for reinsurers. As Munich Re head of claims management and consulting Nicholas Roenneberg explains, a dearth of models for flooding continues to pose challenges.

The Australian floods are also creating policy wording issues. Muir-Wood says there is uncertainty over whether the flood should be defined as a single event or a series of events. “There has been a question of the event definition used by reinsurers for what constitutes a single event for reinsurance requirements.

“We would recognise from a climatological point of view that this is one period of flooding associated with very high rainfall, which caused the sea surface temperatures around Australia to be exceptionally high,” he says. “This was one whole sequence of flooding over a period of a month but we know that for reinsurance recoveries, it is going to be broken into different periods.”

To make matters worse, there are squabbles over the definition of a flood, as reinsurers differ over what constitutes a flash flood and a river flood. “There is inconsistency in how floods are defined,” Muir-Wood says.

He points out that in the case of high-profile catastrophes such as the Australian floods or Hurricane Katrina, politicians can put pressure on insurers to pay out. This in turn can lead to ugly scenes with reinsurers.

Talk to the cedant

In the aftermath of the Australian flood, Munich Re warned insurers that they should adhere to the wordings of their insurance contracts.

Godwin points out that reinsurers are realising from past experiences that swift communication with the cedant company is vital in the aftermath of a catastrophe and are becoming much more hands-on in their approach.

“We have seen in the past few years a greater appetite from reinsurers to sit down with their buyers and understand first hand their strategy for dealing with the claims,” he says. “There is significant value after a catastrophe to mobilise your team and to go and visit the ceding companies on location through that process.”

Munich Re’s Roenneberg believes communication is vital: “It is important to talk to cedants to make them aware of the challenges – if they are not aware of the exposure, how can we be aware of the exposures?”

The past few months may have kept reinsurers busy, but the fall-out of this unusually active period will keep them occupied for many more to come.