Loopholes in the referral fee ban could undermine improvements being made in the sector

The motor insurance market has reported an improved 2013 according to EY, but the accounting firm is hesitant to say the tide has turned on a struggling marketplace.

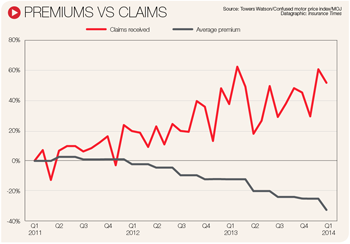

EY estimates that the motor insurance industry’s aggregate combined operating ratio (COR) will be around 101% for 2013, a 2.5 percentage point improvement on the previous year and the best result since 2006.

But EY says that these strong results have been heavily reliant on the delivery of the benefits of the Jackson and Legal aid, Sentencing and Punishment of Offenders (Laspo) reforms, and particularly the referral fee ban. But EY head of retail property and casualty actuarial Catherine Barton is wary about loopholes in the system.

“While referral fees themselves are banned, it looks like there are still ways in which customers can be encouraged to make claims, and that those encouraging them can receive payment in a form other than a referral fee,” Barton said. “Genuine claimants do of course need to be compensated, but the continued presence of manufactured claims in the market drives extra costs into the system, as well as increasing the number of claimants, which has a knock-on impact on premiums.”

Simon Gibson, managing partner at law firm SGI Legal, said that there are a number of ways of complying with the reforms and still receiving income in place of a referral fee.

“If both the insurer/broker and law firm take a robust and collaborative approach to compliance with Laspo, there are options which allow for insurers to maintain a revenue stream through the provision of legal services for their clients,” he said. “One of these could be creating a panel of law firms for their client to choose from, another is for law firms to act as a ‘first response’ on behalf of the insurer, or vice versa.”

And Barton said that the ability for firms to circumvent the referral fee ban means the reforms may not have been as effective as expected at reducing small claims volumes, despite insurers responding to the reforms with a cut in premiums over 2013.

“This is a real concern because of the drain it has on the industry and the knock-on impact on policy holders,” Barton said. “The motor insurance industry sees many late reported claims for small injuries that appear a long time after the accident, which raises questions about whether they’re genuine and should be compensated. The weight of these claims on the industry inevitably leads to higher premiums.”

But there is light on the horizon for motor insurers.

Independent medical panels for the assessment of whiplash injuries are expected to be introduced over the coming months, and Barton expects these to have a positive impact on the claims experience for insurers, as well as providing benefits for policyholders in the form of fairer and more accurate premiums.

“Having a medical panel could be a huge benefit,” Barton said. “Insurers often find it incredibly difficult to navigate the many injury claims they receive, particularly those involving soft-tissue damage, which are notoriously hard to determine, especially if claims come in late in the day.

“The panel should add clarity to the insurance process, which would ensure that the money customers are paying in premiums is more directly fed back to successful claims.”

No comments yet