Lemonade is the market’s most talked about disruptor. We look at Lemonade by the numbers

Lemonade is on everyone’s lips – and not just because it’s Pimms season.

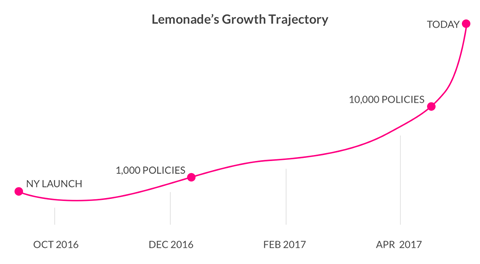

The start-up home insurer has enjoyed an unrelenting wave of positive publicity and steady growth since its launch in September 2016. It has been written about in Time, Wired and The Economist.

And it has attracted some big-name backers: Allianz added its name to the list of investors in April.

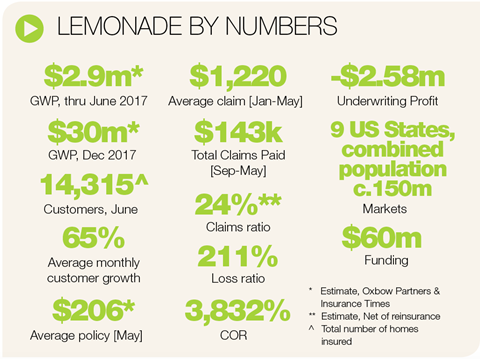

Looking at Lemonade by numbers the company has published on its site, the attention seems to be justified. As of June 1st, it had more than 14,000 in-force policies and an estimated gross written premium of $2.9m (£2.3m).

The 20% loss ratio it has quoted for 2016 is less than half the 52.5% average incurred loss ratio for the US homeowners insurance industry, according to 2015 figures from the Insurance Information Institute.

And in July it revealed that it made good on one of its key promises to policyholders: paying any premium left over after claims – and Lemonade’s 20% commission – to the non-profit organisations of customers’ choice.

In its first ‘giveback’ the company paid $53,174 to 14 non-profit firms, which it said was equivalent to 10.2% of revenue since launch.

But accounts filed with the regulator in its home state of New York paint a different picture of the company’s finances. In the first quarter of 2017 the fledgling insurer reported a net loss of $2.5m on the back of a $2.58m underwriting loss.

The loss ratio – net losses and loss adjustment expenses as a percentage of net earned premium – was 211% according to Insurance Times calculations, and the combined operating ratio (COR) an eye-watering 3,832%. This means the company is paying out $38 for every $1 it is bringing in, calling into question how it was able to pay any giveback at all.

So what is the real story? Is Lemonade, as some critics have suggested, more marketing than substance, or are these just the growing pains of a genuinely new and disruptive company?

Unanswered questions

There are certainly reasons to be sceptical that Lemonade can do as it says and challenge the traditional insurance model.

Are they truly in it for the customer? Do they really want to revolutionise the business model or is the exit strategy already in place?

If one of the company’s aims is to keep the cost of handling claims low, it still has some work to do. Its loss adjustment expenses (LAE) were around four and a half times net incurred claims for both the fourth quarter of 2016 and the first quarter of 2017.

Accounts show that the company is relying heavily on reinsurance, potentially making it susceptible to fluctuations in the price and availability. Reinsurers, which include Berkshire Hathaway and Lloyds, paid 91% of gross incurred claims in Q1 this year.

Although Lemonade’s business model is predicated on using artificial intelligence (AI) and behavioural economics, as well as giving back unused premiums, it will still ultimately be judged on the same metrics as its more traditional competitors.

Lemonade’s aim is for “Instant everything. Killer prices. Big heart”, but Nick Lamparelli, consultant and former catastrophe modeller at companies including QBE and Marsh, believes it’s hard to live up to all three at the same time.

“The real key performance indicators are retention, combined ratios and customer satisfaction. Those will take years to sort out,” says the founder and chief underwriting officer of US flood/catastrophe MGA, reThought Insurance.

“Are they truly in it for the customer? Do they really want to revolutionise the business model or is the exit strategy already in place?”

Lemonade’s reliance on AI could also prove to be a challenge. Other startups that have introduced automation and AI into the claims process, including Trov, have been dogged by questions over these systems’ ability to separate fraudulent claims from genuine ones.

There is no evidence to suggest fraud is of particular concern to Lemonade. It is, however, integral to their marketing: The price will be paid by its customers, who will see donations to their chosen charities diminished, as claims – fraudulent or otherwise – are processed.

While the company sells itself on its use of AI, it admits that its famous three-second paying artificial intelligence claims bot, AI Jim, handles only around a quarter of claims without human intervention.

Promising signs

But there are also signs that Lemonade could indeed be the disruptive force that it is being touted as. Customers so far seem to be broadly satisfied: Its smartphone app has an average rating of 4.2 out of 5. User experience afficionados swoon over the product design.

And while the results filed with the regulator look unflattering so far, it is only to be expected. Such a young insurance company could never hope to be earning enough premium to cover its claims and operating expenses. Even established firms suffer ‘new business strain’ when entering new lines of business. The costs are payable immediately, but it takes time to earn the premium, resulting in temporarily poor underwriting results.

UK insurtech fund EOS Venture Partners founding partner Sam Evans says he would not be concerned about profitability over the short term.

“The focus will be on growth: They have raised a lot of money which implies a healthy valuation,” he says.

“They are going to need to write a lot of business to justify that. They will be focusing on expanding the geographic footprint, adding new products and getting the brand out in the market.

“All of these will be costly, particularly marketing, hence I’m more interested in top line growth rather than profitability over the next two years.”

Comparisons are difficult, but one proxy could be German peer-to-peer insurer, Friendsurance. It was founded in 2010 and as of last year it had not posted a profit. Chief executive Sebastian Herfurth said pursuing profit would impact growth. The company raised $15.3m in 2016.

According to a top five global insurer, it usually takes around five years to start turning a profit from scratch.

The focus will be on growth: They have raised a lot of money which implies a healthy valuation.

In the meantime, Lemonade has a large cash pile. The company still has around $50m cash in the bank, and has raised $60m.

Patience

Plus its investors are not the impatient type. Backers include venture capital firms Sequoia Capital and GV (formerly Google Ventures) alongside Allianz and XL Innovate, part of XL Catlin, which took at a 10% stake in Lemonade as part of the start-up’s $34m Series B capital raising in December.

It also appears that overall company underwriting results do not affect Lemonade’s ability to make charity payouts. The company explains that policyholders choosing the same non-profit to donate to are placed into the same ‘virtual group’. The amount of giveback to that non-profit is determined by the level of claims, and thus unused premiums, in that particular virtual group rather than the company as a whole.

There are indicators that once it has overcome its growing pains, Lemonade could outperform its peers.

Founding partner at consultancy Oxbow Partners Greg Brown points out that Lemonade’s customer base, and thus its claims profile, is not typical.

The insurer rated 42% of its customers as ‘excellent’ risks in January. 81% are 45 or younger. 90% are renters, and based on the low average premium and claim amount ($1,220), it seems likely the coverage is short tail and low risk.

Lemonade’s renters insurance starts at $5, which it claims is up to 80% cheaper than its competitors. Detractors, including some customers, say that is because the cover is not as comprehensive.

A true disruptor?

Lemonade still has much to prove. But what cannot be disputed is Lemonade is usually the first insurtech to be invoked as a potential disruptor – even if people quibble over the definition of the term.

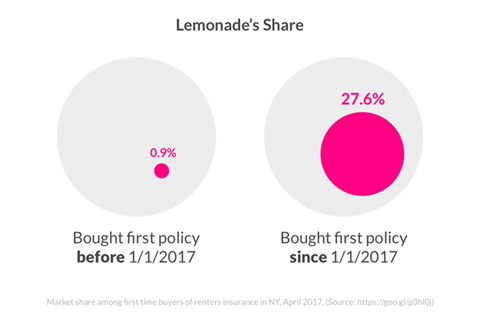

The company’s disruptive messaging, partly based on the assertion that insurers do not want to pay claims, may infuriate incumbents but it resonates with the millennial target market – as the company’s indicative capture of 28% market share of first time buyers of renters insurance in New York suggests.

While the vast majority of start-ups fail, the vast majority of those that reach a Series B funding round, which is typically dedicated to financing a company’s building phase after its initial development, succeed.

The answer could be in Lemonade’s own tagline. “A tech company that does insurance.”

Viral marketing and ‘growth hacking’ is standard parlance in tech circles. If the company can eliminate even marginal operating costs while driving low cost per acquisition (CPA), loyalty and referral, it could win big. Chief executive Daniel Schreiber recently said Lemonade has reduced the CPA by a factor of 10. The market average for home insurance is understood to be around $65.

Most consumers like the idea of Lemonade, while innovation evangelists love it for its use of technology and customer-centricity, through which it promises to offer improved customer experience as well as insurance. Lemonade has become their standard bearer.

The marketing will continue. And the market will be watching.

No comments yet