Insurers and brokers are grappling with the immensity of the challenge and opportunity the digital revolution presents

“The computer is here to stay, therefore it must be kept in its proper place as a tool and a slave, or we will become sorcerer’s apprentices, with data data everywhere and not a thought to think.”

So said Jesse Hauk Shera, a celebrated American information scientist and pioneer of the use of IT in libraries, who died in 1982.

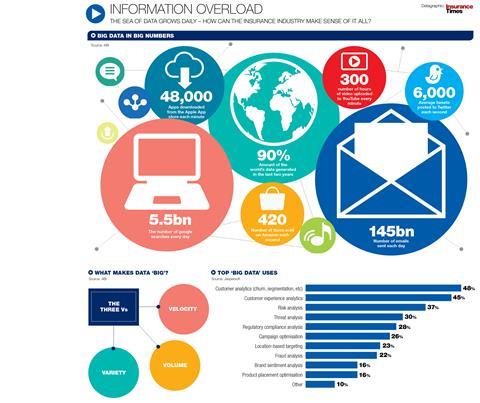

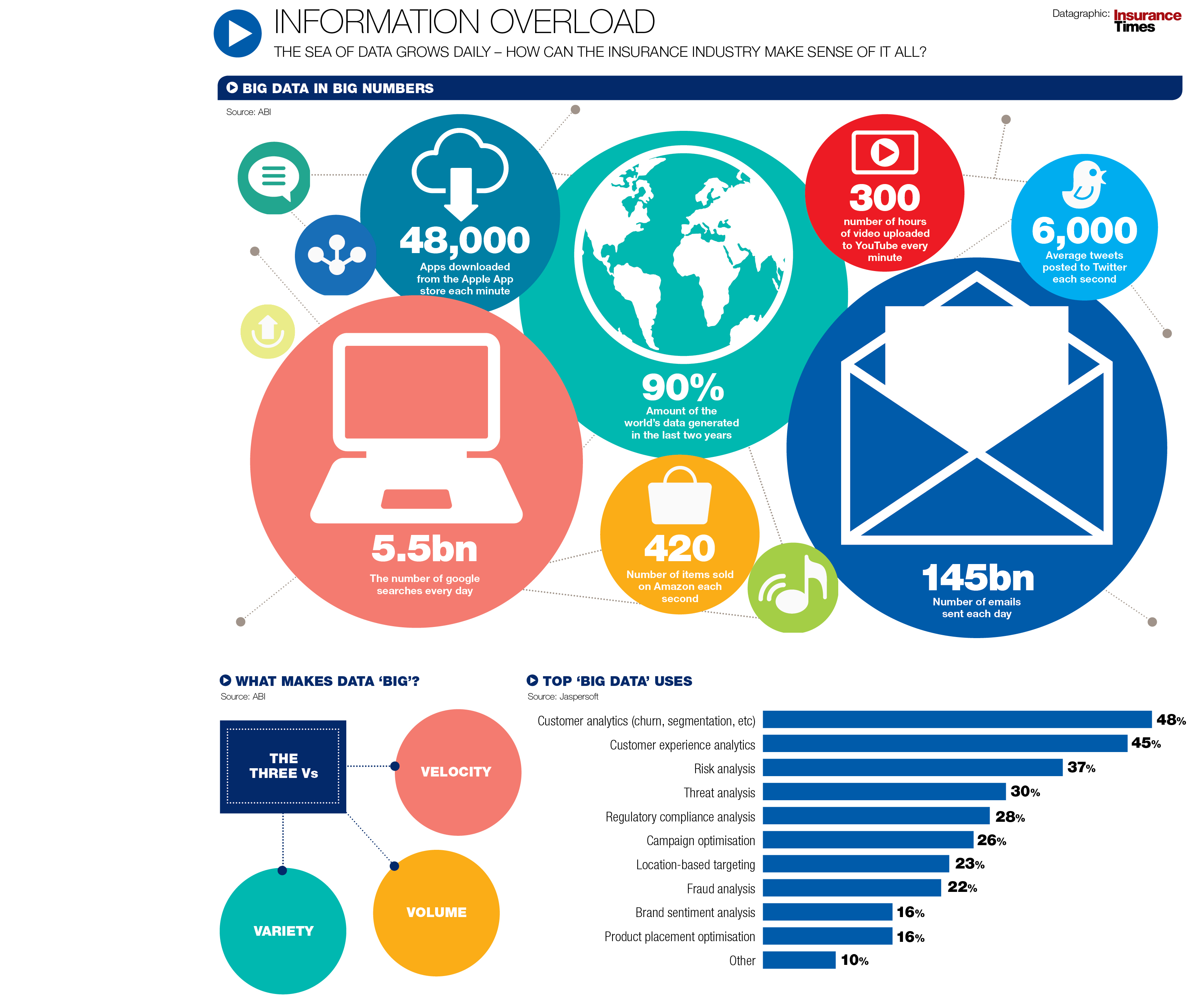

Fast forward to today, and it is estimated that 90% of the world’s data has been created in the last two years alone. In fact, we now create as much data in a single day as we have done from the dawn of civilisation up until 2003, according to Google chief executive Eric Schmidt.

With masses of information at their fingertips, the way insurers and brokers assess, price and underwrite risk is set to change, both in personal and commercial lines.

Personalised products

More data – from both internal and external sources, structured and unstructured – means more rating factors and more opportunities to offer more tailored products.

In the UK personal lines market, there are already signs of this, with insurers and brokers using information such as credit scoring and driving records (via the MyLicence database) to provide more accurate price quotes.

Also, the ability to generate more value from claims information, including spotting indicators of fraud, is becoming more effective thanks to advanced analytics.

And external sources of data can help insurers identify new and emerging risk areas that are likely to be sources of significant claims in the future.

Click here for a larger version

The amount of data available to the industry is set to rise exponentially. The key challenge is, therefore, how to make sense of the information.

“We have only begun to scratch the surface of available data,” says Aon Benfield’s latest Insurance Risk Study.

“We can look for new predictive variables in the ‘digital exhaust’ we all leave behind in our day-to-day lives. We can also capture more directly relevant data through risk-monitoring quid pro quos, such as home telematics and the Internet of Things.”

In UK motor more than one-third of fleets employ a telematics system and the usage-based insurance market grew by 15% between 2013 and 2015, according to Ptolemus Consulting Group. According to one survey by RAC Business, 35% of businesses in the UK have used telematics data to contest either a speeding fine or a false insurance claim.

Another piece of research by Chevin Fleet Solutions, however, found that the possibilities presented by emerging Big Data are overwhelming for fleets. Many are collecting too much data that has no strategic purpose.

Chevin managing director Ashley Sowerby says: “Future developments such as greater use of telematics, mobile data and the connected car all mean that Big Data is only going to get bigger and we will see more exponential increases.

“Making this mass of information easily digestible and just good, old-fashioned useful, will require more and more ingenuity.”

Winners and losers

For Aon Benfield’s global chief executive of analytics Stephen Mildenhall, the challenge rests firmly in analytics and value is extracted from the information being gathered.

“Telematics is a fantastic example of harnessing technology in a useful way for insurance and we’re only just beginning to get to grips with what it has to offer,” he says.

“But telematics devices in cars can provide up to 750Mb of information a minute. It’s capturing this huge amount of information that is clearly relevant: how you drive, where you drive; and it’s not a great leap to think this information is going to be correlated to accident propensity.

“But it’s a pure analytics problem of teasing out the signal from all of that noise – what are the relevant statistics to look at?”

{kind=link}

No comments yet