The Cardiff-based insurer’s share price plunged by 15% last month as a result of profit concerns

The insurance darling of the stock market is having a blip.

Admiral’s share price is down by nearly 15% since the beginning of March 2022, at the time of writing.

This drop was caused by concerns over Admiral’s dividend, its ability to deal with claims inflation challenges and questions over reserving.

Despite the insurer reporting a 27% rise in its UK motor insurance profits for 2021 to £871.1m, according to its full-year financial results published on 3 March 2022, Admiral’s chief executive of UK insurance, Cristina Nestares, said that this year, the insurer is ”expecting profits to come under some pressure”.

Investors and analysts are now examining how serious the claims inflation challenge is for Admiral’s profitability.

Reserving and claims

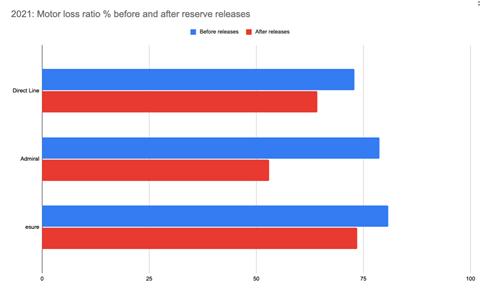

Compared to its rivals, Admiral’s headline figures on claims are superior. In its latest results last month, Admiral reported a UK motor loss ratio of 53% - better than both Direct Line Group (DLG) and Esure.

However, before reserve releases, Admiral had a 78.8% loss ratio for 2021, which is 6.5% worse than 2020.

Admiral actually trails behind DLG in terms of its loss ratio before releases (see table).

Speaking to analysts about these results, the insurer’s chief financial officer Geraint Jones explained that Admiral had a number of underwriting years that ”have become very profitable”, which has enabled the reserve releases.

For example, in 2018 Admiral recorded a loss ratio of 92%. This came down to 81% at the end of 2019 and 73% in 2020.

Despite Jones’ assurances, some industry voices believe there remains a bear case.

Investment bank Jefferies, for example, believes Admiral’s ”recent acceleration of reserve releases and heightened inflation will likely reduce the level of future reserve available to release”.

Furthermore, in a briefing note written at the end of last year, Jefferies questioned Admiral’s capital structure and whether it could withstand the headwinds coming from claims inflation.

The Cardiff-based insurer uses quota share reinsurance - so, for every pound written, Admiral only retains 22p in risk.

It takes a profit commission from its reinsurance partners on the rest of its book.

Jefferies predicted that Admiral will face lower underwriting profitability as it grapples with higher claims inflation. In turn, this will lead to less profit from its reinsurance arrangements.

Admiral also has a relatively low level of excess of loss cover compared to its peers, which could leave it exposed if there is deterioration in long-tail bodily injury claims.

Admiral’s bull case

The future of Admiral’s profits going forward has polarised opinion, with some commentators rallying behind the company’s prospects.

Analyst firm Berenberg believes Admiral has an advantage in terms of bodily injury claims.

Equity analysts Thomas Bateman and Kathryn Fear wrote in a post-results briefing note last month: “Claims inflation is running at mid to high single digits, versus mid single digits in 2021.

“This is being driven by labour shortages resulting from Brexit, an ageing workforce, increasing energy costs and rising used car prices.

“These are all negatives but, in our view, nothing that was not well known by the market.

“We would also highlight that Admiral is more exposed to bodily injury claims than [its] peers that reinsure the bodily injury risk.

“We note that claims inflation is lower in bodily injury [claims] versus damage claims. In addition, pricing is continuing to rise at high single digits - hence there is no reason why it cannot match claims inflation.

”In fact, pricing is more likely to overshoot claims inflation, leading to a period of outperformance for motor insurers.”

Independent analyst Librarian Capital agreed with Berenberg, believing that industry fears around profit declines were overblown.

It stressed that Admiral has an advantage because of having a lower cost base, as well as the fact that it is growing faster than its nearest rivals - such as DLG - and has a historic track record of strong underwriting profitability.

“Investors’ fear of future profit declines were likely why [Admiral’s share price] fell 14% on the day of results,” Librarian Capital said.

“We believe this was too short term. The profit decline is likely to be limited in size and cyclical, while Admiral’s customer base continues to grow - profits will be much larger when the cycle turns.”

Read: FCA pricing reform will encourage ‘evolution rather than a revolution’ – Admiral Group

Read: Admiral named best Gibraltar-based insurer for second year running – Insurance DataLab

Market claims challenge

Whatever happens to Admiral, one thing is for sure - the whole market is struggling with the claims inflation challenge.

Matt Scott, co-founder of Insurance DataLab, explained that a cocktail of factors is causing claims inflation, such as supply chain issues, increasing import costs due to Brexit and staff shortages hitting the motor repair sector.

Insurers with scale - and especially players that own their repair network, such as DLG - will have an advantage.

“Those with a repair network can have a [better] handle on costs they are handling internally, or negotiate better rates because of the scale they are putting through the network,” he said.

Scott believes claims inflation is here to stay as technology advances.

He continued: “We have advanced driver assistance systems (Adas) and the costs of that. Electric vehicles are coming in as well, which are mostly difficult to repair.

“Then we have autonomous vehicles, which will reduce [claims] frequency but will be more costly and difficult to repair.

“Across other markets, even in the property market, the cost of wood and labour has shot up.

“There is a lack of labour supply in certain trades, such as electricians and plumbers, so that will cost a lot more in certain lines with property repair.

“It is certainly going to be [a] challenging 2022 for personal lines insurers.”

No comments yet