Reserve releases surge but Engelhardt says long-term success lies beyond UK motor

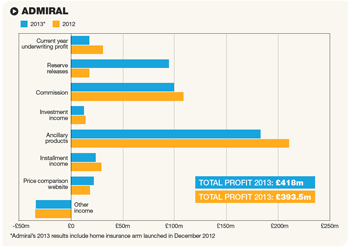

Admiral’s UK motor business made a profit of £393.m in 2013, up 6% on the £372m it made in 2012.

The insurer’s combined operating ratio (COR) improved by 8.2 percentage points to 81% (2012: 89.1%), largely driven by a five-fold surge in reserve releases to £94.2m (2012: £17.6m).

However, the UK motor turnover dropped by 12.2% to £1.7bn (2012: £1.94bn) because of a focus on lower premium, lower risk business.

In his trademark quirky style, Admiral chief executive described 2013 as “the year of the baked potato” because it was “solid, but not flashy”. He said: “This is a comfort food set of results.”

While noting that Admiral’s short-term success would continue to be driven by reserve releases from UK motor, Engelhardt added that the recipe for the insurer’s long-term success would come from beyond the UK motor market.

He said: “You don’t look at a baked potato and think nutrients. Just as you might not look at Admiral’s 2013 results and see the progress made by our non-UK operations and UK Household. But for both Admiral and the potato, they are there.

“It’s not just the businesses we’ve set up in Spain, Italy, France, the US and UK Household that give me confidence, it’s the people we’ve got running them. They, along with a number of others, are the future.

He added: “Our strategy, once again like a baked potato, is simple: to make measured progress in the UK car insurance market while taking what we know and do well, which is internet and telephone delivery of insurance, to create growing, profitable, sustainable businesses outside the UK and in UK household insurance.”

Home and international losses

Admiral’s fledgling UK household business, launched at the beginning of 2013, made a £100,000 underwriting loss in its first year of operation.

Admiral retains 30% of the UK household premium it writes, passing the other 70% to reinsurers Munich Re, which takes 40% and Swiss Re, which has a 30% share.

Admiral said it has also purchased excess of loss reinsurance on the home account to mitigate the effect of catastrophe claims.

Admiral’s international car insurance made a loss of £22.1m (2012: loss of £24.5m) and reported a COR of 152% (2012: 177%).

Group profit, which is still mainly driven by UK motor, rose 7% to £370.2m (2012: £344.6m).

Rebutting criticism

Admiral’s leaders also took the opportunity to rebut criticisms of the company’s financial performance.

Analysts and other commentators have previously attacked the company for depending too heavily on ancillary income and reserve releases.

Commenting on ancillary income, Engelhardt said: “Some people might say that our results are dependent on ‘other revenue’ and that this income is under regulatory threat.

“It’s true, we do make good money from ‘other revenue’, but so does the rest of the UK market. If you took away all ‘other revenue’ tomorrow it might surprise you to know that I’d be the happiest guy in town. Why? Because it means that all any firm has left is its combined ratio, forcing a battle for survival of the fittest and we are, arguably, the fittest.”

Commenting on criticisms about reserve releases propping up results, Admiral chief operating officer David Stevens said: “To my mind, underwriting profits derived from releases on older, more developed, more predictable years cannot be lower quality than underwriting profits reported on current, undeveloped, years.

“Secondly, in Admiral’s case, profits from reserve releases can’t be considered ‘one-off’ – we have released reserves every year since our flotation in 2004, at an average of 12% of premium earned.”

No comments yet