RSA has been through a turbulent decade, but analysts now predict good times ahead. True or is it another false dawn?

Briefing by Saxon East

Looking for a good share buy? Well RSA is the place to go, according to analysts.

’The cheapest name in UK retail space,’ says the well-respected analysts at Barclays.

This week Jeffries calls it ‘one of the most fundamentally mispriced stocks in the sector.’

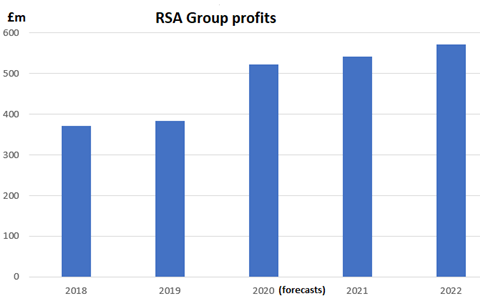

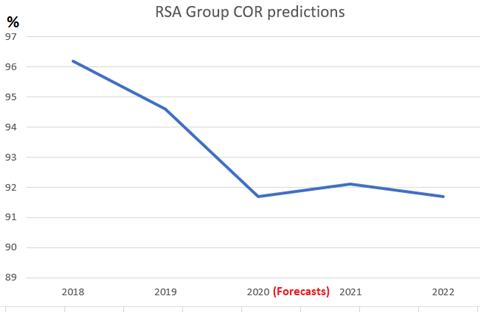

They forecast impressive improvements in combined ratio and profits stretching into 2022 (see below).

It’s been a long journey, but a number of analysts are convinced chief executive Stephen Hester will deliver.

Once investors realise the losses from Covid are manageable, they will pile in. Jeffries predicts a 50% share price rise from its current standing at 412p.

Market watchers believe Hester has cleaned up the underperforming parts such as marine, cut back on a troublesome UK business so it can deliver stronger combined ratios and successfully focused on the more profitable parts of the group in Scandinavia.

All good then? Not quite.

RSA surprises and broker service

For UK brokers, what matters is customer service. In our service surveys, they rated RSA as one of the bottom performers this year in both commercial and personal.

RSA’s UK and International chief executive Scott Egan is showing improvements on combined ratio, but he will be keen to improve broker service.

Ex-Paymentshield chief executive Kay Martin has been recruited to lead improvements on personal lines, part of an overhaul of the UK management team last year.

In UK commercial lines, the global and domestic risks units joined together: a more simple structure.

Investor troubles

On the investor front, some shareholders will be wary of RSA. The last decade was turbulent.

The Irish accounting scandal in 2013 came out of nowhere. Fund managers were very concerned and retail investors attracted by RSA’s solid reputation were left disappointed.

Best yet to come: RSA CEO Stephen Hester has primed the insurer for good times, analysts and market watchers say

People’s retirements funds were hit because of reckless behaviour and poor managerial oversight at RSA.

Last month, it emerged 65 shareholders were suing RSA over the scandal.

Following this crisis, Hester steadied the ship with a rights issue, solvency boost and a cull of worst performing parts.

Rival insurers say RSA’s geographic footprint in the UK across property leaves it more exposed than rivals on catastrophe and weather-related claims.

There is inherent volatility in the business.

So some were surprised when the problems came from elsewhere in 2018, with the London market and marine leading to a ‘disappointing’ third quarter £70m underwriting loss.

Hester and RSA supporters would argue with some justification that 2018 had some bumps, but this can be expected in a large insurer on a journey to correcting its portfolio and optimising its capital allocation.

Indeed, RSA recovered quickly.

It had a good 2019, with record year in underwriting profits.

Even with Covid, it appears 2020 will also be solid.

Post-2020, RSA will really begin to shine, analysts say.

Let’s hope the surprises are over once and for all.

No comments yet