Insurance DataLab unpicks underwriting in the motor insurance market, flagging the financials of successful firms that have weathered pandemic and regulatory-induced trends

UK motor insurers returned to underwriting profit for 2020/21 with a combined operating ratio (COR) of 93%, according to the latest analysis from market intelligence and research service Insurance DataLab.

This is an 11 percentage point improvement on the 104% COR the motor market reported for 2019/20 and is also five percentage points better than the 98% COR recorded for 2018/19.

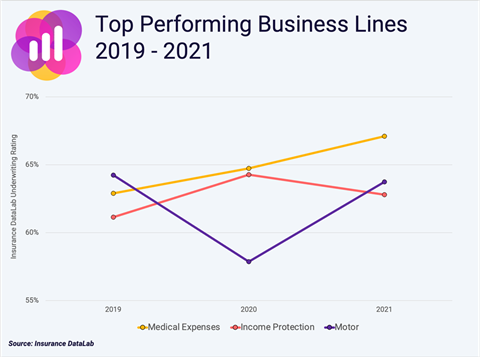

This marked improvement led to UK motor insurers picking up an average Insurance DataLab underwriting rating of 64% for 2021 – the second highest rated business line, behind first placed medical expenses insurance (67%), in Insurance DataLab’s inaugural UK Underwriting Performance Report, which was published in February 2022.

This 64% result represents a six percentage point improvement on the 58% underwriting rating motor insurers received for 2020, making it the most improved business line over the last 12 months.

Pandemic driving improvements

Motor insurers have, of course, benefited from a reduction in claims as a result of the Covid-19 pandemic, with driving miles falling across the UK.

Figures from car insurance provider By Miles found that, as of November 2020, UK drivers had reduced their weekly mileage by as much as 550 million miles because of homeworking during the pandemic.

Indeed, a December 2020 study of 2,000 British drivers by insurer Direct Line found that 55% of respondents were driving fewer miles than they did before the first Covid-19 lockdown.

This trend contributed to net claims incurred falling by 15% to £5bn for 2020/21, down from £5.9bn for the previous year.

This, combined with a 2% increase in net earned premiums, meant that the UK motor market reported an aggregate loss ratio of 60% for 2020/21 – a 12 percentage point improvement on the 72% loss ratio reported for the previous year.

This was, however, partially offset by a less than 1% increase in operating expenses for this line of business, to just over £2.7bn.

But, the pandemic-induced changes that hit the motor claims market are expected to be relatively short-lived, with many workers already returning to their offices and driving miles beginning to creep up again.

This does not mean that the UK motor insurance market will simply return to clocking up pre-pandemic commuting miles, however.

Annual mileage levels are expected to remain lower than immediately before the Covid-19 pandemic, meaning that reduced mileage policies are predicted to become more popular - this will apply downward pressure on premium levels.

Figures from Consumer Intelligence’s Car Insurance Price Index, which was last published in December 2021, revealed that motor insurance premiums fell by almost 8% in the 12 months to the end of November 2020. This meant that average premiums had reached their lowest levels since early 2017.

Regulation challenges

But regulation is also set to have an impact on UK motor pricing.

The FCA’s general insurance pricing reform, effective from 1 January 2022, has now banned price walking, meaning that insurers need to offer the same rates to existing customers as they do to new business. This will undoubtedly lead to lower renewal prices for motor insurance customers.

However, this will also create a challenging environment for insurers with a large back book that have previously practiced price walking.

Ongoing data from Consumer Intelligence further suggests that many motor insurance customers will, somewhat counterintuitively, be more likely to shop around when faced with a substantially lower renewal premium, compared to pre-reform times last year.

On the flip side, new business rates are expected to increase, but with competition for new business expected to remain intense, there could be a number of players – particularly at the smaller end of the market – looking to the regulatory changes as a way of winning market share from some of their more experienced competitors.

These fluctuations will, of course, add pressure to CORs in a product line that has traditionally found underwriting profit hard to come by and it would not be surprising to see motor insurance slip back down Insurance DataLab’s underwriting rankings next year.

About Insurance DataLab

InsuranceDataLab.com is a market intelligence and research service, focusing on the performance of insurers, Lloyd’s syndicates, MGAs and brokers based in the UK and Gibraltar.

With hundreds of thousands of data points covering almost £100bn of annual gross written premium and featuring more than 1,000 insurance companies and brands, InsuranceDataLab.com provides access to comparable industry data to help providers benchmark performance, assess existing and potential partners and identify new opportunities.

QBE rises to the top

In addition to analysing the performance of individual business lines at an aggregate level, Insurance DataLab has also ranked the 25 largest UK-regulated insurers on their underwriting performance.

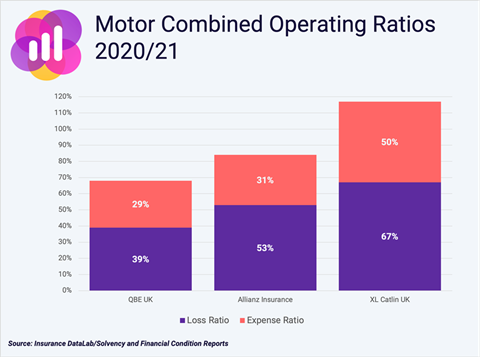

Top of the pile for motor insurance in 2021 was QBE UK, which outperformed the market aggregate position by almost 25 percentage points to report a COR of 68% – the best motor COR in this analysis – helping QBE to pick up a motor underwriting rating of 79% for 2021.

The 44 percentage point improvement in QBE’s motor COR was also the best uptick recorded in this analysis, with the insurer picking up a 95% rating under Insurance DataLab’s COR improvement metric.

This movement was driven by a drop in claims that knocked 48 percentage points off the insurer’s loss ratio after net claims incurred fell by 60% for the year ending December 2020 to reach £96.2m, compared to £240.1m a year earlier.

This led to the insurer reporting a 39% loss ratio for 2020, down from 87% for 2019.

Meanwhile, QBE’s expense ratio remained relatively steady at 29% for 2020, compared to 25% in 2019, after the insurer’s operating expenses increased by 4% to £70.5m.

A three-year motor COR of 93% – which equates to a standardised underwriting score of 68% for this Insurance DataLab metric – means that QBE has an overall motor underwriting rating of 80% for 2021.

This is eight percentage points higher than any other insurer in this analysis, as well as 16 percentage points ahead of the 2021 market average.

Allianz and XL Catlin UK make improvements

Allianz Insurance and XL Catlin Insurance Company UK were ranked second and third respectively by Insurance DataLab, with motor underwriting ratings of 72% for 2021.

This marks an eight percentage point improvement for Allianz Insurance after it earned an Insurance DataLab underwriting rating of 64% for 2020. Last year’s score is also better than the 66% rating it received for 2019.

Allianz’s improvement over the last 12 months was driven by a 13 percentage point improvement in its motor COR to 84%, down from 97% a year earlier.

This earnt the insurer a COR rating of 72% for 2021 (2020: 67%) and a COR improvement rating of 76% (2020: 55%).

Allianz also picked up a three-year COR rating of 69% after reporting an aggregate COR of 92% for the three years to the end of December 2020.

This compares to 2020’s three-year aggregate COR of 97%.

XL Catlin Insurance Company UK’s 2021 underwriting rating represented a 28 percentage point improvement on the 44% rating it received for 2020 after its COR improved by an impressive 46 percentage points – this result earned it a 95% COR improvement rating, the highest in this analysis.

This was, however, not enough to take the insurer back to underwriting profitability. It reported a 117% motor COR for the year ending December 2020, down from 163% a year earlier, with the insurer picking up a 59% Insurance DataLab COR rating.

The improvement in the insurer’s underwriting performance was driven by a large increase in premiums following a transfer of business from other group companies - XL Catlin Insurance Company UK’s motor net earned premium rose more than sevenfold in 2021 to £10.6m, compared to £1.4m a year earlier.

And while net claims incurred more than tripled over the last year to £7.1m, the overall effect of these changes knocked 75 percentage points off the insurer’s loss ratio, which fell to 67% for the year ending December 2020, down from 142% a year earlier.

This was, however, partially offset by a 29 percentage point increase in the insurer’s expense ratio – this reached 50% after its operating expenses rose to £5.3m for 2020 (2019: £301,000).

Methodology

Performance metrics have been calculated using Insurance DataLab’s own analysis of insurer Solvency Financial Condition Reports (SFCRs), which take into account both short and long-term performance over the last three years of underwriting.

The three metrics used to calculate the overall Insurance DataLab Underwriting Rating are:

- Combined operating ratio (COR): Insurance DataLab has calculated the COR as the amount paid out in claims and expenses as a proportion of net earned premiums, with a sub-100% COR representing profitable underwriting.

- COR improvement: To account for improvements in underwriting performance over the last 12 months, Insurance DataLab has also calculated the improvement in COR compared to the previous year.

- Three-year aggregate COR: Insurance DataLab’s assessment of long-term performance has been made using the three-year aggregate COR, which is calculated as the aggregate amount paid out in claims and expenses over the last three years as a proportion of net earned premiums over that period.

Each metric has then been standardised to create a percentage score for each insurer, with a weighted average used to create the overall rating.

Full details of how these metrics have been calculated, as well as summary data for all 25 insurers rated in this analysis, can be found in the inaugural Insurance DataLab Underwriting Performance Report.

No comments yet