As Gefion handles its solvency ratio getting reduced to 86%, Insurance Times analyses its UK market exposure

Danish insurer Gefion’s rapid growth in the UK motor market looks to be heading to an abrupt halt after a regulatory inspection bit down hard on its solvency ratio.

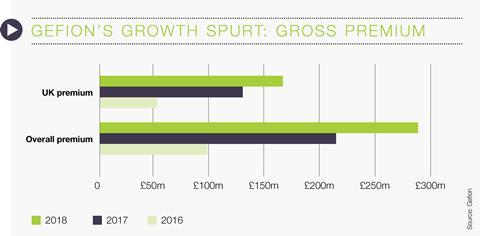

Gefion’s Solvency and Financial Condition report showed the business saw a growth boom of 29% in the UK last year. It reported UK gross premiums of around £168m for 2018, up from £130m in 2017. Overall gross premium grew from £215m to £292m - growth of 36%.

However, until it raises capital to improve its solvency ratio, which following the Danish regulator’s latest intervention is at 86%, the insurer has been ordered to cease the expansion of its business.

Coming after announcing an underwriting loss for 2018 and the news that Premium Credit will no longer finance Gefion-written policies, unless it can reach a solvency ratio of 135% by mid August, pressure is building for the unrated carrier.

Joanna Parsons, analyst with Canaccord Genuity, said that whatever happens with Gefion, it will most likely need to shrink its book.

“Whilst not a given, were Gefion to go under completely then there may well be additional van policies up for grabs,” she said.

“Regardless, Gefion still has to improve its solvency position (and manage down its volumes), implying it will have to increase pricing significantly to do so.”

This she said, could help the likes of Sabre and Hastings grow their van books, as they become more competitive.

Broker concern

With a solvency ratio below 100%, brokers too may think twice before renewing customers on Gefion policies, due to the potential risk of collapse.

Brokerbility chairman Ashwin Mistry last week reiterated his view that brokers should wean themselves off using unrated insurers, or else pay an increased proportion of the FSCS levy. It’s a view that has been given before, as the debate around the use of unrated insurers rumbles on. Four alone - Alpha, Horizon, Qudos and LAMP, have collapsed in the last 14 months. Enterprise and Gable both collapsed in 2016.

The FSCS helped transfer over 370,000 customers in the last year due to insurer collapses. Enterprise UK motor claims are expected to reach over £157m, with the FSCS having already paid over £118m in compensation to customers. For Liechtenstein-based Gable, the FSCS has to date paid around £43m in compensation.

But the good news for Gefion is it still appears to have support.

Brokers have shown signs they are willing to take their business away from Premium Credit and seek financing options elsewhere, rather than renew with a different carrier.

And after meeting with Gefion, wholesale broker Bollington Underwriting suggested to its brokers that the unrated insurer would be able to boost its solvency ratio to a safer level in the short-term.

Gefion has stated it is taking “immediate steps to recapitalise the business” to take the solvency ratio back above 100% and start expanding again.

The focus now, it said, is on “consolidation and profitability in existing programs”.

More importantly longer-term, Gefion has revealed it is in discussions with a number of third-party investors to “significantly increase” its capital base before the end of the year.

With exposure stretching to £168m in the UK, the FSCS would welcome such a deal to ease Gefion’s solvency worries sooner rather than later.

| 2018 | 2017 | 2016 | |

|---|---|---|---|

|

UK premium |

£167m |

£130m |

£52m |

|

Overall premium |

£291m |

£216m |

£98m |

No comments yet