Insurers and brokers should expect a big surge in claims ahead of the latest round of whiplash reforms and, once the new portal comes into place, prognosis shift and an attempt by CMCs to reposition themselves

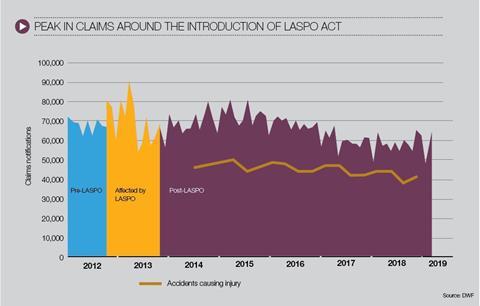

First it was the Woolf reforms of 1999, which precipitated the Civil Procedure Rules, then the Jackson reforms, enshrined as the Laspo (Legal Aid, Sentencing and Punishment of Offenders) Act of 2012. Each stage of claims reform has attempted to tackle the UK’s “whiplash culture”, with varying degrees of success.

Now insurers and brokers are awaiting the finer details of when the Civil Liability Act and new “litigants-in-person” claims portal will come into force. At this stage it is uncertain whether the legislation will succeed in bringing down the cost of personal injury claims to the benefit of all policy holders, or if the reforms will simply prove to be another set of rules for unscrupulous claims farmers to circumnavigate as they seek new ways of extracting money from the system.

“Every reform we’ve had was meant to be a whole new dawn,” says Mark Hemsted, a partner who leads Clyde & Co’s volume motor practice. “And with every reform you saw a large number of claims going through shortly before the closing date, then claims dropped off significantly in the period shortly after reform and then they slowly came back.

The Civil Liability Act is attempting to tackle the high volume of personal injury claims – particularly road traffic accident (RTA) whiplash claims – on a number of fronts. It will impose a tariff of fixed damages that are significantly reduced from current levels for soft-tissue injuries lasting up to two years. Additionally, it will increase the small claims limit for RTA claims to £5,000, with the intention that most claimants will be guided onto an online portal, reducing the involvement of personal injury lawyers.

Calum McPhail, head of liability claims at Zurich, thinks it is inevitable that there will be a surge in claims.

“The reforms in the small claims track and whiplash will affect two principal areas, namely the level of damages awarded and the fact that legal costs will no longer be recoverable in certain cases,” he says.

“On that basis, it is easy to imagine that there may be a surge in claims submitted prior to changes in an effort to maximise both the level of awards and recoverability of legal costs.”

The suggested reforms have been widely welcomed by the insurance industry, with the ABI estimating the total value of fraudulent motor claims at £775m in 2018, a rise of 4% year on year. It is hoped the reforms will make personal injury claims less lucrative, dissuading organised criminal gangs and opportunists alike from exploiting the system.

Prognosis shift

There are still many question marks, including the timescales involved. Experts are quick to point out that the government does not have a great track record when it comes to implementing new claims portals on time and the proposed deadline of April 2020 is expected to slide. Others are dubious about the long-term benefits of the reforms, anticipating that claims management companies will simply find new ways of making money once the system has bedded in.

Prognosis shift is one likely element, with an increase in claims for other soft tissue injuries, including knee and elbow complaints which are not subject to the fixed damage tariff once the regime comes in.

“It is disappointing that the whiplash definition did not include for associated minor injuries, in terms of valuation, but also in relation to legal costs recovery,” says McPhail. “So we expect to see elements of exaggeration in relation to those areas as a means to circumvent the true intention of the reforms.”

There is also anticipation that claims management companies (CMCs) could push claimants to gain a medical diagnosis of whiplash that extends beyond 24 months. This would take them out of the small claims track, significantly increasing the potential awards.

“In the current system, an expert might say, ‘we anticipate this whiplash victim will make a full recovery after nine months’,” says Hemsted. “And the claimant will accept that, take the money and disappear. Whereas, under the new reforms, we’d expect them to elongate the prognosis period to get as many claims beyond 24 months for pure whiplash as is possible by sending them back for additional medical reports.”

Small claims

Meanwhile, CMCs could move into the small claims track, as personal injury lawyers move away, and there could be an increase in exaggerated and opportunistic claims as a result. Mathew Kiff, corporate team leader at BHIB Insurance Brokers, points out that it may be more difficult to detect fraud in the digital portal and that insurers need to consider how they will tackle this.

“CMCs are likely to move into the space left by lawyers at the lower end. Capturing the third party quickly will become more imperative to keeping claims costs and therefore future premiums down as much as possible for the customers that we look after,” he says. “Brokers can still position themselves to be a part of this process and play their part in managing the claims once reported.

“You’ll find that the majority of negative comments regarding the bill are from the people who stand to lose profit from it. While they make some valid points that need to be considered, on claimants not having access to free ‘no win/no fee’ type legal advice or access to the internet, it’s those companies that needed to be targeted for the overall good of consumers.

“The FCA are taking over regulation of CMCs with effect from April 2019 and they’ve set out rules and guidance which must be followed,” Kiff adds. “This can only be a good thing to drive up standards in that sector, which has been let down by a few. The professionalism of our sector is paramount to winning back the customer trust and the increased fines that can be enforced for companies not adhering to the higher standards is an important step.”

Pledge to pass on savings

In 2018, the chief executives of 26 major insurers signed a pledge to pass on savings from the Civil Liability Act to their customers. It is hoped the reforms will reduce the cost of personal injury claims, benefitting each policyholder by as much as £35 per year.

The cost of motor insurance fell in 2018 for the first time in four years, according to the ABI’s Motor Premium Tracker, suggesting the industry is already making good on that pledge.

“Implementing the provisions of the Civil Liability Act will be crucial to delivering a fairer compensation system for claimants and continued competitive premiums for motorists,” said ABI assistant director and head of general insurance policy Mark Shepherd.

No comments yet