The British construction industry is suffering, which means some insurers and brokers will be hit too. Jeremy Buckley explains

Gordon Brown is considering allowing councils to build more homes. But such pieces of good news for the construction industry have been rare in recent months. And insurers, brokers and loss adjusters need to keep in mind how tough times are for the sector.

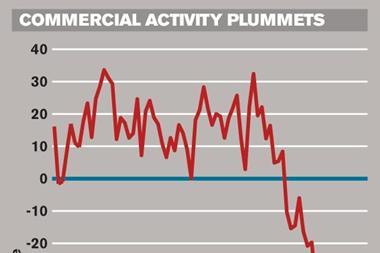

Housebuilders have watched in disbelief at the implosion of an industry that was healthy and sustainable less than a year ago. Their share prices have plummeted, as has the market for private finance initiatives – government-funded public-private partnerships. Many landmark developments have been pushed back as funding has all but dried up.

Construction and related industries make up about 200,000 companies that employ more than 2 million people, generating about £200bn in revenues. They are, in effect, the heart and soul of our economy.

In its pre-Budget report in November, the government announced plans to help the industry by bringing forward £3bn of infrastructure work. The chancellor Alistair Darling also said he would bring forward by one year the £800m earmarked for the Building Schools for the Future programme, which funds the modernisation of schools. Social housing was given a further £775m – originally earmarked for 2010 – to be made available over the next 16 months for upgrades, repairs and some new-build projects.

This all sounded positive, until it was reported that Building Schools for the Future was in jeopardy. The initiative is worth more to construction than the 2012 Olympics and the Heathrow expansion plan combined, so any delays will have serious consequences.

Meanwhile, the withdrawal of exemption from National Insurance contributions in holiday pay – set up to encourage construction workers to take time off – will cost the industry a further £150m a year.

At a time when it needs all the help it can get, construction is facing a number of serious problems – rising material and energy costs, an expensive contract bidding process, an imperative to redress environmental issues and a shortage of skilled labour and professional management.

Strong order books will ensure many construction companies have a consistent workflow – for now. But confidence has been eroded and the predictions are that there will be an upsurge in failures of small construction-related firms.

One of the big challenges is the retention of the industry’s skills base – something that could take many years to recover if it is allowed to diminish. Construction also has a lot of talent within many small companies, something that supports the UK as a global leader in building technology.

These businesses are the most vulnerable as banks continue to run for cover, while many of the larger companies will be able to ride out the recession. They will also be in a strong position when things pick up.

However, 312 construction companies were rated as “in danger” in an analysis of the 2,000 largest building companies in the UK, published earlier this month. In the report by researcher Plimsoll, 121 companies reported falling sales for the second year in a row and one in nine admitting to selling their products and services at a loss. My guess is many of these businesses will be forced into retirement, retraining or receivership.

Impact on insurers and brokers

All this will have a knock-on effect on insurance. Just look at Kerry London, the specialist construction broker, which is set to cut jobs as part of a restructuring.

In 2008, about 15 new carriers entered the market writing construction risk – which makes over-population an issue. And with a hardening market seeming no nearer in reality than it was 12 months ago, one has to wonder where the sector is headed.

Rates are competitive, with some underwriters taking sometimes unprecedented steps to attract and retain business. There appears little room for error in ratings and fallout is inevitable. The insurance market needs to take a hard look at the construction industry in its current condition and consider what the next two years will bring.

Meanwhile, fraudulent claims are increasing and, with cashflow coming under increasing pressure, companies will be forced to make cost savings. Many see insurance fraud as an easy option with little consequence. That’s why there is no better time for insurers to work together and agree on principal requirements before premiums can be quoted.

Proving fraud

Under-insurance is one type of fraud that is difficult for an insurer to prove after the event. Dealing with a claim for a multi-site company with assets spread across several locations makes it hard to assess values at risk accurately – especially when the insured suspects what you’re trying to establish.

Construction companies should be made to provide document proof of plant and assets. It’s not difficult; they already have them in their accounting system, as required by HM Revenue & Customs. Brokers should lead this approach because their commission is based on premium spend. This should not be an issue if everyone adheres to the principles agreed.

In the motor industry fleet policies require similar declarations, so why is construction effectively 20 years behind?

The industry has proved it can work together to fight fraud through initiatives such as Construction Equipment Security and Registration (Cesar), launched by the Metropolitan police in April 2007. Cesar, which tags and tracks plant equipment to deter and catch criminals, has resulted in the top five engineering insurers – Allianz, HSB Engineering, Norwich Union, RSA and Zurich – working together in an attempt to stop plant theft.

If this approach were rolled out to general underwriting disciplines in an attempt to prevent under-insurance, it would help ensure this sector of the market received the correct premium income reflective to risk.

Postscript

Jeremy Buckley is managing director of Buckley Scott Associates, a loss adjuster

No comments yet