Sponsored content: Tom Chamberlain, vice president for customer and consulting at Hyperexponential, discusses the underwriters of the future

I’ve seen many specialty and commercial insurers lured by the promise of change, only to be left with poorly integrated legacy systems and the same inefficiencies they’d been grappling with for decades.

While other sectors, such as finance, have evolved into a slicker and more digitised way of working, insurance remains underequipped for the future.

Our recent research explored the current state of underwriting, what Underwriting 3.0 could and should look like and the actionable steps to get there.

Underwriting now

Our research discovered that the typical underwriting workflow is defined more by clunky manual input than seamless processes and dynamic insights.

Over half of an average underwriter’s working week is spent just getting information into the system!

This same sluggishness impacts other aspects of pricing, from quote to bind processes – which typically take more than a week – to peer review, which can take a whopping three to four weeks.

Underwriters are well aware all isn’t as it should be. Chillingly for those invested in the future of insurance, 82% of underwriters didn’t feel confident they would have fit for purpose pricing models in the future.

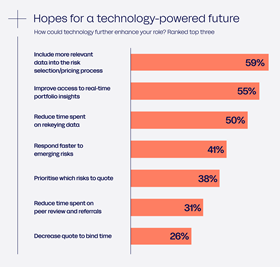

We asked underwriters how technology could enhance their role and their answers revealed both the issues in the current state of pricing and a pathway for the future.

Underwriting 3.0

Let’s paint a brief picture of Underwriting 3.0.

In the future, each decision is underpinned by rich data, the collection of which is effortless and automatic.

Freed from repetitive manual tasks, underwriters have more time for value-added work that is both impactful and fulfilling.

The entire pricing process is exponentially faster and more accurate to drive measurably better outcomes in the competitive market.

Things are beginning to develop in the right direction, with generative AI to ingest unstructured data, predictive models for real-time insights and automation cutting through the slurry of archaic processes.

But while digital innovation is the catalyst for pricing transformation, insurers need to boldly embrace change to truly unlock next-gen underwriting.

Active, concrete efforts need to be made towards:

- Fully harnessing the potential of automation

- Driving greater actuary-underwriter collaboration for better models and better results

- Internal and third-party data at underwriter’s fingertips for faster, data-driven decisions

- Developing underwriter’s portfolio management skills

This isn’t progress for the sake of progress. As Klaus Schwab of the World Economic Forum said: “In the new world, it is not the big fish which eats the small fish, it’s the fast fish which eats the slow fish.”

Getting back to the broker fast enhances your chance of winning business. Insurers that don’t push the boundaries of their platforms and processes will discover their competitive edge eroded as more dynamic players dart ahead.

Underwriting 3.0 is possible today, it’s just a step or two ahead of most organisations.

It’s up to insurers — and it’s up to you — to make it your reality.

To find out more and view the full The Vision and Road to Underwriting 3.0 report, click here.