In April’s issue, Cazana’s strategic partnership manager, Roly O’Neil tells Insurance Times about the value of insights from vehicle data and why it could help write profitable business

When it comes to motor insurance customer journeys there is a constant tug of war between customer experience and the ability to underwrite quality business with an appropriate level of risk assessment.

While insurers have a genuine want to operate in the most streamlined and customer-centric way possible, they will always be restricted by the need for a minimum level of information to allow them to produce an accurate level of pricing.

While customers may feel that the numerous questions asked for a car insurance policy, seem inconvenient and unnecessary, the reality is that the more information that a (lower risk) customer can provide the more preferential the end price is likely to be. However, this theory is not one size fits all. There will be customers that benefit from the broader brush pricing methodology that comes from not having to disclose as much. But on the whole, there are benefits for both insurers and insurees to providing not only the information, but the information in its most accurate state.

How do you please all of the people all of the time?

Simply put, you can’t. There is a constant balance, and a conflict between wanting to guide a customer seamlessly through the journey, ideally without requiring them to pause their enquiry to locate the requested data, whilst also wanting to know that the data inputted is indeed accurate.

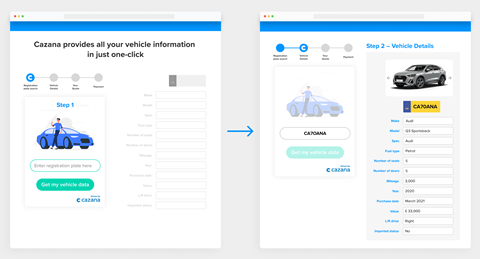

Cazana has been working with multiple companies within the insurance industry on how they can help prepopulate these essential fields, relating specifically to the insured vehicle. With the majority of journeys that have been reviewed, Cazana are confident that they can prepopulate a minimum of 7 fields (this varies depending on the journey).

The impact of question set reductions is well documented. With a mixture of benefits for both the customer and insurance provider. The less the customer has to leave the initial interaction, to look for answers, the greater the chance of progression through the journey and ultimately an increase in conversion.

The alternative to this is that the customer will simply guess to get the job done. As we know, buying car insurance is a necessary chore, not something people tend to do for fun. So, anything that can be done to enhance and simplify the process is likely to increase the chances the customer will complete the car insurance purchase process in a single visit.

From their research, they estimate that between 15% and 20% of dropouts in a standard car insurance journey come from questions relating specifically to the vehicle itself. They can prepopulate a number of these responses including but not limited to those represented in (see fig1)

Not only does this enhance the chances of the customer progressing further through the journey, but Cazana has also learnt that this level of knowledge of the customer’s specific vehicle can improve customer confidence that the provider really does know their car and therefore that they are properly insured at the best price.

Of course, prepopulated data acts only as a suggested response for the customer and it is essential that a customer has the freedom to make any changes they wish. This also helps to create a secondary line of defence against potential fraud.

As the insurer can use the underlying data to flag any changes the customer has made that would impact the overall risk assessment or any future potential claims costs associated. It is very useful, not only to know if a customer has made multiple amendments (sometimes to a single question) but also the extremity of the changes. (e.g., massively inflating a vehicle valuation)

Outside of the pre-populated fields, there are numerous other Cazana led data points that can be utilised to improve fraud prevention or even just help provide an enriched level of data that form part of the post sales or renewals process.

For example, it is not possible to prepopulate the exact modification that a vehicle has as part of the quote process, but the underlying data can trigger a response as to whether a vehicle has any modifications when the customer has answered that there are none.

These sorts of insights can, again, not only provide the insurer with the additional risk related information to accurately price. But also ensures that the customers that have made a genuine mistake are adequately insured. This makes for a much more transparent contract between the insurer and their customer.

This array of vehicle data should not just be viewed as a way to trip customers up or to lead a witch hunt of non-disclosure. But more as a way to enhance and improve the relationship between insurer and customer. Not only can this help increase trust through transparency, but also provides the insurer with the opportunity to add value to the customer experience.

There are multiple ways that knowing about the customer’s vehicle can provide genuine additional points of customer contact outside of the usual annual renewal cycle, for example flagging reminders for when MOTs are due, through to highlighting when a customer is looking to sell their vehicle. Detailed knowledge of the ongoing ‘live’ value of a vehicle also enables insurers to make more informed midterm adjustments and of course more accurate renewal ‘journeys’.

By using Cazana’s vehicle data the insurance industry is bridging the gap between great customer experience and underwriting profitable business.