FCA price walking ban impact on customer, insurers, brokers and aggregators

Briefing by Saxon East

The proposals are out, and although there may be some tweaking, it is almost certain the end result will be a ban on differential pricing between old and new customers.

There are also proposals on premium financing, with a clear warning to players not to charge excessively.

So who will be the winners and losers?

The customer

Prices will increase in year one to compensate for the discounting that previously went on in new business. The winners will be older customers, and those that shop around less.

The losers will be those savvy customers who like to get on price comparison sites every year and shop around for the best deal. This was always the FCA’s intention.

Insurers

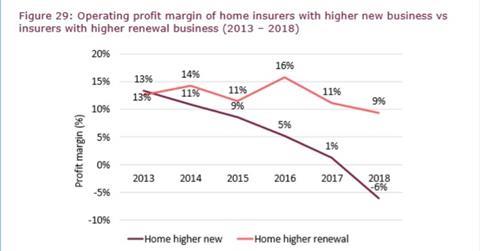

Direct Line is one of the most exposed, with its book of older home insurance policies, and a lot of faithful customers renewing.

This likely has led to much higher profit margins for Direct Line in home, compared to players who have a higher churn (see data below).

Direct Line should have a higher volume of customers it can price walk, as opposed to say, Admiral, with its younger customer book that churns through quicker.

However, direct insurers will still maintain their key advantage in motor. This is their control of the ancillary income – especially the lucrative premium financing, although the FCA has fired a warning in its pricing proposals today about being fair and transparent on premum financing.

This is quite an advantage as opposed to an Aviva or AXA, who to some degree lose out when they go down the intermediated route, as the broker controls premium financing, plus other ancillaries such as legal expenses, breakdown cover and key cover to the brokers.

Brokers

The pricing ban will create some complexity for brokers. Typically, brokers take the net rate from the insurer and then add on the commission. In the first year, brokers deduct heavily from their commission to remain competitive and increase at renewal.

Brokers will need to work with insurers, supplying them with good data and relationship management, to ensure the net rate remains competitive and they can charge a decent commission in year one.

The pricing reforms may lead to more brokers setting up their own MGAs, where they have full control of their pricing.

On premium finance, for those brokers charging high interest to customers, these plans are potentially bad news.

The FCA wants clear transparency and fair interest charges given to customers.

Price comparison sites

The FCA’s pricing differential ban is not helpful for aggregators, and that is evidenced by the way both Moneysupermaket and Gocomapre owner, Goco suffered share price falls after the news was announced yesterday.

Aggregators lose one of their features, that they can help customers get a much better deal in year two of their contract.

This may decrease usage of price comparison sites, as customer stay more loyal to their provider.

No comments yet