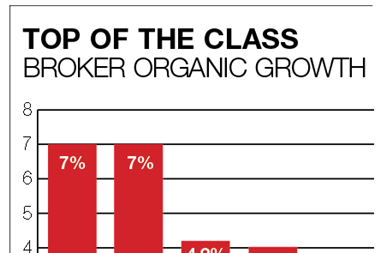

Broker achieves 6.3% organic growth in first half of year

JLT boosted its revenue by 7% as the insurance broker achieved strong organic growth of 6.3% during the first half of 2012.

Total revenue climbed to £441.7m for the six months to 30 June 2012 from £411.3m for the same period in 2011.

JLT’s risk and insurance division reported organic growth of 7%.

Within that segment, JLT Specialty delivered organic growth of 3%, wholesale broker Lloyd & Partners 6% and JLT Re 17%. Other growth areas included Insurance Management (22% organic growth), Asia (18%) and Latin America (14%).

The company said it expected higher levels of organic growth in the second half of the year.

The broker’s after tax profit rose to £59.3m from £53.6m over the same period.

Fees and commissions were up at £439.2m in the first six months of the year from £408.7m in 2011.

JLT’s chief executive Dominic Burke said: “JLT’s continued execution of its clearly defined strategy gives us confidence in our ability to deliver year-on-year financial progress.”

The company’s shareholder equity was down at £302.5m in the first half of 2012 from £326m last year.

JLT’s board declared an interim dividend of 9.6 pence per share to be paid on 1 October 2012 to shareholders registered on 7 September 2012.

The results beat some analysts’ expectations.

Panmure Gordon analyst Barrie Cornes wrote in a a research note: “JLT has delivered a strong set of interim 2012 results, with headline underlying profit before taxation at £89.4m (+12%) well ahead of our £82.6m forecast.

“The beat appears to have been driven by better operating margins at 19.4% (H1 2011: 18.5%). The interim dividend at 9.6p share (+4%) is in line with our 9.7p share forecast.

“Total revenue has increased to £441.7m (+7%) again close to our £446m forecast. A particular highlight is that of organic growth, which on a continuing basis was 6.3% (H1 2011: +7%). The outlook statement is cautiously upbeat, with talk of ‘confidence…to deliver year on year financial progress’.

“Our recently upgraded buy recommendation reflects our view that the trading environment is gradually improving and that JLT is well placed to capture the benefit of rising rates.”

Shore Capital analyst Eamonn Flanagan revised his earnings forecasts of around 2% for 2012 and 2013 on the back of strong revenue, margins and profits.

“The highlights to us of the 2012 interims were: the 6% organic growth in revenue…another excellent outcome; the 90 basis points improvement in trading margin; the 12% growth in underlying earnings and the strength of the margins from the Asian employee benefits,” he wrote.

“Revenue grew by 7% to £441.7m (SCS: £440.4m), of which 6% was organic…we suspect this may put JLT amongst the highest of its peers. The key drivers were JLT Re, up 17%, Asia, up 18%, and Latin America (+14%)…it is these latter two that really distinguishes JLT from its major worldwide peers.

“By division risk and insurance delivered 7% organic growth and employee benefits 5%. Trading profits increased by 13% to £85.7m (SCS: £82.9m) implying a 90bps improvement in trading margin to 19.4% (SCS: 18.7%)…another excellent outcome.

“The key drivers in the improved margins were Australia and Asia, with the 34% margin from the employee benefit business in Asia especially impressive. Underlying pre-tax profits grew by 12% to £89.4m (SCS: £86.5m), with EPS up likewise to 28.5p (SCS: 27.6p).

“The dividend was increased by 4% to 9.6p, broadly in line with our 9.7p estimate. In terms of operational performance we were also pleased to note the small profit from Thistle, JLT’s managing general underwriter (H1 2011: £0.4m loss)…hopefully further improvement will come.

“As for the balance sheet, JLT’s net debt increased to £177.2m (end June 2011: £118m, end 2011: £100m), with the group retaining headroom of £108m. Finally, as a result of lower discount rates, the pension scheme deficit increased by £10m in H1 2012 to £131m.”

No comments yet