Global commercial insurance pricing was also up by 22% in Q4 2020

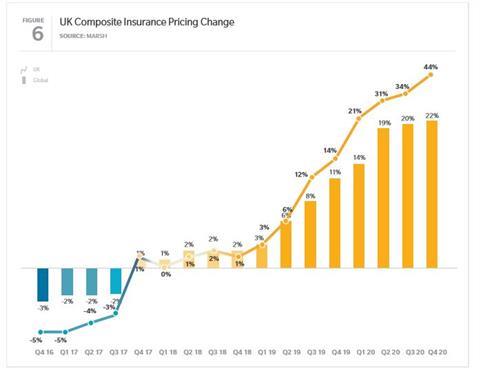

The UK saw a 44% pricing increase for commercial insurance in Q4 2020, according to Marsh’s quarterly Global Insurance Market Index.

The report found that the UK’s figure, combined with the Pacific region’s 35% increase, pushed up the global composite rate for commercial insurance.

Commercial insurance pricing increased globally by 22% in Q4 of 2020, which is the largest increase since the index was initially launched in 2012. This follows year-on-year average increases of 20% in Q3 and 19% in Q2.

Average composite pricing increased in all regions for the ninth consecutive quarter.

Marsh pointed out that the average composite price increase in Q4 was driven by property insurance rates, as well as financial and professional lines.

Property and casualty

Property insurance pricing increased by 24% in quarter four of 2020 due to continuing market challenges - this is consistent with price increases observed in the third quarter.

The broker reported that larger clients experienced higher increases, in the 30% to 35% range, while renewals for larger companies featured significant negotiations on terms and conditions.

Increases for smaller companies averaged 15%.

And exclusions continued to be a concern, especially in terms of Covid-19 and cyber risk.

Meanwhile casualty pricing increased by only 6%, with general liability - such as public and product liability - increasing more than other casualty products for large and mid-size clients; these increases were between 10% to 15%.

The employers’ liability market remained competitive, with pricing increases in the low-single digits.

Capacity continued to reduce for excess of loss placements.

And auto liability clients continued to see pricing increases of 1% to 2% as competition remained.

Financial and professional

Financial and professional lines pricing increased by 90% in 2020’s quarter four - this was largely due to directors’ and officers’ insurance (D&O).

Renewals continued to be “extremely challenging”, with some D&O clients receiving triple-digit increases as capacity departed the primary and low excess markets.

But Marsh believes that new insurers in the market in 2021 should bolster the mid-excess space and provide some relief.

The report revealed that insurers justified large D&O price increases and restricted coverage terms by citing a “deterioration in claims”, a Covid-19 impacted economy, insolvencies, wrongful trading and a lag on claims after government support.

Commercial crime pricing increased by 80% on average as insurers continued to withdraw from this class of business - increases of 100% were common.

For financial institutions (FI) clients, markets continued to monitor capacity and push for higher rates.

Marsh believes pressure on capacity and rates may ease in the future as new entrants come into the market.

Cyber insurance pricing also rose from 25% to 30% due to an increase in the frequency and severity of claims.

Although capacity remained available, carriers closely managed total capacity deployed on any given risk and some insurers introduced co-insurance or specific ransomware strategies.

Utopian pipe dream

Richard Hartley, chief executive of Cytora, told Insurance Times: “These latest figures from Marsh indicate substantial price rises in commercial insurance.

“But they also reveal more fundamental issues being faced by the market today. As pressure from an increasingly competitive and hard market mounts on insurers, there’s still a significant opportunity to generate a lot of new business.”

Hartley explained that to capitalise and grow profitably without compromising loss ratio, insurers need to assess all new business submissions and upcoming renewals with vigour.

“Currently a painfully manual process, this puts strain on the expense ratio and adds to ever increasing operational costs. Instead, those able to reduce costs and identify profitable risks quickly will be able to offer highly competitive rates and faster turnaround times, to brokers and customers alike,” he continued.

“While this previously seemed like a utopian pipe dream, today’s smart insurers leverage digital platforms to digitise submissions and renewals as they flow through the business and connect underwriters to profitable opportunities instantly – all in full alignment with their underwriting strategy.

”The digital streaming of risk will soon become an imperative part of every commercial insurer’s business, and those who move fast can capitalise on this immediately viable opportunity.”

No comments yet