Pricing for the new normal that will emerge post-coronavirus will be difficult for insurers to navigate, says Willis Towers Watson

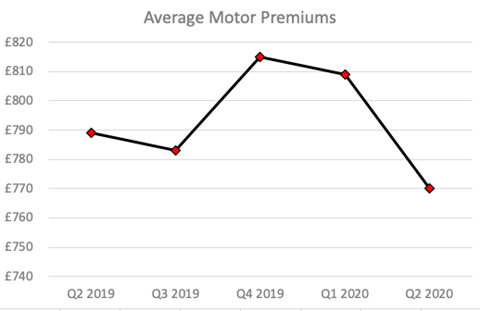

Comprehensive car insurance premiums have fallen by 5% in the second quarter of 2020, the largest quarterly drop in premiums since early 2018.

The Confused.com Car Insurance Price Index in association with Willis Towers Watson also revealed that the average cost of car insurance now stands at £770 following a (2%) decrease over the past 12 months.

Graham Wright, UK lead of P&C personal lines pricing at Willis Towers Watson, said: “The sudden drop in traffic during lockdown and fall in accidents and claims inevitably put temporary downward pressure on the cost of premiums.

“However, a forensic analysis of the complex changes in customer quoting patterns in the last quarter reveals the impact of the pandemic on market dynamics was about more than just price.”

This analysis revealed that fewer young driver quotes were conducted because fewer newly qualified young drivers were coming onto the roads, and also that many consumers were looking for quotes at lower mileage levels.

And this will have had an impact on the average premiums seen across the quarter.

“Some of the initial market-level price reductions seen post-lockdown were driven more by the significant shifts in customer quoting patterns,” Wright said. “And although quoting patterns reverted towards more normal trends towards the end of the quarter, the research has only highlighted further the need for insurers and intermediaries to look closely at how they price for the so-called new normal.”

Pricing for this new normal, however, is something Wright says will present difficulties for insurers.

“Looking further ahead, as we emerge from lockdown and roads become busier, insurers are attempting to predict claims and adjust prices before the full impact of Covid-19 on both medium and long-term frequency and severity trends is known,” he said. “Whilst there are trends that simultaneously point to both higher and lower levels of driving than before – such as less use of public transport balanced with more working at home – a further headache is estimating the impact on severity from broken repair supply chains, more cyclists on the roads and recessionary trends.

“These are just some of the moving parts that will make pricing risk correctly even harder than before the COVID-19 crisis – meanwhile all of the challenges from before such as whiplash reforms, inflation and Brexit remain.”

Read more…Motor insurance and coronavirus-golden era or further misery?

Not subscribed? Become a subscriber and access our premium content

No comments yet