With inflation up and premiums down, the industry is under pressure. But is there cause for optimism?

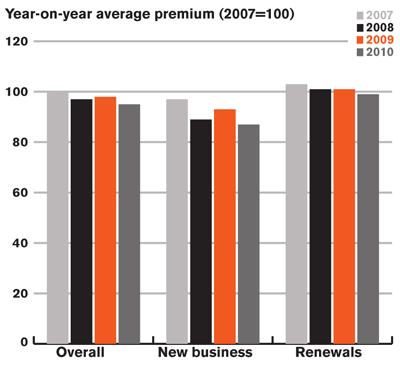

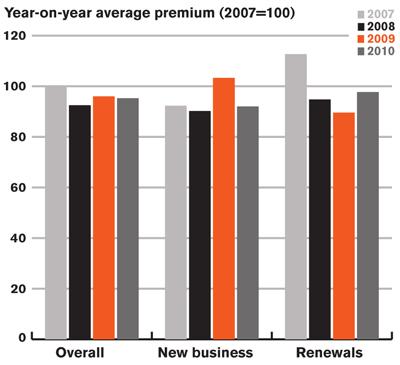

The year 2010 was not a good one for average premiums in commercial lines, as these figures from insurance technology?firm Acturis show.

Acturis co-chief executive Theo Duchen commented: “There is no class of business that the indices cover where 2010 average premiums are higher than 2007 average premiums, with most classes 3%-5% off their 2007 benchmark values.

“When one considers that cost inflation in the same period amounted to some 11%, it underlines the pressures facing brokers and insurers alike.” Both parties will be hoping that the next 12 months fare better.

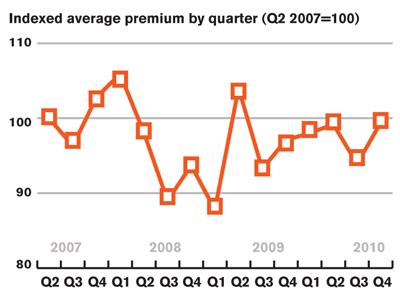

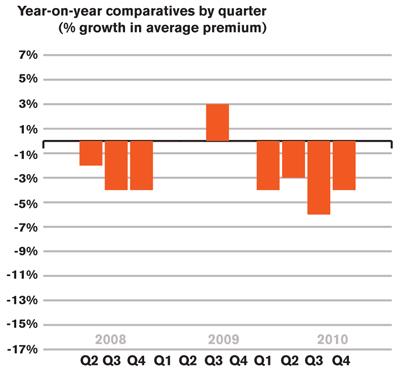

Commercial combined

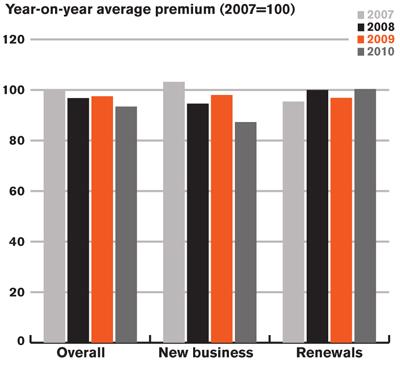

The Acturis commercial combined index ended 2010 some 5% below its 2007 average, and 3% below its 2009 average. This fall was largely driven by new business premiums falling from 98% of the 2007 value to 87%, with renewal premiums only falling from 101% to 99%.

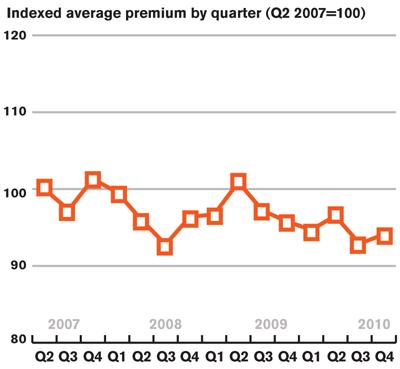

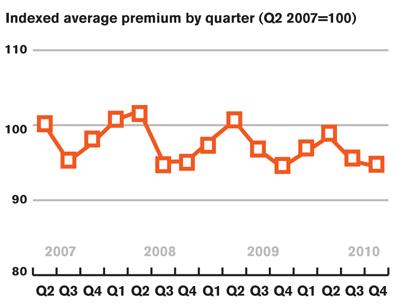

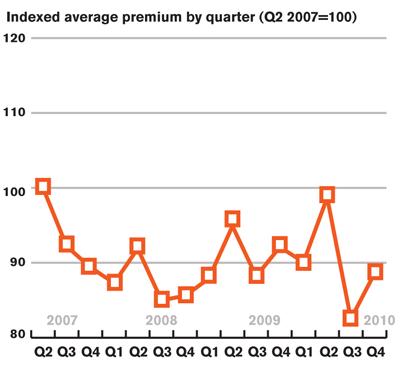

Indexed average premium rose 2.2 percentage points from Q3 to Q4, displaying a similar trend to corresponding times of year in 2007 and 2008. This brings the commercial combined average premium to 94.1% of the Q2 2007 value in Q4, representing a 1.7% decrease relative to Q4 2009.

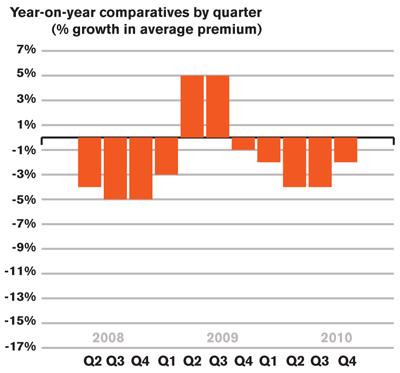

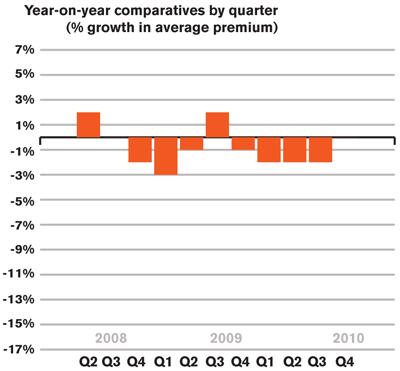

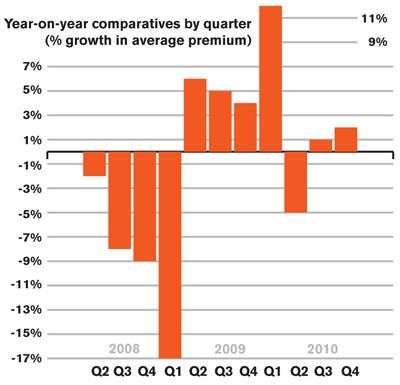

The trend of negative year-on-year by quarter growth since Q3 2009 continues. However, the decrease in year-on-year indexed average premium for Q4 2010 is the smallest of the year (1.7% compared to over 4% in Q2 and Q3), which may be cause for optimism that it could stabilise in 2011.

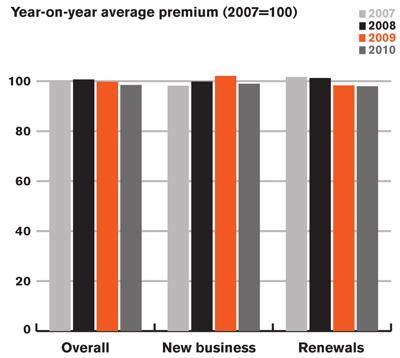

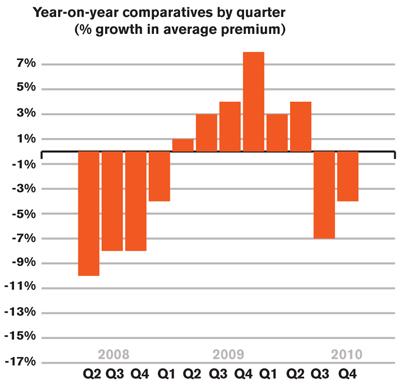

Motor fleet

The Acturis motor fleet index continues to be stable. The overall year-on-year comparative shows little movement – a slight fall from 99.8% of the 2007 value in 2009 to 98.5% in 2010. This fall was a result of new business premiums falling from 102% of the 2007 value to 99%, while renewal premiums stayed steady over the last two years.

Motor fleet premiums remained stable in 2010, with an extremely small drop in average premium between Q3 and Q4, from 95.2% to 94.5% of the Q2 2007 value.

This is almost the same as the Q4 2009 value of 94.4%, which results in the 0% figure displayed by the year-on-year comparatives by quarter analysis.

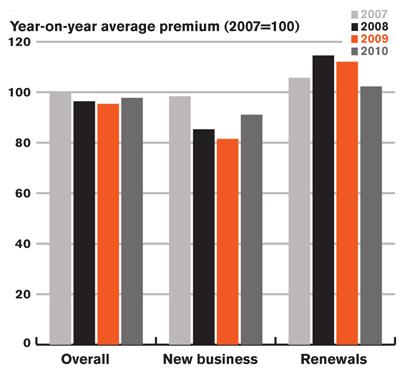

Property owners

Property owners average premium rose to 97.8% of the 2007 value, driven by a strong increase in new business premiums, but tempered by a fall in renewal premiums.

Looking at the indexed average premim by quarter, we see that from a cyclical Q3 drop in 2010, the index has risen to 99.4% of the 2007 value in Q4.

Encouragingly, this represents a 2% increase on Q4 2009, as displayed on the year-on-year comparatives by quarter graph above. This paints a largely positive picture of 2010 for the index.

Packages

Average premiums in 2010 were 93% of their 2007 value, down some four percentage points from 2009. This fall in 2010 was due to a large decrease in new business premiums. Increases in renewal premium (97% of the 2007 value in 2009 to 100% in 2010) could not prevent an overall slide.

There was a significant increase from Q3 to Q4 in 2010, from 93.2% to 98% in Q4. But there was a 4% drop in average premium compared to Q4 2009.

Year-on-year comparatives show negative growth each quarter in 2010, underlining the competitive nature of this product class.

Combined liability

The combined liability index was introduced last quarter. Again, the story for this class of business is not good. The year-on-year comparative index shows average premium fell slightly from 96% of the 2007 value in 2009 to 95% in 2010. This was a result of a fall in new business premiums, counteracted by increases in renewal premiums.

Average indexed premium by quarter recovered strongly in Q4 2010, rising from 83% of the Q2 2007 value in Q3 to 89% in Q4.

The year-on-year comparatives shows a second consecutive decrease. While the Q4 2010 fall of 4% relative to Q4 2009 is troubling, it must be noted that this figure is mainly due to the fall in average premium from Q2 to Q3 in 2010.

Basis of Calculation for Indices

All renewal and new business trades on Acturis System in a particular class for 2007 (Q2 onwards), 2008, 2009 & 2010 with extreme values removed:

Commercial combined £500-£65,000 premiums;

Packages £50-£4,000 premiums;

Property owners £125-£60,000 premiums;

Motor fleet £500 – £60,000 premiums;

Combined liability £125-£60,000 premiums.

Property owners includes commercial, residential and mixed business.