Numbers just don’t add up

Rates have stayed stubbornly low in corporate lines despite a spate of natural catastrophes and volatile financial markets. Insurers’ underlying balance sheet strength is a big factor driving their appetites.

Shore Capital analyst Eamonn Flanagan says: “Insurers are not being given enough credit for squaring up their balance sheets after the early 1990s wobble. There was a divestment out of equity into bonds when insurers found themselves too exposed. There is resilience in balance sheets after a squirrelling away of money.”

Miller corporate specialist Trevor Young says: “Pure UK capacity is still significant. If you add all the growth targets and look at the whole corporate market, someone is going to be unhappy. It doesn’t add up.”

Rates have rolled down for at least seven years, despite short-term spikes after such events as 9/11.

Opportunistic new but short-term capacity is a problem, says Miller head of corporate Ken MacDonald. “After an event like 9/11, new capacity can put on 20%. But, as soon as prices taper off, they walk away. Existing markets suffer.”

He adds: “Anyone can walk along a risk and get a reduction. We like to focus on challenging risks where we can differentiate with our skills.”

RSA this year took the unusual step of withdrawing capacity “where we are unable to meet our target returns”, reporting a 13% decline in mid-market GWP to £228m in the first half. It even drove up rates in some commercial lines, with liability up 4%, property up 6% and motor up 13%.

Of RSA chief executive Andy Haste’s decision to quit, Flanagan says: “He’s more of a doctor; not necessarily the right person to do a caretaking role.”

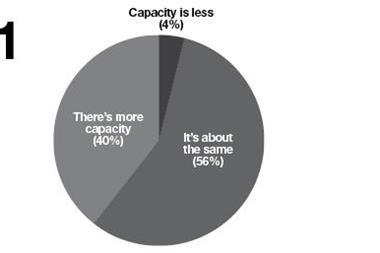

How capacity has depressed rates

To see our full infographic, click on the pdf, right.

Downloads

IT_Knowledge_BigStory

PDF, Size 0.26 mb