The issues facing the market

Coverage

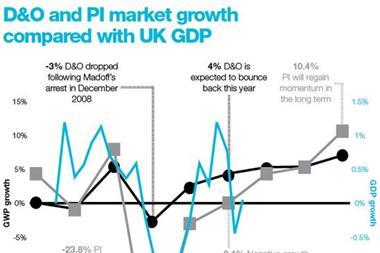

D&O client bonanza

Stiff competition means directors’ and officers’ (D&O) clients are getting better deals than ever as rates soften and coverage is widened.

Underwriters are typically offering to cover investigation costs without charging the client much more in premium. Lockton executive director risk solutions Chris Hewitt says: “Many buyers have taken advantage of vigorous competition among carriers to increase policy limits and extend the scope of cover.”

In professional indemnity (PI), grave concerns remain over policy terms and conditions for covering solicitors, which are still set by the Solicitors Regulation Authority (SRA). There have been cases of insurers having to pay out for solicitors even if there is strong evidence of fraud.

Claims

Recession lag

Recession-related claims have been a problem for the PI market. Solicitors have had to pay higher premiums in response to increased claims.

Claims frequency is also creeping up among valuers hit by the downturn in property. Accountants, architects and IT professionals will need to be watched closely for rising claims.

There hasn’t been the expected rush of claims in D&O. Expected lawsuits against banks in the USA never emerged, partly because lawyers struggled to find solid evidence of wrongdoing.

Hewitt says: “There was expectation and prices moved in response. But it was quickly established that not a lot was coming through, so prices fell.”

Technology

Direct action

The market will remain dominated by brokers but, at the lower end of SME, direct insurance is creeping in. Markel has its own direct arm, offering PI for a wide range of trades.

Entrepreneurs are finding innovative ways to take advantage of technology. Professional Insurance Agents latches its interface onto a broker’s website, enabling customers to buy direct.

Manchester Underwriting Management chief executive Charles Manchester says: “In 20 years, we’re going to wonder why brokers ever got involved in the micro end – with premium levels of £50, £100 or £200. That’s smaller than your average motor premium.”

Capacity

Solicitor flood

Both PI and D&O have been flooded with capacity. The solicitors’ market is fraught with difficulties, yet in the past two years Ukraine-based Lemma, Denmark’s Alpha Insurance and Inter Hanover have pumped in capacity. Expect another year of over-capacity in solicitors’ PI.

Manchester says: “Solicitors will probably make money once in a decade, so if you pick that one year you’ll probably make money out of solicitors.”

Torus entered the D&O market this year. Further capacity is expected to keep rates low in this line.

Lockton’s Hewitt adds: “Players have increased their capacity and looked to capture more premium by writing larger lines of business.”

Regulation

ARP stalemate

Solicitors’ PI has had a turbulent year, with insurers calling on the SRA to scrap the Assigned Risks Pool (ARP). To underwriters’ frustration, the SRA has said it will only end the ARP in 2013. The continuation of the ARP will cost insurers dearly in claims.

In D&O, the Bribery Act coming into force in July will make directors responsible for staff actions. If members of staff breach the act and there were inadequate procedures and controls, directors could face jail.

The act may widen the scope of coverage of policies and encourage more directors to take out D&O cover. In the wake of the financial crisis, there is a trend, especially in the USA, for enforcement agencies to act more quickly.

Once again, this should encourage more bosses to take out adequate cover.

Quinn

Filling the PI gap

The decision by the Irish regulator to put Quinn into administration left a gaping hole in the solicitors’ PI market. The withdrawal of Quinn’s capacity was a problem for brokers that had large agency agreements with the insurer.

There was a knock-on effect for small law firms of typically one or two staff that were covered by Quinn and struggled to find cover on the open market. Fresh capacity from new entrants helped repair some of the damage.

It’s likely that outstanding Quinn claims will partially be covered by the Irish Compensation Fund, the government scheme to pay for unpaid insurance claims.

Quinn’s administrators would need to seek Irish High Court approval to access the funds, which could result in an uncertain wait for brokers wanting their claims settled.

Expansion

Litigation dangers

PI has expanded as the UK becomes more aware of the threat of litigation. For example, there has been debate within the Department of Health over whether PI should be compulsory for nurses and midwives.

Complementary therapy PI is expanding, as it is for contractors, especially if they are working for a government or local authority that demands coverage.

Manchester says: “If you do any work for local authorities – even if you change the light bulbs – people often require you to have a certain level of PI, and that’s increasing the number of low-risk cases coming to market. A light-bulb changer doesn’t have much PI exposure but he might have to buy a policy.”

No comments yet