’If we can’t service the broker quick enough, we’d lose the sale, they lose the sale, conversion drops and ultimately it hurts all of us,’ says head of broker development

The latest managing general agent (MGA) data from Insurance Times paints a clear picture that such firms have become very popular among brokers.

In the publication’s Five Star Rating Report: MGA market 2023/24, released in January 2024, figures show that 82% of UK-based brokers wanted to work with MGAs more over the next five years, while 81% agreed that such firms were becoming a viable alternative to big insurers.

A total of 1,850 brokers provided feedback for the report, which investigated brokers’ opinions, attitudes and levels of satisfaction with MGAs.

The report’s findings do not come as a surprise, as the MGA market has become an increasingly important subsection of the UK general insurance (UKGI) landscape, fuelled by new entrants and new products.

And, with this part of the insurance market bringing more choice to brokers and consumers, it is also no surprise that there is a need for MGAs to provide a strong service.

The necessity for this was highlighted in Insurance Times’ report, with most brokers (41%) stating that good service was what they valued most from MGAs.

“Service and flexibility is probably the biggest thing that brokers look for,” Barry Driscoll, chief trading officer of broker Brown and Brown’s underwriting division, said.

“It’s not about financial benefit or commission – they absolutely value service, flexibility and underwriting more than anything else.”

Tim Baxter, head of broker development at Prestige Underwriting, added that while service was key, this can be challenging as demand from brokers increases – especially during busier periods.

“If we can’t service the broker quick enough, we’d lose the sale, they lose the sale, conversion drops and ultimately it hurts all of us,” he said.

“We do try and increase that support, but it’s a challenge to get the right balance of resource versus demand.”

Capacity

The increase in broker demand comes at a time when capacity, which is capital that determines the amount of risk an MGA can underwrite on behalf of insurers, has become a key talking point.

Read: In Focus – What are the competitive advantages of MGAs for underwriting?

Read: Capacity for MGAs is ‘challenging’ as traditional avenues are ‘being more selective’

Explore more MGA-related content here or discover other news analysis stories here

For example, the 2023/24 Insurance Times MGA Data Book – published in line with the Five Star Rating Report: MGA market 2023/24 report – highlighted brokers’ concerns over what they have seen over the last year across the MGA market.

Considering how important the underlying capacity arrangements of an MGA were, 45% of broker respondents said this was very important, while 24% said it was somewhat or extremely important.

However, Baxter commented that his firm had spoken to brokers that had been left “high and dry” by other businesses amid “significant” adjustments in rating and underwriting appetite.

And Driscoll warned that “where you see shifting sands in capacity is generally where the result is not right”.

He continued: “Where I have seen it in the past [across the market], shifting sands on capacity is driven by poor results and insecure underwriting decisions.”

Stephen Gibson, managing director of MGA Avid Insurance Services UK, added: “If you don’t have your strength, consistency and relationship with capacity, you are on eggshells and it might be a short-lived relationship you have with brokers – how much value you can deem over that period of time is questionable.”

In turn, John Inwood, underwriting director at Avid, said that the “quality of information and quality of decisions that you make hopefully mean that insurers stick with you”.

And Gibson said that MGAs were more likely to get a ”favourable response” for their propositions that were backed by capacity that has been secured long-term.

“Fundamentally, capacity is the biggest single thing that MGAs need to be very mindful of,” he added.

“You are playing with someone else’s money and ultimately, we have to be so respectful of that.

“If you have longevity of capacity and strength of relationship, you are more likely to get a favourable response to improve and innovate your products.”

Partnerships

Brokers’ capacity concerns came after providers got a grip on their exposures and reserving strategies following detrimental economic headwinds.

For example, in January 2023, figures from the Office for National Statistics showed UK inflation at 10.1%, as measured by the Consumer Prices Index.

“As we see capacity drop out of the market, which we have seen over the last 12 months, prioritising the right partnerships has become more and more important,” Driscoll said.

According to the Five Star Rating Report: MGA market 2023/24, when brokers were asked what the most important aspect of good service was, the majority (43%) said expert relationships.

Driscoll said his firm had adopted a partner approach with its distribution model that had “evolved significantly” to meet the needs of brokers.

“We have robotics and automated workflows running through our business now that allow us to focus on our partnerships, enquiries and renewals,” he added.

“We’ve introduced a work prioritisation for our partner brokers, so their turnaround is better and they are serviced more frequently.

“It’s [also] about providing relationships with underwriters [and] flexibility in the proposals that go out, so [the process] is more meaningful.”

Baxter said that MGAs with stable capacity were more likely to secure new partnerships to grow their business books.

“It has been a long-standing core focus and priority of ours – the capacity rating,” he added.

“[Capacity] is a big tick in the box for the broker and that certainly helped in conversations and new partnerships we have entered into.”

Specialism

On top of solid partnerships helping to bolster service, the Five Star Rating Report: MGA market 2023/24 also flagged that brokers valued MGAs that can provide services in niche classes.

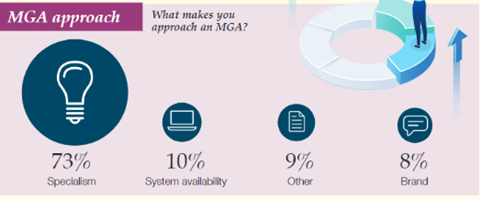

When Insurance Times asked brokers what made them approach an MGA, 73% stated specialism, trumping other factors such as system availability (10%).

This is linked to the fact that niche schemes have been the bread and butter for many brokers over the last few years.

Broker schemes typically provide cover that is tailored to address the specific needs of a certain demographic.

Baxter said his firm would aim to bolster service in this area through the use of online portals, which ensures brokers receive a range of support.

“We try and create efficiencies through the portal journey and the rating engine that sits behind that,” he explained.

“Then, the underwriting service team will support brokers via telephone, email, live chat facilities – we’ve tried to create as many routes as possible to our team.”

Driscoll added that there are “changing customer needs that an MGA can support through niche schemes”.

“Customer needs are changing significantly over time, whether that is environment led, or exposure led, [for example],” he continued.

“Within the insurance market today, MGAs are a critical and fast growing part of that.

“Capacity partners benefit from working with MGAs – their expertise and agile capabilities improve distribution.”

His career began in 2019, when he joined a local north London newspaper after graduating from the University of Sheffield with a first-class honours degree in journalism.

He took up the position of deputy news editor at Insurance Times in March 2023, before being promoted to his current role in May 2024.View full Profile

No comments yet