With the liability for autonomous vehicles placed at the doorstep of insurers, Insurance Times explores how the recent government consultation on automated lane keeping technology could prove to be a headache for insurers amid a growing list of safety concerns

On 18 August, the government launched a consultation into the safe use of the automated lane keeping system (ALKS) on British motorways, issuing a call for evidence to explore whether ALKS complies with the definition of automation under the Automated and Electric Vehicles Act 2018 (AEVA).

According to the Department for Transport and the Centre for Connected and Autonomous Vehicles, ALKS “is vehicle technology designed to control the lateral, left and right, longitudinal, forward and back movement of the vehicle for an extended period without further driver command.

”During such times, the system is in primary control of the vehicle and performs the driving task instead of the driver at low speeds on motorways”.

Defining the system’s level of automation and any potential safety red flags is important for the insurance sector, as the AEVA dictates “that victims of a collision involving an automated vehicle (AV) will receive compensation from the vehicle’s insurer in the same way as they would from the insurer of a conventional vehicle”.

This means that if ALKS is classified as an autonomous driving system and cars featuring ALKS are listed as autonomous vehicles under AEVA, then motor insurers will be liable for claim payouts rather than the vehicle’s manufacturer.

Neil Ingram, head of motor product management at DLG, explained: “Without the Act, the vehicle would be driving itself and anybody that was harmed in an accident caused by the vehicle would essentially have to go and sue the manufacturer for any damages.

“We have compulsory motor insurance in the UK for a reason and that is serious injuries can occur and we want to make sure that there’s a very easy and fair way to claim for compensation.

”So, it was felt that the right thing to do for customers and potential victims of accidents would be to essentially mimic and replicate that. What happens is the Act places that liability on to the motor insurer.

“We believe that’s the right approach because it means that somebody who is a victim of an accident can easily, quickly and fairly claim compensation rather than having to try to go through the courts to identify the manufacturer at fault.”

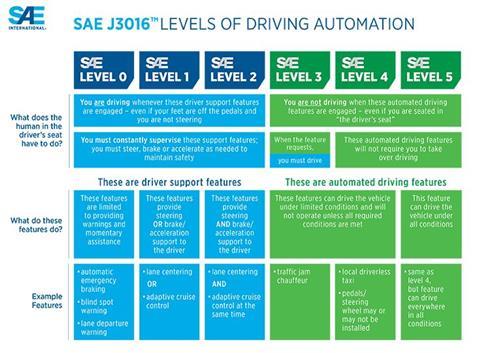

Levels of automation

When determining how autonomous different driving systems are, insurance professionals turn to engineering association SAE International’s ‘Levels of Driving Automation’ standard, which defines six levels of driving automation (see chart).

Vehicles classified as a level two, for example, are described as being assisted rather than autonomous, so the car will just support the driver – this could include with steering or braking.

Level four, on the other hand, is considered to be completely autonomous, where the car can drive itself without any input or guidance from the vehicle owner.

The crux of the matter, according to Matthew Avery, director of insurance research at Thatcham Research, is that ALKS is classified as level three – a step ahead of assisted driving, however it still may need to signal a hand-back request to the driver if it encounters a situation that it cannot cope with, for example if another vehicle has broken down in the motorway lane it is travelling in or if it needs to avoid debris in the road.

“Level three [is] automation whereby the driver is supported, the car will do all of the operational safety, but if it can’t cope, it requires you to hand back control very, very quickly.

”So, if something’s there and it doesn’t know what’s going on, it requires you to take back control and the problem of course is that is very confusing to someone who is using automation.

”They believe you can press a button, then go to sleep or do something else. With this automation, you can’t. There are big safety issues,” Avery said.

Avery has a number of safety concerns around ALKS. He explained that the system is only designed to drive vehicles in a straightforward motorway lane, so it is not able to change lanes, for example to avoid pedestrians standing by a broken-down car.

Furthermore, if the driver does not respond to a hand-back request because they are engaged in another task, like reading or having a nap, then rather than find “safe harbour” on a hard shoulder, ALKS will simply stop in the car where it is in the motorway lane.

Also, since ALKS is intended to be used at full motorway speed, Avery added this is “hugely more challenging for a system to be able to react at 80mph”.

The ABI shares Avery’s safety worries. It said: “We have some serious concerns about ALKS not being able to drive safely in some circumstances without the driver monitoring the system and, therefore, we believe they should be classified as ‘driver assisted systems’ and not considered to be fully automated.”

Insurance implications

For Ingram, the insurance considerations around ALKS are multi-faceted. Firstly, there is likely to be an increase in claims severity “because for the first time the person sat behind the wheel will be considered a passenger and not the driver. We’ll have one extra claimant per claim”.

Ingram also feels that without thorough testing, it will be difficult for insurers to price and underwrite the risk of cars with ALKS technology accurately, especially considering the safety threats raised by Avery.

“As an industry, we want to be able to say look, these vehicles will be safer and therefore that will clearly impact on insurance premiums – it’s very difficult for us to say that and my concern is, actually, we could see things go the other way, particularly if it turns out that these systems are less safe than humans,” he said.

“Without Thatcham really being able to test these vehicles and understand how each of these different systems respond and react in certain scenarios and situations, it’s very, very difficult for us to understand the risk and therefore to accurately price and underwrite these vehicles.”

Pursuing claims could also prove problematic. Ingram explained: “Under the Act, we’re liable and it’s a strict liability placed on the motor insurer and we’re fine with that as long as it is a genuine autonomous vehicle.

”Our ability, then, to potentially pursue a claim from the manufacturer, we’ve always felt that’s going to be quite difficult. There’s no additional rights of recovery under the Act. We’d be relying on the common law and current product liability laws and there are a number of defences manufacturers could use.

“It may not even be the manufacturer. As the vehicle rolls off the production line, absolutely that’s the manufacturer, but if the vehicle’s now three, four, five years old and been tampered with at various garages [in] the market repair network, it’s very difficult to identify if someone’s made a fault somewhere that’s ultimately led to that accident, so insurers would be on the hook.”

There’s also the question of whether insurers are able to obtain the relevant data to pinpoint whether the human or the car was driving at the time of an accident – for example, the car may only detect an incident has occurred if the airbags are deployed, so low speed accidents, which account for 90% to 95% of accidents according to Ingram, could go unnoticed by automated systems.

“Without the data to establish who was driving the vehicle, it’s going to be very difficult for the Act to work, for us to be able to say yes, the vehicle was driving itself and the person sat behind the wheel, we consider a passenger,” he added.

Aside from the insurance impacts, there are also legal considerations, Avery said. For example, the Road Traffic Act will need to be amended to accommodate ALKS.

”Also, ALKS is not sensitive to variable speed limits or the red crosses displayed above motorway lanes, so “there could be legal issues with using these vehicles and the vehicles simply not responding as they think it should”.

Time frame indications

The government’s consultation closed on 27 October.

According to the consultation documentation, the responses gathered from this call for evidence will help inform a consultation paper, which will be published by statutory independent body the Law Commission at the end of the year.

Furthermore, a public consultation is planned for late 2020 to consult on the detail of any proposed changes to secondary legislation and the Highway Code - this will include a summary of the responses to this most recent call for evidence.

Alex Glassbrook, barrister at Temple Garden Chambers, predicts that a decision regarding ALKS’s automation level will be confirmed in spring 2021.

Broker involvement

Although Ingram said there is no direct impact from the consultation on brokers, Alex Glassbrook, barrister at Temple Garden Chambers, believes it is important they are educated about the AEVA in order to better advice and assist clients.

He explained: “Many new vehicles require software updates. The AEVA 2018 allows an insurer to avoid liability under that Act if the user has not installed safety-critical software. So, buyers of insurance need to be aware of the Act.

“From a practical perspective, brokers also need to be aware of the legal landscape of electric and advanced vehicles because the numbers of those vehicles are increasing and some technologies on those vehicles – for example, tracking-type technologies – might help to reduce a premium.

“Availability and cost of insurance is likely to alter relatively quickly as those vehicles become more widely available, so users of new technology might turn to brokers for advice as to their insurance rights and obligations.”

This becomes more important when considering consumers’ understanding of automated vehicles themselves and, therefore, how to use them safely – Avery added that Thatcham research showed that many drivers believe they are operating automated vehicles today.

He continued: “We have to involve the consumer in this and frankly the consumer does not understand the sorts of systems we have got on cars today. We’ve done several surveys of people asking them about automation and a lot of them think they’ve got automated vehicles today.

“[Automated vehicles are] going to look like the car of today with just an additional system, which then leads to some very big safety concerns about people just misunderstanding what they’re doing.

“There could be also consumer issues because if drivers don’t trust these systems or there are problems with them, they will reject it. And they might reject it prematurely.”

Glassbrook added: “From the perspective of the insured, it is important to understand the insurance obligations of driving an automated vehicle.

”It will be important to know whether or not the vehicle you are driving falls within the AEVA 2018 definition of ‘automated’. That is presently both unclear as a matter of law - hence the call for evidence - and might be unclear as a matter of fact, as it might well depend upon which functions have been activated, whether by default or by the user, on the vehicle.

“The way we drive has changed; new vehicles might seem more like a smartphone or computer than a car, because they require software updates. They are new types of transport. Users and insurers need to familiarise themselves with these new cars, just as they would with other new devices.”

‘Under no illusions’

For Matthew Avery, director of insurance research at Thatcham Research, ALKS technology is not automated and should not be considered so by consumers.

He explained: “We’ve produced a document with 12 key elements around safety. It’s about safe automated driving.

”What this basically does is it highlights 12 key things that insurers think make a safe automated vehicle. And this ALKS regulation only addresses three of those 12.

”So, we think three of the things it does, we think ‘yeah that’s automated’, but another nine of them, it doesn’t comply with, which is why we would say ALKS must be regarded as an assisted driving system - that’s level two, [as in] you have to keep watching it.

”It’s not automated and the vehicles should not be listed as automated and the driver should be under no illusion that the system is automated.

“Bear in mind these cars cannot move lanes. If you’re not watching, you’ll either create a crash, be involved in a crash or at least commit a road traffic offence.”

No comments yet