Insurance Times looks at what Ardonagh will need to achieve moving forward off the back of its improved 2018 results

First the good news.

Ardonagh has improved its cashflow position to £67.7m for 2018, well above the £3.3m it posted for the nine months.

This is largely due to a £172m debt raise in November and £66m of selling non-core business, such as the old Towergate commercial underwriting arm.

Buttressed by £216m in liquidity, Ardonagh is financially sound in the near term.

This will be a relief to service providers and insurer panellists to Ardonagh, who may well have looked at the nine-month 2018 results and reflected on the cash crunch which brought the old Towergate to its knees.

David Ross aims high

The goal now is to turn the projected earnings of £186.5m into a reality.

This will means achieving free cashflow - operating cashflow minus capital expenditure (note this excludes company sales or financing) - above £150m.

This is the fairest and truest metric of the underlying performance of a consolidator such as Ardonagh.

If David Ross and his team can do that, it will be a job well done.

Key to achieving this will be the cost savings - with as much as £36m identified in the near term - and winding down the business transformation and high capital expenditure.

This is a constant strain on cashflow, although there is a valid reason for it.

As great as Peter Cullum and Andy Homer were with their entrepreneurial flair in building up the old Towergate, there was still quite a lot of investment and integration needed.

Combine this with meshing it together with the Ardonagh-acquired firms, and you can understand why there has been such high costs involved.

These costs include things such as the new broker trading platform in Acturis, superior back office functions and tidying up all the different legal entities.

Another important piece in the strategic jigsaw will be integrating Swinton. The Ardonagh team believe most of the restructuring was done by Covea, so there will be some costs, but not a significant strain on cashflow.

Finally, Ardonagh must show that the underlying businesses continue to grow organically - and there is some evidence in the 2018 results that this is the case.

If Ardonagh can complete these three things - reducing costs, integrating Swinton and continuing organic growth - then they have a chance of becoming a business throwing off plenty of clean cash.

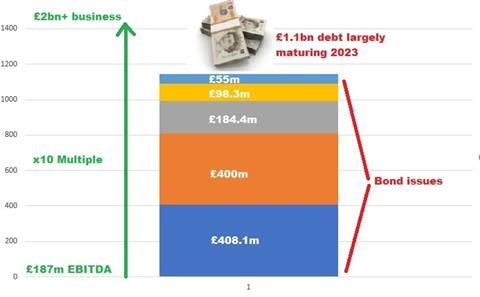

That will need to be done well before 2023, when most of the £1.1bn debt needs dealing, and the new owners will need a good multiple as they likely seek new investors.

Over to you, Ardonagh.

No comments yet