Insurance DataLab takes a deep dive into the UK’s property insurance sector, exploring market trends and pinpointing improving insurers

The UK property market has reported an improved underwriting result for 2021, but it still experienced an underwriting loss despite a sharp drop in claims.

Analysis of the latest insurer Solvency and Financial Condition Reports (SFCRs) by Insurance DataLab, published exclusively by Insurance Times, found that UK property insurers reported a loss-making aggregate combined operating ratio (COR) of 103% last year - down from 110.5% in 2020.

Much of this improvement came from a 17% decrease in gross incurred claims as the property market rebounded from a surge in Covid-19 related claims.

Figures published by the ABI in 2021 found that Covid-19-related business interruption (BI) claims, which typically fall within an insurer’s property book, accounted for around £2bn worth of claims incurred in 2020, out of a total of £2.5bn coronavirus-linked claims across all business lines, including travel and life insurance.

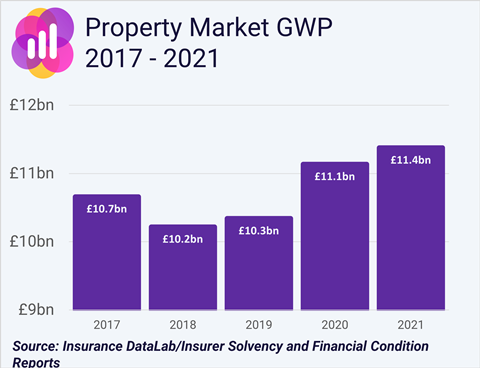

As a result of this surge, overall property claims in the UK for 2020 rose to more than £8.3bn, up from £6.8bn the previous year, before falling back to £6.9bn in 2021.

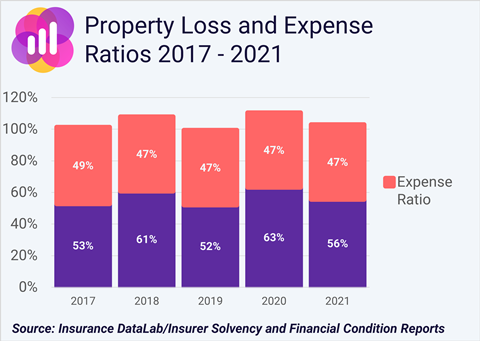

This resulted in the UK property insurance market reporting an overall loss ratio of 55.5% in the most recent round of SFCRs – a reduction of 7.7 percentage points on the 63.2% loss ratio reported for 2020.

When it comes to expenses, the property market has been steadier. Operating expenses have climbed by a little over 1% in the last 12 months to £3.6bn, creating an aggregate expense ratio of 47.5%.

This latest expense figure does, however, mark a reduction on previous years - operating expenses peaked at £3.9bn in 2017, leading to an expense ratio of 48.5%.

Despite the improvement in the aggregate loss ratio, 2021 marked the fourth year out of the last five that UK property insurers have reported an underwriting loss - the market only achieved underwriting profitability in 2019, when the market reported an aggregate COR of 99.4%.

Market movements remain a concern

Property insurers continue to face ongoing market conditions that will add upward pressure to the cost of claims.

For example, the UK’s exit from the European Union and the ongoing impact of the Covid-19 pandemic have created supply chain issues and a shortage of skilled labour that continues to affect the construction industry.

Timber and plaster shortages were particularly acute throughout 2021 and while demand has started to stabilise for these goods, the ongoing energy crisis – which saw average energy bills rise by 54% in April 2022 according to the Office of Gas and Electricity Markets – has led to a surge in costs across energy intensive industries, such as concrete, steel and cement.

This will only add further fuel to the fire driving increased repair costs within the property insurance market.

The ongoing war in Ukraine is also expected to exacerbate these trends over the coming months.

Methodology

Insurance DataLab analysed property underwriting results as reported by UK insurers in their latest Solvency and Financial Condition Reports (SFCRs) for 2021.

Where insurers are part of a group operating structure, solus entity SFCRs were used, with the premium, expenses and claims figures in these regulatory returns used to calculate the loss ratio, expense ratio and combined operating ratio (COR) for each insurer.

Market figures were calculated using the aggregate position of the 43 property insurers included in this analysis.

Price movements may ease pressure

While insurers continue to face rising claims costs, they may find some financial respite in the home insurance market where new business rates have risen since the introduction of the FCA’s new general insurance pricing practices regime in January this year.

The new rules banned the act of price walking, which traditionally saw insurers charging higher rates for renewing customers compared to new business.

However, the FCA’s action has resulted in a 2.3% increase in average premiums for new customers in the three months to April 2022, according to the latest figures from market research firm Consumer Intelligence.

Indeed, Consumer Intelligence’s May 2022 Home Insurance Price Index revealed that average home insurance premiums in the UK have climbed by 6.3% over the preceding 12 months, taking these premiums to the highest level recorded since the company started monitoring home insurance premiums in February 2014.

In commercial lines, premiums have also been on the rise. Marsh’s May 2022 Global Insurance Market Index, for example, revealed a 9% year-on-year increase in property premiums across the first quarter of 2022.

This uptick does, however, still represent a slowdown on previous property premium increases - these peaked at a 24% rise in the final three months of 2020, according to Marsh.

The uncertainty created by these changing market dynamics has led to increased levels of reinsurance within the property market, with around 42.7% of premiums ceded to reinsurers in 2021.

This is up more than 10 percentage points compared to 2017, when insurers reinsured less than a third of property premiums.

While this strategy will help to reduce overall exposure to property claims going forward, it is to the detriment of net earned premiums, which have already fallen by more than 7% since 2017.

UKGI’s top performing property insurers

While ongoing market conditions have forced the UK’s property insurance sector into loss-making territory in four of the last five years, there are still insurers that are outperforming the market and delivering strong results.

Of the 43 property insurers included in this analysis for 2021, 20 were able to report an underwriting profit with a sub-100% COR, while 23 fell to an underwriting loss.

![]()

Tradex was the top performing insurer in terms of its underwriting performance - excluding those that reported negative claims incurred or operating expenses - with a COR of 30.7%.

Although, with gross written premium (GWP) of a little under £1.1m, it was one of the smallest property insurers included in this analysis.

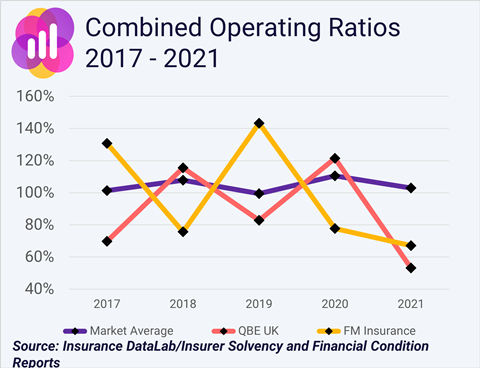

When it comes to larger insurers – defined as those with more than £100m of GWP – it was QBE UK that rose to the top, with a property COR of just 53.2% for 2021.

This result came off the back of the insurer’s market-leading 13.2% loss ratio for last year – a marked improvement on the previous year’s 84.3% loss ratio – and an expense ratio of just 40%.

QBE’s improved performance was driven by an 82% decrease in net claims incurred in 2021 to £23.4m (2020: £126.5m) – this knocked around 71 percentage points off the insurer’s loss ratio.

This improvement was, however, partially offset by a 27% increase in its operating expenses last year to £71m (2020: £55.8m), adding three percentage points to QBE’s expense ratio.

The insurer was also able to report profitable growth over the last 12 months after it grew property GWP by 20% to £267.1m and net earned premium (NEP) by 18% to £177.4m.

The second most profitable property insurer in 2021 was FM Insurance, with a COR of 67.1% – a 10.6 percentage point improvement on the 77.7% COR it reported for 2020.

This improvement was driven by a 30% reduction in the insurer’s operating expenses to reach £11.3m last year (2020: £16.2m). This knocked more than 16 percentage points off its expense ratio.

Meanwhile, FM Insurance’s net claims incurred rose by 25% in 2021 to £10.2m (2020: £8.2m), with the insurer’s loss ratio climbing by just under six percentage points.

Despite the increase in claims, FM Insurance was still able to grow profitably over the last 12 months, with GWP increasing by 9% to £157.6m (2020: £144.3m) and NEP up 2% to £32.1m. The insurer reinsured 78% of its property book in both 2021 and 2020.

No comments yet