Internet giant is said to be experimenting with ideas on how to take forward the new acquisition

Google’s £37.7m acquisition of BeatThatQuote last month sent a shockwave through the price comparison market and sparked an industry-wide guessing game as to what the technology giant would do next.

Behind closed doors, the big four aggregators – GoCompare, Moneysupermarket, ComparetheMarket and Confused – will have concerns that Google could use its technological might to grab market share. And by remaining tight-lipped, Google has only fuelled suspicions.

But an Insurance Times investigation can reveal the true story behind Google’s decision to purchase BeatThatQuote.

According to a source, who has close links with both companies, it began when Google became convinced that customers were struggling when searching for a credit card. This, it claimed, was evident from the amount of rekeying and use of the ‘back’ key by users of the search engine.

So Google decided to create its own credit card comparison site: www.google.com/comparisonads/ukcredit.

When this proved successful, Google wanted to expand its comparison offerings in personal financial products, but lacked contacts with banks, insurers and investors.

The source says: “I think Google probably wanted something right at the top of the page; something that would give the customer the answer they were looking for.

“To do that well in this industry, you need somebody with a lot of contacts, somebody with really deep ties with insurers, to get their information – and that’s not available on any old website. That company was BeatThatQuote.”

Conflicts of interest

Since the acquisition, market watchers have noted two potential conflicts of interest.

Aware that customers often access aggregators by keying search terms into Google such as “car insurance” or “cheap car insurance”, commentators ask whether Google could promote BeatThatQuote to the top of the search engine rankings.

BeatThatQuote also has a site comparing a range of financial products. And it supplies technology for other comparison sites, such as MSNCompare, owned by Google’s biggest rival, Microsoft. How will these business conflicts be resolved?

The source insists Google would not play the system. “The minute people think Google is fiddling with something on the page, they’re going to lose trust in the search engine and they’re going to go elsewhere,” the source says.

“And the fact is that for personal financial products, buyers don’t even go to Google; they go direct to MSM.com or they go to moneysavingexpert.com. All these sites talk about their direct site traffic. So I don’t think they’ve got that much to fear from Google.”

The source believes there will be no rush for Google to expand BeatThatQuote; the internet giant is still “experimenting” with the site.

BeatThatQuote currently performs as a standalone business and has so far not received a single penny in advertising money. One insurance director said: “That’s very much the impression we’re receiving from Google – that they’re experimenting. It must be nice to have so much money that you can spend £37m on a business and not have to worry about it.”

But Google has made a string of purchases in recent years that have flopped, so could BeatThatQuote end up like the others?

BeatThatQuote is relatively unknown, so Google faces a big challenge building up the brand without a large-scale TV advertising campaign. That’s something Google is unlikely to embark on – BeatThatQuote turned in a £2m loss at the end of last year.

By comparison, the big four aggregators have years of experience in a fiercely competitive space – they are building up exceptional brands and are pulling in a healthy profits by giving the customers what they want: cheap deals.

GoCompare, one of the few insurers to speak on the record for this article, says it is relaxed about the deal. If a supermarket giant such as Tesco can’t crack the comparison market, why should Google, it asks.

The insurer’s finance and marketing officer, Anders Nilsson, said: “The market remains attractive to new entrants. Generally, new entrants bring improvement to the whole market – that is part and parcel of the way markets operate – but we’ve got nothing to fear from that. Everyone thought Tesco was going to take over the market, but it didn’t happen.”

Nilsson added that his company had concentrated on developing the insurance comparison experience over recent years.

“We’ve spent four years working with our insurance partners and our customers to make the quote experience as smooth as it can be,” he said. “And we’ll continue to do that because it is in the best interests of our customers."

Advertising advantage

One area in which Google could hold sway over the aggregators is the amount of money they pay to advertise on the search engine.

But even this is not a clear-cut position, says the source. “These companies are advertisers with Google. If Google suddenly decided to raise advertising costs, saying: ‘Hey, your ads against these insurance sites are going to cost 10 times as much’, they’re just going to walk away and advertise elsewhere.

“They have tons of traffic, lots of which is direct, they’ve got great brands, and they’re all over TV. I don’t think they should be worried about Google,” says the source.

Perhaps the issue is not so much what the big four have to fear from Google, but what Google has to fear from them.

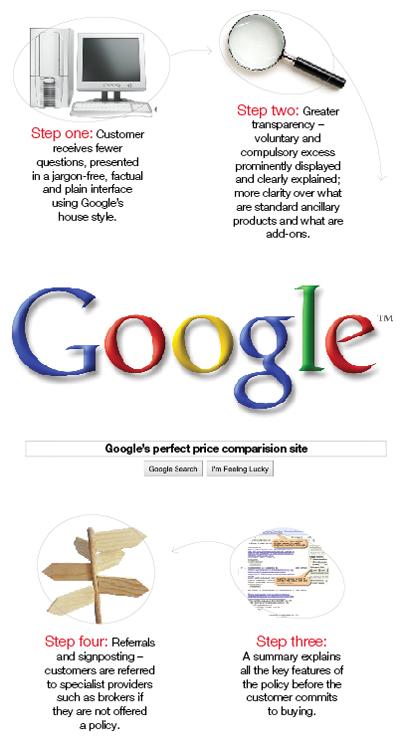

Getting the online edge

Google should be able to exploit areas in which aggregators still fall short, such as transparency over excess and

add-ons. ABI guidance released in December stressed the need to improve these areas.

A poll of 1,703 shoppers by consumer magazine Which? in December showed that fewer than half of those who use price comparison sites are satisfied with the service provided. A satisfaction rating of 46% was 2% down on the previous poll, conducted in September 2009.

Aggregators are at a crossroads in their question set. High levels of motor fraud and a surge in bodily injury claims in the past two years could force insurers to develop more complex pricing models. Insurers would require more questions and that could make the customer experience of aggregators more difficult. In turn, that could force more customers to go direct to the websites of insurers such as Aviva, Esure and Swiftcover.

If rate increases bring motor back into profitability, insurers may decide that the time is right to pull in more customers and they may ask for a simpler question set.

No comments yet