Only a new business model, a startling innovation or clever niche marketing can help UK motor insurers recover from the invasion of the aggregators

The UK motor market is now in a situation similar to the airline industry in that competition is making profitability elusive. The situation is not likely to improve until some consolidation occurs or a new business model is developed.

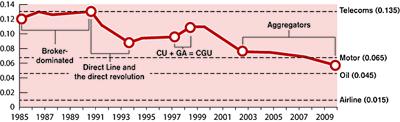

Figure 1 plots the Hefindahl Index (HI), a common measure of the competitive structure of an industry, for the UK motor market over the period 1985 through 2009. Comparison points are shown for several other industries.

The inverse of the index gives a rough estimate of the number of effective competitors in the market. For example, the HI index of 13% for 1985 through 1990 implies that there were essentially eight firms vying for market share in that period; and the HI index of 6% in 2009 implies that there are now essentially 16 firms vying for market share. In effect, competition has doubled over the past two decades.

Figure 1. Plot of the Herfindahl Index showing the competitive structure of the UK motor market

Life before aggregators

Like the rings on a tree, this graph tells the history of the UK motor market. Before 1991, the majority of motor business was placed through brokers. There were only a handful of firms in the marketplace with the brokers effectively controlling market entry by funneling business to these larger firms and ignoring new entrants.

In 1991 the advent of Direct Line changed the picture: rather than relying on brokers for business, Direct Line went directly to the customers. Over the next decades, its market share expanded from almost 1% in 1990 to 10% in 2000 and almost 16% today.

The spike from 1997 to 1998 represents the merger of Commercial Union and General. The sharp increase in competition in the years following this is attributable to UK insurance and Esure entering the market and Churchill, Groupama and Zurich expanding their writings while Aviva shrunk theirs. All of which brings us to 2002 and the first aggregator.

Price contest squeezes profits

The first insurance aggregator, confused.com, was launched in 2002. Previously, only about 1% of insurance had been placed online; but a year later that number had risen to almost 10%. Currently, more than 40% of motor insurance is placed online with the majority of that business coming from aggregator sites. In five years’ time number will be closer to 75%.

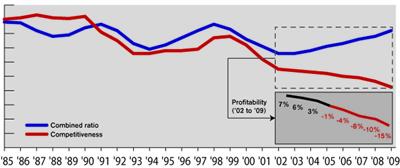

But the aggregators have cost the insurance industry enormously in terms of unnecessary competitiveness. Figure 2 illustrates the extent to which this has happened. Here, we have overlaid the combined ratio for the UK motor market over the same time period.

Figure 2. The relationship between competitiveness and profitability in the UK motor market

Focusing on the period following 2002, the conclusion is obvious and rather damning – the aggregators have encouraged greater price competition while not showing much profitability themselves, channeling revenue to advertisers. Aggregators cost the industry £1bn last year in unnecessary price competition while generating only £50m in profits for a select few insurers. Further, advertisers have more than doubled their revenue with more than £100m due to advertising spends for price comparison sites. Effectively, aggregators have commoditised the motor market.

Where there was at best a tenuous relationship between the market structure and the profitability prior to 2002, subsequent to 2002 as competition increases, profitability decreases with a correlation of almost -96%. This is only natural as insurers are no longer to the same extent competing on brand, marketing, service or other intangibles – rather they are competing almost solely on price and their position on the aggregators’ screens.

Skinny margins unsustainable

In situations like this, each new entrant creates additional supply, driving down industry profits. In theory, this occurs until no excess profits exist; however, the current situation is much worse. What we are seeing is insurers cutting prices below the actuarially fair rate in order to maintain volume. In addition, as a byproduct of their participation in these aggregators they are writing business which they previously would not have actively pursued.

The past 10 years should have been extremely profitable, with inflation steady at around 2%. But rather than several years of profitability allowing insurers to build up their capital reserves, the industry has been taking larger and larger losses.

In the US motor market, as Liberty Mutual chief executive Ted Kelly recently noted: “We’ve had no inflation for 10 to 12 years. Any idiot can make money in personal motor.” Aggregators have been completely unsuccessful in the US market (and it is better for everyone that they stay that way).

In the UK, however, with many economists forecasting several years of high inflation much akin to that of the 1980s, these ultra-thin/too-thin margins which the aggregators have been forcing the industry to increasingly write at are not sustainable.

Take refuge in a niche

Without a fundamental shift in the structure of the marketplace or the way business is done, the future of the UK motor market looks bleak. Mergers would certainly help, as would consolidation of single insurer brands into a single marketable product; on the other hand, breaking up the various insurance arms of larger multinationals is likely to do much more harm than good.

And in the absence of any change in the market structure, the question really is: what is the next big innovation? Pay-as-you-drive (PAYD) insurance, piggy-backing on the green movement, is certainly a contender and had been adopted by several large US insurers.

For the most part, as the structure of the industry is outside any one insurer’s control, and fundamental changes in insurance don’t happen that all that often, the key is to retool your business plan and carve out a niche market where the aggregators have no influence.

George Maher and Ryan Warren are directors, and Andy Staudt is a senior analyst, at Towers Watson