As our comparison of Lloyd's results shows, COR is not a standard measure

The combined ratio is perceived as the universal measure of underwriting profitability across the global insurance and reinsurance industries. Closer analysis of some of the ratios posted, however, shows that combined ratios are anything but universal.

While conventions exist, there is some flexibility in the way combined ratios are produced. They are not a part of generally accepted accounting principles (GAAP) but rather are a measure specific to the insurance industry and typically reported separately from the main audited income statements and balance sheets.

x + y = ?

The combined ratio is the sum of the claims (or loss) ratio and the expense ratio. These two ratios are in turn calculated by dividing net claims and cost respectively by net premiums earned.

However, several companies exclude certain costs from their expense ratios, resulting in lower combined ratios than those who factor in all costs. Furthermore, not all companies exclude the same costs.

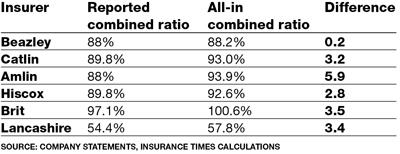

The table below shows the difference between reported combined ratios and ‘all-in’ combined ratios for the listed Lloyd’s insurers that have posted results so far. In some cases, there are several percentage points difference. In the case of Brit, taking an all-in approach produces a combined ratio of over 100%.

Only one of the companies studied – Beazley – takes an all-in approach to calculating the ratio. Markel International, the Lloyd’s and London market division of US insurer Markel Corporation, also uses an all-in approach to calculating its ratio.

Incentives to exclude

Why would companies pare down their ratios? One cost that is often excluded is employee bonuses – both Catlin and Amlin, for example, strip these out. This is because, in a good year, bonuses paid effectively work against the underwriting improvement. The better the underwriting, the higher the bonus, and so the worse the expense ratio.

Another reason is simply peer pressure. If several companies are doing it, those that don’t follow suit will have comparatively worse ratios.

Some see this as a non-issue. Companies typically disclose the costs they are excluding, and so it is relatively easy for equity analysts to add them back in. Several analysts do this, providing investors with a consistent picture. One source quipped that the differential is only really a challenge for lazy analysts.

Getting the full picture

However, others argue that using a stripped-down combined ratio figure as a headline number causes confusion.

Journalists, unlike analysts, typically do not add the stripped out costs back in, so those relying on the trade press for their financial information could be getting an inconsistent picture.

Also, underwriters relying on the lower combined ratios may be lulled into a false sense of security that their underwriting performance is better than it is, potentially leading to less caution.

While companies may have valid and logical reasons for excluding certain costs from their combined ratios, some feel the lack of consistency ultimately undermines the usefulness of the combined ratio.

“Inconsistent calculations of the reported combined ratios reduces the credibility of the ratio as a measure of operating performance,” argues one finance director. “It creates confusion in the insurance market with our underwriters, with analysts and also investors.”

No comments yet