Like the oil platforms that were ravaged by hurricane Ike, the Gulf of Mexico wind storm book lies in ruins, writes Lauren MacGillivray.

It wasn’t supposed to be like this. By the time Ike hit land in September 2008, it had weakened to a Category 2 storm, according to the Saffir-Simpson hurricane scale. But it blew hurricane winds over a 125-mile radius and tropical storm winds over a 255-mile radius.

Fifty-four oil platforms were destroyed and a further 95 damaged as Ike overtook hurricane Ivan as the third most expensive insured loss in the past 10 years, at $15bn or £10.8bn (see bar chart, overleaf).

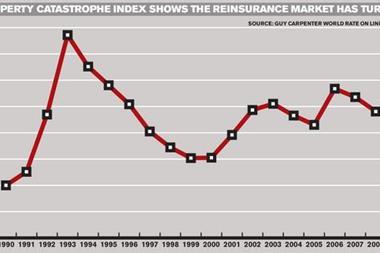

With the market’s capacity expected to be about 30% lower than it was last year – depending on fresh capacity from Berkshire Hathaway – broker Willis has used its latest Energy Market Review to warn that the future of Gulf of Mexico wind storm insurance is in jeopardy. As the report notes, these policies account for a quarter of upstream insurers’ premiums (see chart, right).

“Faced with an even more limited and expensive product, we understand that some energy companies are likely to question the viability of continuing to purchase this cover,” says the report. “Given the potential disconnect between supply and demand for Gulf of Mexico wind insurance products, it is little wonder that market pessimists are forecasting the end of Gulf of Mexico wind as a viable insurance class.”

The report adds that several energy insurers have found their initial loss estimates to be “wholly inadequate”, concluding that Gulf of Mexico risk is “more confused, volatile and expensive than ever before”.

“It is clear that Ike was no normal Category 2 storm and, in terms of the number of platforms damaged, this is a very sizeable event,” says Paul Dawson, underwriter for energy at Beazley Syndicate. “We shouldn’t be surprised that we will be paying a substantial claim.”

On top of this, reinsurance capacity for direct insurers in this market is set to be as little as 70% of last year’s total.

What’s the solution? Willis believes one answer is to introduce a capital market instrument. This would allow reinsurance companies to transfer risk into the capital markets via private investors, allowing them to generate more capacity to the direct market, which may fix the supply and demand imbalance.

Hurricane index

Willis has unveiled a capital market instrument called the Hurricane Index (see chart, right), which delivers parametric cover. Rather than traditional indemnity-based risk, parametric cover means payouts are triggered solely by the physical characteristics of the storm, such as wind speed or radius.

This type of cover relies on basis risk. This means the policyholder cannot recover losses from a hurricane unless the physical characteristics of the storm breach certain trigger levels.

Parametric cover has been available for some time but has not been accurate. Willis claims its index minimises basis risk for policyholders because it is based on maximum wind speed, radius of the hurricane-force winds and wave height.

Wave height in particular, it says, allows the index to more closely match actual losses sustained than other similar products.

“Achieving this ultimate solution to a seemingly insoluble risk management problem for the energy industry will require the goodwill and understanding of everyone involved: risk managers, catastrophe modellers, brokers and the capital market specialists, insurers and reinsurers,” says Alistair Rivers, Willis Energy’s chief executive.

“To date, this understanding has not always been in evidence; however, the needs of the energy industry now require us all to step up to the plate.”

Energy market overview

Putting the wind storm issue aside, the energy insurance market as a whole is relatively stable and capacity levels are up by about 5%.

But in the longer term, it is believed energy companies will resist the prospect of a hardening market as they try to defend their profitability from falling demand and lower crude oil prices.

Because of this, insurers are facing reduced premium income, a threat that is also the result of the credit crunch-related fall in construction work and lower business interruption values.

Insurers need rate increases to ensure long-term profitability in this sector. Since the third quarter of 2008, underwriters’ profitability has been hurt by larger-than-expected wind storm losses from Ike, as well as a drop in investment income down to the economic crisis.

Construction

No major natural catastrophes have affected the construction market since hurricane Katrina in 2005, although overall and insured total losses in 2008 were markedly higher than during 2006/07.

With no major natural losses, rating levels have been maintained. But Willis has started to see “clear indications” of a market hardening.

The credit crunch has made its mark on the construction insurance market since July 2008. Capacity for 2009 has hit a seven-year high of up to $2.5bn (£1.8bn), based on markets with a Standard & Poor’s credit rating of A- or above. The report says “contractors’ books remain extremely full, vendors and suppliers are stretched and overall project values continue to be very high”, and insurer appetite for quality business is strong. But as construction work slows, more competitive pricing is expected.

International liabilities

International liabilities refer to the conditions in the liabilities market for companies domiciled or with corporate headquarters outside the USA.

When Willis last reviewed the energy sector liability market, there had been benign conditions for several years. Some buyers, for example, had benefited from year-on-year rate reductions of up to 40% over four years.

However, as in other markets, more difficult conditions are expected. Meanwhile, insurers and insurance buyers are increasingly focusing on tax and regulatory compliance.

“It is clear that an increasing number of insurers and insurance buyers are putting both tax and regulatory compliance at the top of their agenda,” says the Willis report.

It adds: “It is also critical to ensure that there is an agreed approach on the specific programme with the parties involved.

“For example, it is vital to ensure that on a multinational programme, local policies are issued correctly in all territories where this is required.

Even where non-admitted placements are permitted, there may be penalty rates of tax applied (as in Canada).”

US excess liabilities

Companies domiciled in or with corporate headquarters in the USA can expect premiums for excess liability insurance (including petrochemical and chemical risks) to rise by up to 12%. But over-capacity means this might not happen until early 2010.

There are several reasons for this, including an increase in catastrophe losses in 2008, investment losses and the disappearance of excess capital.

“One might expect that, since some of these factors are not directly related to this market, rating levels for this class should not be affected,” says the Willis report. “However, given the magnitude of the dollar amounts involved, these events/conditions will most likely transcend product lines and result in increased excess liability premiums.” IT

No comments yet