First-half 2011 results generally more encouraging than this time last year

Soft rates in commercial lines are continuing to drag on UK insurers’ results despite improvements in personal lines, recently filed results show.

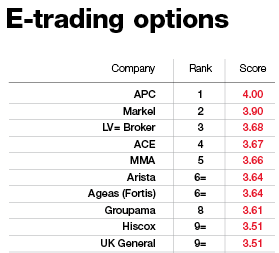

But the first-half 2011 results reported so far are generally better than they were this time last year thanks to rising rates and re-underwriting (see chart).

Zurich UK’s operating profit increased to £71m in the first half of 2011, from £60m in the first half of 2010. The combined ratio improved 1.3 percentage points to 98.4% from 99.7%.

Part of the reason was an 18% increase in personal lines rates. But Zurich UKGI’s chief marketing officer Kay Martin said the company’s two commercial divisions achieved rate increases of 3%, which, while on target, were not enough. “Our view is while we are hitting plans we feel that the market needs to move and if we don’t see rate increases continue this year and into 2012 over and above claims inflation, there will be a significant correction in the market in 2012 or 2013,” she said.

Similarly, Allianz UK’s commercial lines gross written premium grew just 1.9% in the first half of 2011. The growth that was seen was down to rate increases in commercial motor. But Allianz UK chief executive Andrew Torrance said other commercial lines were only able to achieve rate increases of between 2% and4%, which he said was “a reflection of a market which remains highly competitive, and a policyholder base operating in an economy showing only very muted signs of a return to normality”.

He added that the company cut its exposure to unprofitable commercial business during the first half of 2011.

Allianz’s first half 2011 profit dipped slightly to £77.5m from £78.4m as a result of lower reserve releases.

Zurich’s Martin said her company was equally intolerant of poorly performing commercial business. “We continue to focus on retaining and attracting business at the right price. We are absolutely prepared to walk away if it doesn’t meet our criteria,” she said.

Commercial lines performance also held back Aviva and RSA’s first-half results. RSA’s personal lines book made a profit of £27m but its commercial book made an underwriting loss of £19m. Aviva’s personal lines underwriting profit was £67m compared with a commercial loss of £12m.

No comments yet