The drastic change to the Ogden discount rate has dominated the motor market over the past year, but it’s not the only challenge facing motor insurers

The Ogden rate has dominated the agenda of UK motor insurers throughout the past year.

But there are plenty of other challlenges facing motor insurers.

Brexit, claims inflation, tax increases and terrorism have all had an impact on the market.

“An absolute smorgasbord: Brexit, Ogden, IPT, vehicles used as a weapon by terrorists and increasing repair costs way above inflation as vehicles are built with more expensive technology,” says Graeme Trudgill, Executive Director, British Insurance Brokers’ Association (Biba).

Trudgill also highlighted the passage of three Parliamentary bills that will all affect motoring issues. The Civil Liability Bill, which has not been introduced to Parliament yet, the Financial Inclusions and Claims Bill, which will see the Financial Conduct Authority (FCA) regulating claims management companies, and the Automated and Electric Vehicle Bill.

In addition, he says: “Advanced driver-assistance systems (ADAS) developing quickly which brings more cost to repair but should reduce the number of incidents and of course there is the European Commission Refit of Motor directive which we hope will deal with the Vnuk unintended consequences.”

The European Court of Justice’s Vnuk ruling could force owners of off-road vehicles like mobility scooters and golf buggies to buy third party liability insurance.

Despite this array of issues it was the Lord Chancellor’s announcement on 27 February of a change in the Ogden discount rate from 2.5% to -0.75% that caused greatest consternation within the industry.

Significant impact on profits

The change in the rate, used to calculate the size of one-off compensation payments to injured claimants needing long term care, caused great surprise and had a significant impact on the 2016 year-end profit and loss accounts and balance sheets for many insurers.

It also caused motor premiums to soar.

Simon Warsop, Chief Underwriting Officer for Aviva’s personal lines business, says: “For certain people that meant the cost of settling a claim doubled in some cases. As insurers we have passed that cost onto our customers.”

However, in September the new Lord Chancellor unveiled proposed reforms that would “make sure personal injury victims get the right compensation” and would move the rate back to between 0% and 1%.

Warsop adds: “The thing here is that in most manufacturing industries they know what it has cost before you assign a price. As insurers you take the cost from the customer and it is only a long time afterwards when you actually find out what it cost to pay the claims.

“We know what the Ogden discount rate is today, but we don’t know what it will be when we are settling the claim. That announcement of the change and the review of how the rate was set has created a lot of uncertainty.”

Liability perils

The change in the discount rate also highlighted other issues for insureds in addition to increased premiums.

Trudgill says: “The dramatic Ogden change introduced a significant underinsurance problem regarding liability perils. We have seen reserves for EL/PL claims increase from £8m to £15m, so brokers are reviewing limits of typical £10m policies and considering excess layers.

“If the Lord Chancellor’s changes go through, the current prediction is the discount rate will land between 0% and 1%, so the dramatic change we have seen will be mitigated to a degree but it is still different from the previous plus 2.5%.”

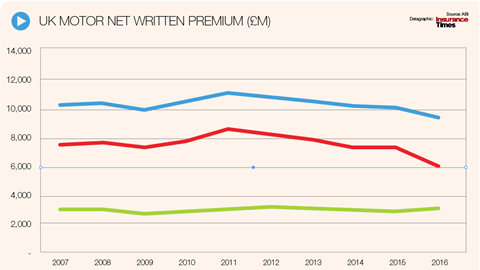

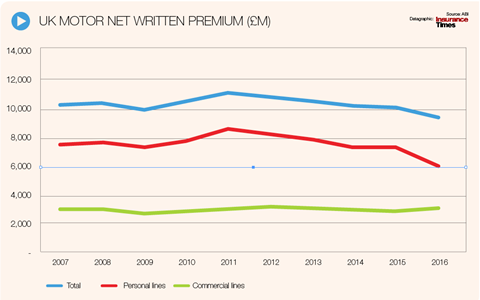

Spurred by Ogden, the average motor premium rose by nearly 14% compared over the twelve months to June this year, according to figures from the Confused.com Car Insurance Price Index in association with Willis Towers Watson.

However, rates underwent a slight reversal in the third quarter of 2017 falling by an average of 1.1%. Small though it was, it was the largest quarterly reduction in premiums seen in more than three years, and only the second quarterly fall seen in that time.

According to Willis Towers Watson, the third quarter’s decline in prices reflected in particular insurers’ reactions to the prospect of a forthcoming increase in the Ogden rate.

“If you look at what happened during the year because rates are so competitive when prices increased they didn’t increase the whole way. If the Chancellor hadn’t made the September announcement we would have seen another increase in October and November, but those planned increases got scrapped,” says Mohammad Khan, UK general insurance leader at PwC.

He continues: “Rates aren’t going to fall off a cliff but they are going to continue gently softening towards the end of this year and into next year. We’ve had the hard market so if you’re not profitable in Motor now it is difficult to foresee how in the near future rates are going to harden even further. From an underwriting perspective if you haven’t got the underwriting right now it is going to be much tougher for you next year.”

Few have made a profit

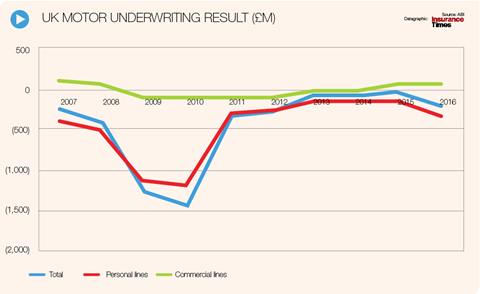

Yet, it appears that many insurers have been unable to produce positive underwriting results despite enjoying this hard market.

“Not that many insurers made an underwriting profit in 2016,” says Tony Sault, UK general insurance leader at EY.

“The market average operating combined ratio was 109% for motor, and they all made their money on reserve releases on prior-year underwriting,”

Sault continues: “The average expense ratio is 26.4%, which is still very high relative to what they are writing. Anyone who can keep that under 20% is doing well but there are not many players doing that.

“There’s still uncertainty around what the whiplash reforms will finally look like and what will actually be implemented. We think the reforms will be beneficial to insurers but how far and by how much it is very difficult to say at this point in time.”

Whereas whiplash claims have been the cause of claims inflation in the past now insurers are seeing the rising cost of vehicles repairs as a major cause.

This is partly caused by the drop in the value of the pound since the Brexit referendum, which means it is now more costly to import the parts needed for many repairs.

And it is also due to the increased value of many of these parts, which are now often packed full of technology, such as sensors.

Biba’s Trudgill highlights a recent visit to vehicle safety experts Thatcham Research where it was shown that one BMW headlight could now cost £5,000.

Ogden has also caused an increase in the cost of large personal injury claims, largely for very young or very old drivers. However, this is helping drive the continued rise of telematics from the 750,000 live policies at the start of this year with boxes, on-board diagnostics port and app systems developing all the time.

Warsop says: “What we have seen more pressure on older and younger drivers and these are the two populations that can least afford premium increases. That has contributed to the rise of telematics.”

He continues: “The young drivers that were shy of having a black box in the vehicle have now got sound economic reasons to get over that shyness. We have passed the tipping point with telematics and there are some large telematics books out in the market.

“We are pretty much at the stage now if you’re a young driver living away from home and owning your own vehicle and you choose not to have a telematics box you’re a bit odd and the industry will now be asking why they don’t want that box.”

It is not only telematics where the march of technology is making its mark on the motor market with the growth of advanced driver-assistance systems (ADAS) and a continued uptake in insurtech changing a range of factors, from the way insureds drive, to the way insurers connect with customers and handle claims.

Sault says: “It is still very early to say what the impact of autonomous driving technology is having on the accident rate. The anti-collision, automatic slow down technology that stops cars drifting out of lanes and things like that. We know that’s having a positive impact on the accident frequency but we haven’t seen any data yet to show how much of an impact that is having on the insurers’ claims ratio yet.”

Meanwhile, Trudgill says there are all sorts of insurtech ideas are in the pipeline, adding: “Biba has just launched a new members Insurance apps facility which members are very keen on, so brokers are embracing insurtech”.

Sault says it is not just the brokers that are looking at this area with many insurers showing “an appetite for investing or playing with insurtech companies to see how they can improve the customer experience and hopefully friction and cost in the motor equation”.

He adds: “There’s lots of insurers playing with pilots and proof of concepts using these insurtech companies, which is interesting to see.”

One development that could prove significant, according to Khan, is Co-op Insurance’s chatbot, which is available on Facebook and can give a driver a quote for cover after asking just four questions.

Khan says: “It is interesting they’re doing that and in the medium term it is a threat to insurance companies on the distribution side. It is somebody coming up with a form, or a way of reaching out to the customer, capturing the customer and not having the customer having to do too much to get an insurance premium.”

No comments yet