After being crowned as market-leading insurers at this year’s Insurance Times Awards, Insurance DataLab explores the figures behind the trio’s successes in 2022

The annual Insurance Times Awards is one of the highlights of the year for the UK general insurance (UKGI) market, as the great and the good of the industry come together to celebrate its achievements from the last 12 months.

Three of the most prestigious awards of the night are the nominated accolades for Personal Lines Insurer of the Year, Commercial Lines Insurer of the Year and the overall General Insurer of the Year.

For 2022, Aviva picked up the gong for General Insurer of the Year, retaining its title from last year.

The insurer had another strong year in terms of underwriting – Insurance DataLab’s analysis of its latest Solvency and Financial Condition Report (SFCR) revealed an all lines combined operating ratio (COR) of 95.9% for 2021, marginally ahead of a market aggregate COR of 96%.

This marked a 2.1 percentage point improvement for Aviva compared to 2020 – this means that the insurer has continued to report a profitable underwriting result following its 100.4% recorded COR for 2019.

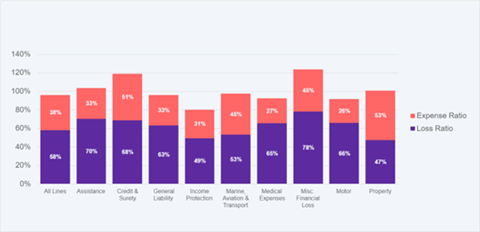

Aviva’s strongest performing line for 2021 was income protection, which had a COR of 80.1% and gross written premium (GWP) of £47.1m.

Other profitable lines for the insurer in 2021 included motor insurance, with a COR of 91.6%, medical expenses (92.2%), general liability (95.9%) and marine, aviation and transport (97.6%).

Aviva’s motor performance is particularly pleasing for the insurer considering that this business line accounts for more than a third of Aviva’s overall book of business, with GWP of £1.7bn making it the insurer’s second largest business line behind property, which has GWP of £2bn.

While the 91.6% motor COR reported by Aviva for 2021 is 1.6 percentage points higher than 2020’s result, it is still 5.4 percentage points better than the aggregate motor COR - Aviva continues to outperform the market when it comes to motor underwriting performance.

The insurer’s two underwriting arms in the UK – Aviva Insurance and Gresham Insurance – were also rated highly in Insurance DataLab’s Underwriting performance report 2021, which was published in February 2022. This analysis compares insurers’ latest CORs, three-year aggregate CORs and COR improvements over the last year.

Aviva Insurance and Gresham Insurance received underwriting scores of 65% and 71% respectively, compared to an industry average of 63%.

Read: Revealed - Who won at the Insurance Times Awards 2022?

Read: Top 50 Insurers 2022 Digital Edition is now live

Explore more news analysis here, or read up on insurers here.

Aviva also performed strongly in Insurance Times’ annual Five Star Ratings Reports - particularly in commercial lines, where its score of 3.95 out of five was the second highest featured in 2022’s report, earning the insurer an overall five star rating.

Looking at customer experience, Aviva fares well here too.

Indeed, the insurer outperformed the market average according to Insurance DataLab’s assessment of sector-wide customer experience, which was published in its Customer experience report 2022 in September 2022.

This research looked at insurers’ and brokers’ customer experience performance across four key pillars – claims, complaints, customer satisfaction and transparency.

Aviva picked up an Insurance DataLab customer experience rating of 70% for 2022, one percentage point above the market average.

Zurich ranks top in commercial lines

In terms of commercial lines specifically, Zurich rose to the top at the Insurance Times Awards and was named Commercial Lines Insurer of the Year for 2022.

The insurer had a strong year from an underwriting perspective - it has returned to profitable territory after knocking more than seven percentage points off its COR for an all lines combined operating ratio of 99.2%, according to its latest SFCR.

This improvement was driven by a reduction in both operating expenses and net claims incurred, with the insurer’s expense ratio improving by 4.6 percentage points in 2021 after a 7.7% drop in expenses. Meanwhile, its loss ratio improved by 2.5 percentage points last year following a 3.6% reduction in net claims.

The insurer’s strongest performing line in 2021 was workers’ compensation, which recorded a COR of just 40% and GWP of £51.6m.

Other profitable lines for Zurich include general liability insurance, with a COR of 90.6%, and motor insurance, which has a COR of 92.6%.

Zurich also reported a 13.1% COR for miscellaneous financial loss business and a 65.7% COR for credit and surety - but these results were skewed by negative net incurred claims across both business lines.

The insurer performed strongly in Insurance Times’ Five Star Ratings Report: Commercial Lines 2022, published in March 2022, after it received a score of 3.73 and an overall four star rating. This was up on the previous year’s score of 3.65, helping it to climb three places in the ranking to place fourth overall.

Zurich was rated highest by the report’s broker respondents for its quality of cover, picking up a score of 4.01 out of five for this metric, compared to a score of 3.89 for the previous year.

The insurer improved its rating across all five of the service areas assessed by Insurance Times in this year’s report.

Read: MGA financials under the spotlight

Read: Complaints fall post-pandemic, but how is the industry really faring?

Explore more news analysis here, or read up on insurers here.

Covéa places first in personal lines

As for the Personal Lines Insurer of the Year prize, this was awarded to Covéa Insurance at this year’s Insurance Times Awards.

The insurer made great improvements in its underwriting results in 2021, knocking more than 10 percentage points off its COR to report an all lines combined operating ratio of 100.4% for that year - although this is still slightly above the 100% breakeven point.

The improvement in Covéa’s performance was driven by falling expenses and a drop in net claims incurred - the insurer knocked 3.7 and 6.6 percentage points off its expense and loss ratios respectively.

The insurer’s strongest performing line was miscellaneous financial loss, which recorded a COR of 79.6% from GWP of £32.9m.

Other profitable lines for Covéa include income protection (82.7%) and property (96.3%).

The insurer should be particularly pleased with the performance of its property book – its second biggest line of business behind motor insurance – after it had a profitable year in a market that reported a loss-making aggregate COR of 102% for 2021.

Where Covéa shone particularly brightly, however, was in the experience it offers to both brokers and customers.

In Insurance Times’ Five Star Rating Report: Personal Lines 2022, Covéa secured top spot with an overall five star rating and a score of 4.51. This compares to an industry average of just 3.89.

Indeed, Covéa was rated number one in three of the five service areas assessed by Insurance Times – this included policy documentation (4.60), relationship management (4.48) and underwriting experience (4.52). It also finished in second place for quality of cover (4.53) and claims experience (4.44). Nine insurers overall were rated in this research report.

Covéa also performed strongly in the aforementioned Customer experience report 2022 – the insurer has picked up a gold award from Insurance DataLab in each of the last two years.

The insurer received a customer experience rating of 75% for 2022 to finish in second place, up four percentage points on the 71% rating it received for 2021, when it finished fourth.

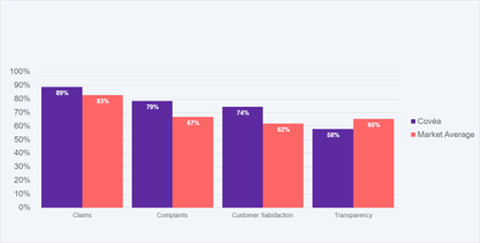

Covéa performed particularly strongly in claims, picking up an 89% customer experience rating for this metric in 2022 – the second highest score across the insurers and brokers analysed by Insurance DataLab. It additionally finished second for customer satisfaction with a metric rating of 74%.

Furthermore, Insurance DataLab found that Covéa was the third highest rated provider for its complaints handling, awarding it a score of 79% for this metric after the insurer reported an upheld rate of 22% for complaints referred to the Financial Ombudsman Service, compared to an average of 27% across all companies covered in the research.

The insurer also received just 1.16 complaints per 1,000 policies sold in 2021, compared to an average of 3.42, according to data reported to the FCA.

Related Companies

- Previous

- Next

No comments yet