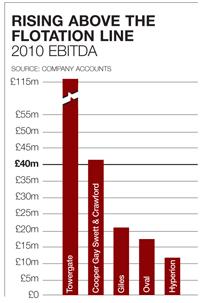

Combined broker posts EBITDA above £40m line analysts say is needed for listing

Cooper Gay Swett & Crawford (CGSC) reported their first combined results, which show the merged company now almost certainly has enough scale for flotation.

The broker posted earnings, before interest, depreciation, tax and amortisation (EBITDA) of $68m (£42m), and fees and commission of $340m last year.

Privately, analysts believe a broker should have at least $60m EBITDA for a flotation to avoid a liquidity problem on the stock market. A number of brokers have listed during the last 10 years, but since the financial crisis their share prices have flatlined.

Cooper Gay’s global operations and strong positions in emerging markets in Latin America and Asia should also attract investor interest.

Chief executive Toby Esser said flotation could take place anytime between this year and 2014, adding: “We were never large enough previously but now we are, and we’re keen to grow and build on what we’ve got.”

Cooper Gay averaged 12% organic growth over the last five years. This growth decreased slightly from 13% in 2009 to 12% in 2010.

Esser said morale in the Swett & Crawford side of the group was good following the merger, and has been hitting budgets and targets.

We say ... only the strong survive

- In the giddy noughties, a number of brokers floated, but found the stock market can be a difficult place. THB, Cobra and Brightside saw their share prices crash after the financial crisis and then flatline, as investors and analysts shy away from small cap stocks without significant growth opportunities.

- Investors want attractive dividends and some kind of a growth story. Debt should be no more than three times earnings, and interest on debt should be within six times earnings.

- JLT, the pin-up boy for wannabe broker floaters, answered all those questions, and its share price has rocketed from just below 200p to 700p since flotation in 1999.

No comments yet