General insurance brokers are being rinsed for funds to compensate for the staggering rise in customer complaints about mis-sold payment protection insurance, and it doesn’t look like the FSA is likely to solve the problem any time soon

It’s painful already and it’s going to get a lot worse - the Financial Services Compensation Scheme (FSCS) levy, that is.

Brokers could hardly believe it when they found out this time last year that the scheme’s funding requirement for the current financial year leapt up nearly eight-fold from £8.5m to £61m. But the FSCS admitted in its business plan earlier this month that there would be another hefty jump next year - the levy is now set to rise 57% from the final figure for 2010-11 of £59.6m to £93.5m.

This rise is a direct response to the staggering increase in recent times of mis-sold payment protection insurance (PPI). The latest quarterly figures of activity at the Financial Ombudsman Service (FOS) show that the dispute resolution body received 24,955 complaints about PPI in the final three months of 2010. This is a dramatic 85% increase on the 13,520 PPI-related cases the service received in the quarter ending June 2010.

The report also reveals that since December’s launch of a judicial review by the British Bankers’ Association into the way the Financial Services Authority (FSA) handles PPI complaints, the FOS has been receiving up to 4,500 payment protection product-related cases a week, as consumers go straight to the Ombudsman rather than seeking redress from the company that sold their policy.

Handcuffed together

These figures spell nothing but bad news for general insurance brokers, as it seems that their fate will be linked to the behaviour of PPI vendors for some time to come.

FSA chief executive Hector Sants admitted after his lecture at the Insurance Institute of London last week that the timing of the long-promised overhaul of the scheme remained uncertain.

With the review of the FSCS tied up with the government’s wider overhaul of financial regulation, it is increasingly likely that the brokers will still be lumped in with sellers of PPI insurance next time the levy is set in 2012.

Another delaying factor, suspects Biba head of compliance and training Steve White, is a new draft EU directive regulating insurance compensation. The Insurance Guarantee Schemes Directive is currently out for consultation, with the final version not due to be published until the beginning of December.

It proposes that schemes like the FSCS should be pre-funded with money raised in advance for helping customers who have been mis-sold policies. If this were to be implemented, it would involve a major overhaul of the FSCS, which collects the money it needs for compensation payments after the levy has been set.

Brokers fear that next year - when they are still forking out for the cost of mis-sold PPI – the volume of compensation payments is likely to be a lot higher than it is today.?“We have to make sure that the FSA gets on with the consultation process,” White says.

The results of this could be disastrous – an increasing number of the firms say they are either going to go out of business or get rid of staff as a result of the increasing levies.

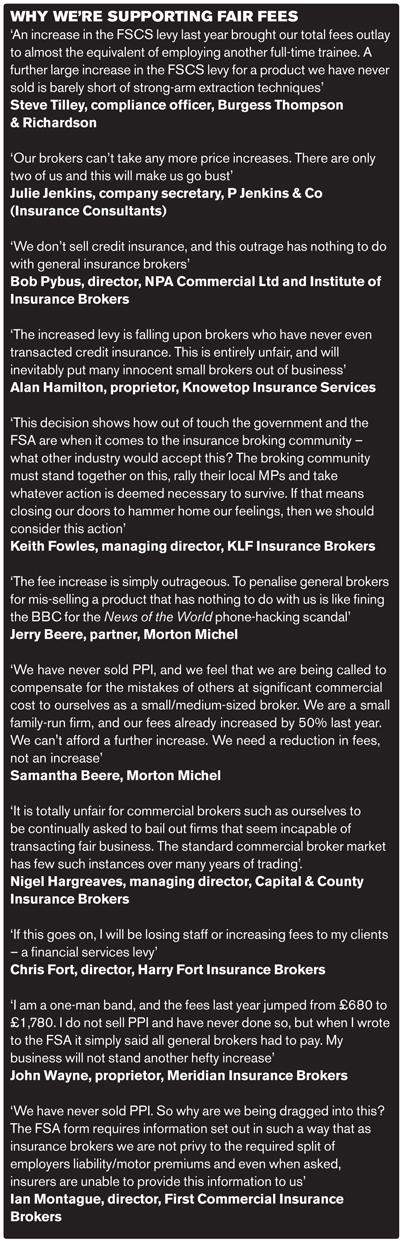

While the bulk of feedback to Insurance Times’ Fair Fees campaign has come from smaller brokers (see box), the consolidators are feeling the pinch too, owing to their exposure to SME businesses.

A senior director at one large consolidator confirms this: “We are paying a significantly disproportionate amount to the FSCS across our different entities.”

Pain relief

Given that escalating levies are likely to be a fact of life for at least the next two years, what can businesses do about it?

Biba has urged brokers to double-check that they are not declaring non-eligible income when submitting their levy returns to the FSA. Until just a couple of years ago, the hassle of splitting out eligible from non-eligible income was not worth the hassle because the levy itself was a relatively small figure. But the year-on-year ratcheting up of the amount means that doing the exercise is increasingly worthwhile.

Eligible income for the FSCS includes all personal lines and commercial policies for businesses with a turnover of less than £1m per annum. For bigger businesses, mandatory classes of insurance (commercial third-party motor and employers’ liability) also count as eligible income for the scheme’s purpose. Brokers dealing with larger clients can therefore cut the size of their payments to the FSCS.

White argues that splitting out income is in the interest of the sector, as well as the individual broker. The FSA bases its assessment of the total compensation brokers can afford to pay, currently £195m, on the income that the sector declares.

Some classes of insurance, such as personal lines, are easy for any broker to distinguish. But working out what counts as eligible income for a policy with a corporate customer can be trickier. White says brokers often must rely on insurers to tell them what counts as eligible income.

But compliance consultant Branko Bjelobaba says the FSA should be a lot more proactive about telling brokers that they can save money by declaring which income is not eligible. “What other regulator would take these figure as read?” he fumes.

Sadly for many brokers, however, such tactics are unlikely to make much difference – the rules of the game are what need to change. IT

Click here to sign the online petition.

Our Fair fees campaign

Last year, Insurance Times hit the campaign trail for the first time in half a decade to fight the massive increase in the Financial Services Compensation Scheme (FSCS) levy.

The campaign aims to:

- ring-fence professional insurance brokers from the rest of the financial services sector when the FSA establishes its new framework for the FSCS;

- exclude the mis-selling of payment protection insurance (PPI) from the compensation scheme for professional brokers;

- ensure that the fees and levies paid by brokers are proportional to the risks they bear; and

- protect professional brokers from having to pick up the tab for the failures of the banking sector.

Since the campaign's launch last year, we have highlighted the problems the increased levy has caused for brokers, while exposing the companies that have fuelled the explosion of the FSCS through their mis-selling of PPI. Hundreds of brokers have signed our petition at insurancetimes.co.uk/backfairfees.

Over the coming months, as brokers brace themselves to

receive their bills for this year's levy, Insurance Times will continue to highlight the inherent unfairness of a compensation scheme that urgently needs reform.

No comments yet