RSA grew commercial lines NWP by 11% in Q1, but underwriting discipline, not rate rises, may have been the main driver

After a year of having its UK premium growth dictated by personal lines, commercial lines was the driving force behind RSA’s 4% uptick in net written premiums in the first quarter of this year.

Commercial lines net written premiums were up 11% compared with the first quarter of 2011, while personal lines premiums were down 2%.

By contrast, personal lines premium growth was 10% in 2011 as a whole, compared with the more modest 2% growth in commercial lines.

Is this the beginning of a resurgence in UK commercial lines? Sadly not. While RSA’s commercial motor price rise of 9% surpassed the rate increases that the insurer achieved across the rest of its book (including personal lines motor rate hikes of 8%), commercial liability and property premium rates increases are still far more muted, at 2% and 3% respectively.

Balancing the discipline

RSA is not alone. A study by insurance IT provider Acturis determined that there has been little sign of commercial rates increasing so far in 2012.

What it does indicate, though, is that personal lines motor is no longer the growth engine it was. RSA’s experience indicates that underwriting discipline is starting to counteract the price rises seen over the past couple of years and eat into premium volumes.

Such a trend is positive as long as it does not go too far. Tougher underwriting will cut losses and improve underwriting results, potentially improving the combined operating ratio, but lower premiums can counteract this. It is a tricky balancing act.

Getting serious on whiplash

On the theme of personal motor pricing, the insurance industry and the government took another step towards their aim of tackling the deluge of whiplash claims and lowering motor insurance premiums yesterday with the second summit between ministers and insurance bosses.

One of the key themes was making it easier for insurers to reject what they feel to be unfair whiplash claims and separate the genuine cases from the fake.

There are still several key questions to be answered, however. A big one for insurers is when, and to what extent, the government will want to see cuts in motor premiums in return for lower whiplash claims, and how this will be measured.

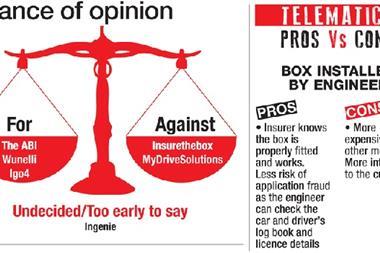

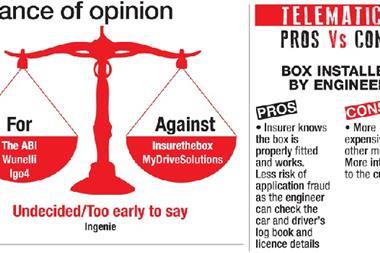

Telematics is likely to play a key role, although some question whether it is the panacea its backers are touting it as.

Nonetheless, the insurance industry has clearly taken telematics to its heart. As Insurance Times revealed today, the ABI has set up a telematics committee with Ageas managing director Mark Cliff at the helm. It will be interesting to see what impact it has.

No comments yet