The financial organisation’s latest research also reveals ‘worrying’ trends around paying for business insurance due to Covid-19’s direct impact on SMEs

As SMEs battle rising insurance costs and the financial squeeze triggered by Covid-19, brokers are responding by zoning in on retention rather than new business as they look to be a “trusted advisor” for struggling small businesses, said Shane Dixon, learning and development consultant at financial company Premium Credit.

Speaking at a webinar co-hosted with the Managing General Agents’ Association (MGAA) last month, titled ‘Supporting businesses as the economy reopens’, Dixon explained that Premium Credit works with around 3,000 different insurance brokers and, according to the company, a lot of them are now “completely changing” how they engage with MGAs and clients.

He said: “Previously, a lot of our partners were really focused on winning new business.

“But what they are really focused on at the moment is what is known in a sales methodology as ‘trusted advisor’.

“This is [a] real key thing that brokers are now trying to move their sales teams towards – it’s about working together with their clients in order to increase retention, but also to have that high focus on results.

“In this space, they are more likely to cross-sale, [upsell], and also buy the right levels of cover that [business owners] are actually looking for.”

Credit crunch

Premium Credit explained that broking is about “going above and beyond just selling [clients] insurance, but providing a whole plethora of advice and support”.

It is also important for brokers to find out how their clients are paying for business insurance, to ensure cover is financially manageable.

For example, the finance company’s inaugural Insurance Index research, which was published at the end of last year, found that of the SMEs and corporates that have used credit to pay for insurance, most firms are relying on credit cards, with 64% using business cards and 52% of enterprise owners using their personal cards.

Around one in 10 who have borrowed money fear that they may default on the loan in the next year.

Speaking on these findings, Premium Credit’s strategy and brand director Adam Morghem, said: “SMEs have had to battle to stay afloat during the pandemic which makes it understandable that they have cut back on insurance and taken out more credit.”

Owen Thomas, the firm’s chief sales and marketing officer, added: “It is worrying that so many SMEs and corporates are relying on personal credit cards or their business cards to pay for insurance.”

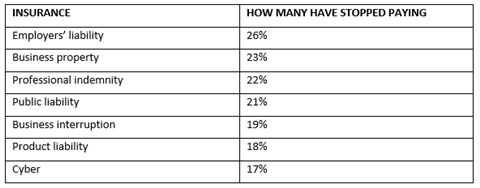

Cutting back on insurance

Premium Credit’s research further identified that nearly one in five SMEs have stopped paying for business interruption (BI) insurance.

To further reduce costs amid the pandemic, 51% of organisations have stopped paying for a range of business insurance policies, such as professional indemnity, property, cyber and employers’ liability.

The index also reflected the financial struggle of SMEs, with 42% stating that they have suffered damage or losses in the past five years because of not being able to claim or being underinsured.

Morghem said: “Perhaps the biggest risk of all is not having the appropriate cover.”

Thomas continued: “We would advise SME owners to speak to their insurance brokers for advice on how best to fund the appropriate level of cover for their business.

“The costs of insurance are rising and businesses need to manage these costs more effectively.”

Increasing touch points

Despite the financial strains of the Covid-19 pandemic, it has also created opportunities – especially around relationship building.

Traditionally, in order to conduct business, insurance brokers travelled to visit clients and may have been on the road for up to four hours a day. “It certainly was the case for me,” said Dixon.

“Now what we are finding is we get a little bit more time, so gone are the days where it would just be one client contact maybe mid-year just to check in on how they are doing before we start to engage about winning that renewal.

“There’s much more opportunity for touch points, really quick conversations with people to really enhance those relationships in this hard market and, ultimately, try and win more business than our competitors.”

To build long-lasting relationships and trust, Dixon highlighted that social media is a beneficial platform for brokers. Sending seasonal and direct messages, utilising website updates and links, as well as creating press releases are also helpful.

Premium Credit’s strategic account manager Dave Sheath added: “Hopefully these measures will continue to be a lifeline for a lot of those SME businesses who are concerned and struggling and worried about their cash reserves lasting.”

No comments yet