Forget price comparison sites and direct online buying: face-to-face relationships are how business is done in HNW, particularly when it comes to tailoring cover for non-standard niche assets. But while the sector may be booming, it’s not always that profitable

Some people appear to be impervious to recession. The latest edition of The Sunday Times Rich List, published in April, revealed that the wealth of Britain’s best-off has soared more than 30% during the past year.

These well-heeled souls may have become even better off because they tend to look for somewhere else to put their cash when stock markets crash, banks go bust and bond markets look risky.

The Russian oligarchs and Asian and Middle-Eastern billionaires that are at the most prestigious end of the high net worth (HNW) market have been busy investing in alternative markets: hard assets such as oil and gold, which have soared in the recession, and other tangibles (albeit niche ones), such as works of art, jewellery and vintage wine.

It’s the high roller equivalent of stashing your spare cash under the mattress. But it’s unlikely that sleeping on your money will earn the type of return available in the niche alternative market.

Earlier this month, the New York office of Christie’s sold Picasso’s 1932 portrait of his lover Marie-Thérèse Walter, ‘Nude, Green Leaves and Bust’, for $106.5m (£73.8m) making it the most expensive artwork ever sold in auction. The painting was owned by the family of Frances Lasker Brody, the Los Angeles-based collector and philanthropist who died last year, and who bought it in 1951 for less than $20,000.

Fine wine returns

Meanwhile, Swiss economists Philippe Masset and Jean-Philippe Weisskopf published a report last month that revealed investments in top-quality wine comfortably outperformed a key benchmark of the US stock market over the past 13 years, with prices more than doubling and even quadrupling in auctions.

Small wonder that HNW individuals continue to flock to niche assets, despite the rise in equity markets.

“There’s been a recent increase in requests to cover modern art in particular, with people seeing this as a potential investment for the future,” Aviva’s HNW underwriting manager Scott Leonard says.

The high net worth household policy has been around for a while, but increasingly brokers have realised that assets such as artworks, or perishables such as wine, are not fully covered by standard HNW homeowner policies.

And in an era when intermediaries are increasingly under threat from price comparison websites and direct online buying, the HNW market remains almost entirely brokered; face-to-face relationships are still the preferred mode of business for most high-end clients, particularly when it comes to tailoring cover for non-standard niche assets that require bespoke policies.

“The broker is king in this market and is likely to remain so,” Chartis UK’s private client group vice-president Nick Grazier says. “There’s been a big shift in the past five years … brokers that were focused on commercial business are now looking at the high net worth aspect of their clients. Brokers want to do more for clients – that has helped drive HNW insurance growth in recent years.”

Sterling Insurance director of commercial and household David Sweeney says that around three-quarters of the firm’s HNW business comes through brokers. “It’s good business with good commissions, and they’re good at accessing clients,” he says. “But part of the reason for the growth in the market is that there is a greater recognition by HNW clients of the need for specialist insurance.”

In many ways, the recent growth can be directly attributed to the recession; partly because HNW clients have diversified their investments into niche assets, and partly, as Grazier alludes, because brokers have diversified their income streams by finding out more about their clients. They’ve simply asked about their art or wine collection or whether they own a yacht or jet or expensive antiques.

But Aviva’s Leonard adds that at least some of the growth, paradoxically, is due to some high rollers cutting their overall spending. “With the depressed housing market, people are often choosing to improve or upgrade their existing property rather than move, hence there has been an increase in requests for cover while works are ongoing,” he says.

“Similarly, in the current economic climate, some HNW clients are choosing to have large family wedding celebrations at home rather than hire hotels. They then look to their insurers to cover this, from the increased liability down to damage to the marquee.”

Diverse range of assets

The diverse range of niche assets requiring cover can surprise even seasoned underwriters. Art, antiques, wine and luxury cars are common nowadays, as are requests for cover for gold and diamonds purchased as an investment as their prices climb to unprecedented levels.

Leonard has also underwritten cover for a collection of Victorian dentist drills and a 1:8 scale sit-on garden railway valued “well into six figures”.

But his “favourite” was to increase liability to cover show-jumping sheep being ridden by teddy bears. “As it was for charity, we were more than happy to offer cover free – fortunately there were no incidents on race day to trouble our claims team,” he says.

Jewellery is another growth market. However, one insurer, who declined to be named, said many in the industry are shying away from “bling cover”.

“It’s fine if the insured wears the item to a restaurant in Knightsbridge and then locks it in a safe the rest of the time,” he says. “But there are a lot of celebrities who wander round some pretty unsafe places with stuff dropping off them. You don’t want to provide their cover.”

Grazier recounts a case where an HNW client’s basement, which held his vintage wine collection, was flooded while he was out of the country. “The water damage resulted in most of the labels coming off the bottles, making the wine effectively worthless.

“But then the housekeeper put in some dehumidifiers in an attempt to dry the basement out. That ended up cooking all the wine. She phoned us very upset, so we sent out a wine expert and replaced the entire collection, bottle for bottle, before the client got back. We even left the old wine with him, as it has no real value once the label comes off.”

As the last example shows, the needs of high-end clients can go far beyond a standard insurance policy and resemble something more akin to a full-time maintenance contract.

“Service is key, and you need the expertise of an extended network of specialists because client demands in high net worth are very different,” Grazier says.

“One of our clients had arranged a large birthday party earlier this year but, because of the heavy snow and ice around at the time, neither the caterers nor the guests could get there. Our policy covers event cancellation, but the claims team at our private client group arranged for the party to take place at a different venue and arranged to get the caterers and guests to the new venue. So our client had his party.

“That’s the difference with high net worth. Claims and money aren’t the issue, it’s the back-up services that HNW clients expect.”

During recent heavy rain, one Chartis HNW client with a home on the Thames discovered the insurer had dispatched a team to sandbag his house while he was away. “It’s not just about writing cheques in HNW, it’s about preventing claims happening, solving problems and, when a claim does occur, making sure our response is suitable,” Grazier says.

The extreme weather of recent years means water damage, through flooding and burst pipes, has become an increasing part of the HNW insurers’ claims book. Sweeney says that around half of his company’s claims spend is water related. “In fact, if you have a Picasso in your collection, it’s more likely to be damaged by water from the upstairs bathroom than it is to be stolen.”

‘Plagued by large losses’

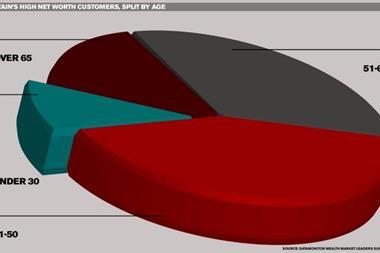

A report into the HNW sector published by Datamonitor this month suggests that recent bad weather means the market is “plagued by large losses”. It claims that water damage accounts for 35% of the total household claims bill, adding that in a year where there are no large losses caused by a weather event, the market combined operating ratio (COR) should be around 90%.

For this reason, Sweeney believes that, although the market is growing, it is not generating as much money for insurers as it might seem from outside the sector.

“It’s not an incredibly profitable account,” he says. “Over the past few years, most insurers haven’t made a great deal of money out of it. There’s been an event of some sort every year in the past three years, and so a lot of money has been taken out.” IT

No comments yet