Fintech investments grow as global insurers strive to stay relevant, while start-ups threaten to steal their business

Insurers worldwide have this year announced significant investments in financial technology (fintech) as they seek to catch up with other sectors and their peers.

It follows a warning by the World Economic Forum (WEF) that major disruptions are in store for many traditional financial services players amid rapid inroads being made by more nimble fintech start-ups.

Disruptive innovation has already been seen in the UK telematics market, where newcomers such as Carrot, Young Marmalade, Insurethebox and Ingenie have carved a niche.

But innovation is better late than never, concludes the WEF’s report The Future of Financial Services 2015. “Insurers have been too slow to embrace innovation for too long – some would say ever since Lloyd’s of London was founded more than 300 years ago,” it said.

“In recent years, they have begun to embrace digital channels and automation to improve and speed up underwriting,” it added.

“But the challenges they are facing on many fronts suggest they must adapt by incubating and incorporating greater innovations to better compete.”

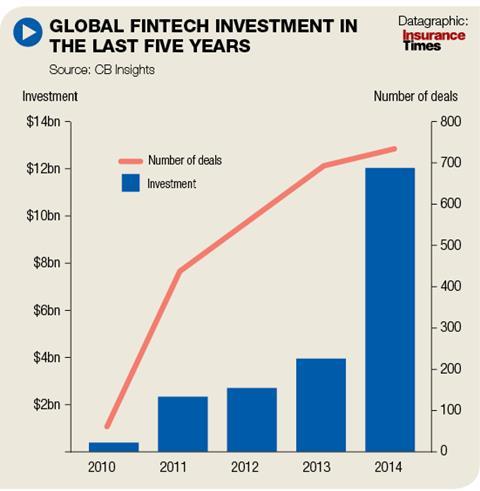

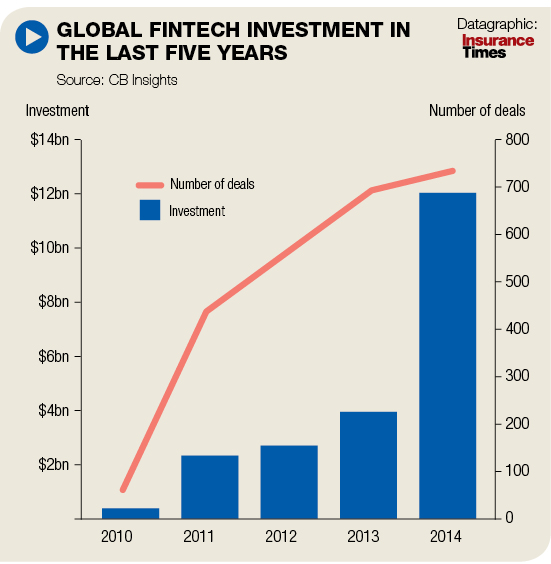

Click here for a larger version

As the insurance industry has lagged behind in technology, consumers have interacted less with insurers than any other industry, according to the Morgan Stanley/Boston Consulting Group (BCG) Global Consumer Survey 2014.

Scouting for tech

With the industry playing catch-up there will inevitably be winners and losers in the race to become more tech savvy.

“A large number of insurance companies around the globe recently had their scouting event in California [Silicon Valley], Israel [Silicon Wadi] or in Shanghai to visit fintech start-ups,” said BCG partner Michaël Niddam.

“This is how they are going about it. What’s happening today is potentially redistributing the gap between players in the market.”

Should the industry’s traditional players be slow to move, there are others who could seize the opportunity. With Google launching a price comparison site in the US and Rakuten, Japan’s answer to Amazon, investing in life insurance, it is clear disruption could come from outside.

Internet and social network companies have rich datasets about consumers that can be of significant value when making underwriting decisions.

“Today anybody who is looking for insurance is starting their research online. So it’s obvious that internet companies can know that somebody is a lead way before any insurance distributor or insurance company,” Niddam said.

“There is a big element of industry reshaping and this is the trend that insurance companies have clearly identified,” he said.

“They are investing to compete.

“You find large insurance companies that have spent hundreds of millions of pounds a year for the past 10 years just to improve their IT infrastructure to support all their digital servicing and distribution needs,” he added.

“In parallel you see companies creating entities whose role is to invest in start-ups and new techs, to explore new business models and new worlds. Some companies do both.”

Join the debate at our Insurance Times Regulation Forum on LinkedIn

{kind=link}

No comments yet