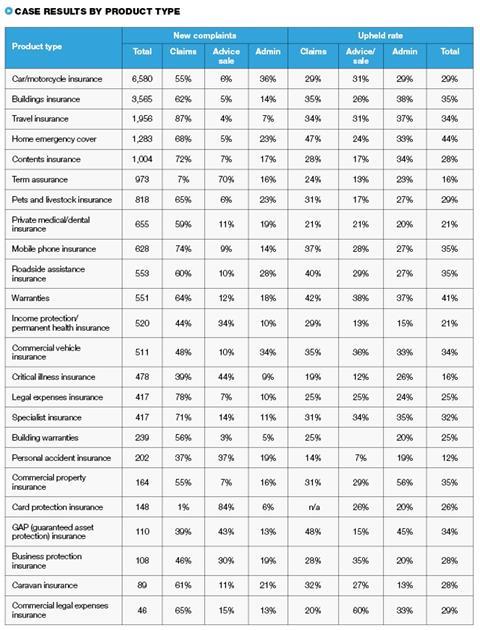

The Financial Ombudsman Service received almost twice as many complaints about car and motorcycle insurance in the six months to March than any other product

Car and motorcycle insurance continues to be the most complained-about general insurance product, according to the latest data from the Financial Ombudsman Service (FOS), published exclusively by Insurance Times.

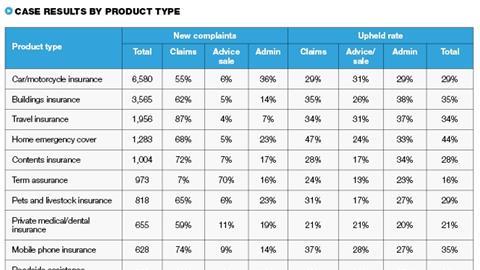

The ombudsman received a total of 6,580 complaints about motor insurance in the six months to the end of March 2019, up from 5,815 complaints for the same period the previous year.

Buildings insurance was the second-most complained about product, with the FOS receiving 3,565 complaints between October 2018 and March 2019, up 48% on the 2,410 complaints received for the six months to 2018.

While motor and building insurance are two of the most common insurance policies sold to consumers in the UK, with both mandatory in certain circumstances, home emergency cover is a less prevalent product. But it still accounted for 1,283 complaints received by the FOS between October 2018 and March 2019.

This makes it the fourth most complained-about product just behind travel insurance in third place with 1,956 complaints.

Almost two-thirds of home emergency complaints related to the claims service provided by insurers, with 47% upheld in favour of the customer, the second highest in this analysis behind GAP insurance (48%), and much higher than the 31% average upheld rate for claims-related insurance complaints across all business lines.

Home emergency products also had the highest overall upheld rate for complaints reaching the FOS, with 44% of home emergency complaints upheld in favour of the customer, compared with an overall average upheld rate of 29%.

An FOS spokesperson said many complaints about home emergency cover could be avoided by insurers paying more respect to their customers when they are going through difficult times, and being more aware of individual circumstances.

“Lots of the complaints we see are about administration, and this includes a range of issues like claims and customer service,” they said.

“In some cases, however, upset could be avoided – we’ve seen complaints about poor communication from an insurer when a consumer is already going through a difficult time, for example in the aftermath of a flood or fire to their home.

“We think that home emergency cover insurers should consider customers’ individual circumstances when they are handling a claim, and be more sensitive when they are vulnerable.”

GAP insurance is often sold by people outside the insurance industry and an FOS spokesperson said insurers still had a responsibility to ensure policy wordings were clear, and that the policies are understood by those selling GAP policies.

“GAP insurance is usually sold by an intermediary such as a car dealership or finance company, rather than an insurer,” they said.

“The FCA has called for anyone selling these insurances to have better communication and provide the options and consequences in a clearer manner. However, insurers have a part to play by ensuring that the wording on policies is as clear as possible.”

GAP offers poor value

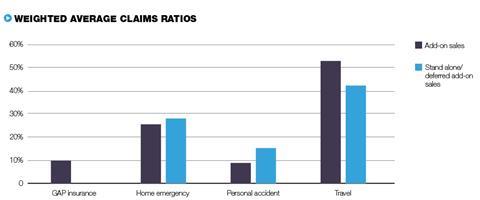

In the FCA’s 2014 market study into the general insurance add-ons market, the regulator’s analysis of claims ratios found that products such as home emergency cover and GAP insurance, which have both fared badly in this analysis of upheld rates, offer poor consumer value.

“The claims ratio results show that, with the exception of travel, the sampled products are poor value, especially when compared to core insurance products,” the FCA report stated.

“For comparison, the average net loss ratio across all personal insurance lines (including motor, household and other categories) for the 2012 regulatory returns was 64% (with 53% for household and 80% for motor).

“The claims ratios for add-on sales of GAP and personal accident indicate particularly poor value. For home emergency add-on sales, nine out of the 10 firms that provided 2012 claims data or pricing model data had claims ratios below 30%.

“This is still low compared with the average across core products, or indeed when compared to travel, the better performing product in our study.”

Cause for concern

At the time of the 2014 study, the FCA recognised that insurers were aware of the issues regarding poor customer value inherent to these products, and that they were working to offer “greater customer value”.

“In their responses to our firm survey, several firms across different products indicated that claims/loss ratios below 30% would be a cause for concern from a consumer value perspective.

“And three firms recognised in their internal documents that their home emergency and personal accident products did not offer good value to consumers,” the FCA report stated.

“One firm reported for its home emergency product with a loss ratio of about 14% that ‘in aggregate the return (claim pay-out to the customer) is relatively low compared to the premiums collected’.

“A second firm selling home emergency identified internally that one of its home emergency products had a low loss ratio (26%) and was taking steps to offer greater customer value.”

Since that time, the FCA has continued to monitor a range of value measures, including claims frequencies and claims acceptance rates, with the regulator finding that four of the 17 insurers reporting over both years had a drop in their claims acceptance rates between 2018 and 2017, while only three had experienced an increase.

Speaking to Insurance Times about the most recent release of ombudsman complaints data, an FOS spokesperson had some simple advice for how insurers can improve their complaints handling and reduce the overall number of complaints received.

“To help reduce complaints, insurers should use less jargon and have clearer wording in their policies,” the spokesman said.

“They should also take all individual circumstances into consideration when dealing with their customers’ claims and complaints.”

No comments yet